Bank of America 2011 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 79

Nonperforming residential mortgage loans decreased $1.7

billion compared to December 31, 2010 as outflows outpaced new

inflows, which continued to slow in 2011 due to favorable

delinquency trends. Accruing loans past due 30 days or more

decreased $1.2 billion to $4.0 billion at December 31, 2011. At

December 31, 2011, $11.4 billion, or 71 percent, of the

nonperforming residential mortgage loans were 180 days or more

past due and had been written down to the estimated fair value

of the collateral less estimated costs to sell. Net charge-offs

increased $162 million to $3.8 billion in 2011, or 2.27 percent

of total average residential mortgage loans, compared to 1.86

percent for 2010. This increase in net charge-offs for 2011 was

primarily driven by further deterioration in home prices on loans

greater than 180 days past due which were written down to the

estimated fair value of the collateral less estimated costs to sell,

partially offset by favorable delinquency trends. Net charge-off

ratios were further impacted by lower loan balances primarily due

to paydowns and charge-offs outpacing new originations.

Loans in the residential mortgage portfolio with certain

characteristics have greater risk of loss than others. These

characteristics include loans with a high refreshed LTV, loans

originated at the peak of home prices in 2006 and 2007, interest-

only loans and loans to borrowers located in California and Florida

where we have concentrations and where significant declines in

home prices have been experienced. Although the following

disclosures address each of these risk characteristics separately,

there is significant overlap in loans with these characteristics,

which contributed to a disproportionate share of the losses in the

portfolio. The residential mortgage loans with all of these higher

risk characteristics comprised six percent of the residential

mortgage portfolio at both December 31, 2011 and 2010, but

accounted for 23 percent of the residential mortgage net charge-

offs in 2011 and 26 percent in 2010.

Residential mortgage loans with a greater than 90 percent but

less than 100 percent refreshed LTV represented 11 percent of

the residential mortgage portfolio at both December 31, 2011 and

2010. Loans with a refreshed LTV greater than 100 percent

represented 26 percent and 24 percent of the residential mortgage

loan portfolio at December 31, 2011 and 2010. Of the loans with

a refreshed LTV greater than 100 percent, 92 percent and 88

percent were performing at December 31, 2011 and 2010. Loans

with a refreshed LTV greater than 100 percent reflect loans where

the outstanding carrying value of the loan is greater than the most

recent valuation of the property securing the loan. The majority of

these loans have a refreshed LTV greater than 100 percent due

primarily to home price deterioration over the past several years.

Loans to borrowers with refreshed FICO scores below 620

represented 15 percent of the residential mortgage portfolio at

both December 31, 2011 and 2010.

Of the $158.5 billion and $180.1 billion in total residential

mortgage loans outstanding at December 31, 2011 and 2010, as

shown in Table 24, 40 percent and 38 percent were originated as

interest-only loans. The outstanding balance of interest-only

residential mortgage loans that have entered the amortization

period was $13.3 billion, or 21 percent, at December 31, 2011.

Residential mortgage loans that have entered the amortization

period have experienced a higher rate of early stage delinquencies

and nonperforming status compared to the residential mortgage

portfolio as a whole. As of December 31, 2011, $484 million, or

four percent, of outstanding residential mortgages that had

entered the amortization period were accruing past due 30 days

or more compared to $4.0 billion, or two percent, of accruing past

due 30 days or more for the entire residential mortgage portfolio.

In addition, at December 31, 2011, $2.0 billion, or 15 percent, of

outstanding residential mortgages that had entered the

amortization period were nonperforming compared to $16.0

billion, or 10 percent, of nonperforming loans for the entire

residential mortgage portfolio. Loans in our interest-only

residential mortgage portfolio have an interest-only period of three

to 10 years and more than 80 percent of these loans will not be

required to make a fully-amortizing payment until 2015 or later.

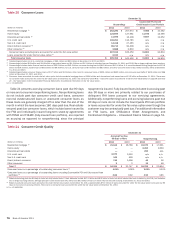

Table 25 presents outstandings, nonperforming loans and net

charge-offs by certain state concentrations for the residential

mortgage portfolio. The Los Angeles-Long Beach-Santa Ana

Metropolitan Statistical Area (MSA) within California represented

12 percent and 13 percent of outstandings at December 31, 2011

and 2010, but comprised only seven percent of net charge-offs

for both 2011 and 2010.

Table 25

(Dollars in millions)

California

Florida

New York

Texas

Virginia

Other U.S./Non-U.S.

Residential mortgage loans (2)

Fully-insured loan portfolio

Countrywide purchased credit-impaired residential mortgage loan portfolio

Total residential mortgage loan portfolio

Residential Mortgage State Concentrations

December 31

Outstandings (1)

2011

$ 54,203

12,338

11,539

7,525

5,709

67,156

$ 158,470

93,854

9,966

$ 262,290

2010

$ 63,677

13,298

12,198

8,466

6,441

76,056

$180,136

67,245

10,592

$257,973

Nonperforming (1)

2011

$ 5,606

1,900

838

425

399

6,802

$ 15,970

2010

$ 6,389

2,054

772

492

450

7,534

$ 17,691

Net Charge-offs

2011

$ 1,326

595

106

55

64

1,686

$ 3,832

2010

$ 1,392

604

44

52

72

1,506

$ 3,670

(1) Outstandings and nonperforming amounts exclude loans accounted for under the fair value option at December 31, 2011. There were no residential mortgage loans accounted for under the fair

value option at December 31, 2010. See Note 23 – Fair Value Option to the Consolidated Financial Statements for additional information on the fair value option.

(2) Amount excludes the Countrywide PCI residential mortgage and fully-insured loan portfolios.