Bank of America 2011 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 95

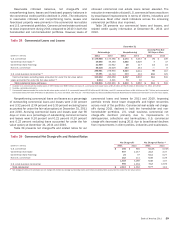

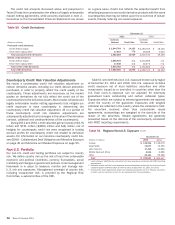

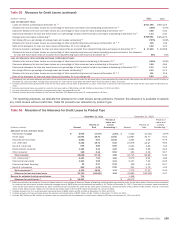

Table 46 presents our commercial TDRs by product type and status. U.S. small business commercial TDRs are comprised of

renegotiated business card loans and are not classified as nonperforming as they are charged off no later than the end of the month

in which the loan becomes 180 days past due.

Table 46

(Dollars in millions)

U.S. commercial

Commercial real estate

Non-U.S. commercial

U.S. small business commercial

Total commercial troubled debt restructurings

Commercial Troubled Debt Restructurings

December 31

2011

Total

$ 1,329

1,675

54

389

$ 3,447

Nonperforming

$531

1,076

38

—

$ 1,645

Performing

$798

599

16

389

$ 1,802

2010

Total

$ 356

815

19

688

$ 1,878

Nonperforming

$ 175

770

7

—

$ 952

Performing

$ 181

45

12

688

$ 926

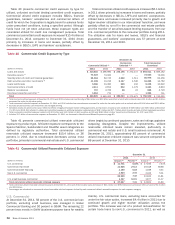

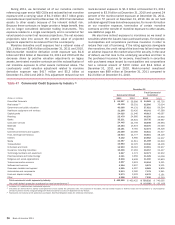

Industry Concentrations

Table 47 presents commercial committed and utilized credit

exposure by industry and the total net credit default protection

purchased to cover the funded and unfunded portions of certain

credit exposures. Our commercial credit exposure is diversified

across a broad range of industries. The increase in commercial

committed exposure of $10.4 billion in 2011 was concentrated

in banks, diversified financials and energy, partially offset by lower

real estate, insurance (including monolines) and other committed

exposure.

Industry limits are used internally to manage industry

concentrations and are based on committed exposures and capital

usage that are allocated on an industry-by-industry basis. A risk

management framework is in place to set and approve industry

limits as well as to provide ongoing monitoring. Management’s

Credit Risk Committee (CRC) oversees industry limit governance.

Diversified financials, our largest industry concentration,

experienced an increase in committed exposure of $8.2 billion, or

nine percent, in 2011 driven primarily by increases in consumer

finance lending and traded products exposure.

Real estate, our second largest industry concentration,

experienced a decrease in committed exposure of $9.4 billion, or

13 percent, in 2011 due primarily to paydowns and sales which

outpaced new originations and renewals. Real estate construction

and land development exposure represented 20 percent and 27

percent of the total real estate industry committed exposure at

December 31, 2011 and 2010. For more information on the

commercial real estate and related portfolios, see Commercial

Real Estate on page 91.

Committed exposure in the banking industry increased $9.1

billion, or 31 percent, in 2011 primarily due to increases in trade

finance as a result of momentum from regional economies and

growth initiatives in foreign markets.

Energy committed exposure increased $5.7 billion, or 22

percent, in 2011 due to increases in working capital lines for state-

related enterprises and increases in large investment-grade energy

companies.

Insurance, including monolines committed exposure,

decreased $8.3 billion, or 34 percent, in 2011 due primarily to

the settlement/termination of monoline positions. For more

information on our monoline exposure, see Monoline and Related

Exposure below.

Other committed exposure decreased $6.0 billion, or 44

percent, in 2011 due to reductions primarily in traded products

exposure.

The Corporation’s committed state and municipal exposure of

$46.1 billion at December 31, 2011 consisted of $34.4 billion of

commercial utilized exposure (including $18.6 billion of funded

loans, $11.3 billion of SBLCs and $4.1 billion of derivative assets)

and unutilized commercial exposure of $11.7 billion (primarily

unfunded loan commitments and letters of credit) and is reported

in the Government and public education industry in Table 47.

Economic conditions continue to impact debt issued by state and

local municipalities and certain exposures to these municipalities.

While historical default rates have been low, as part of our overall

and ongoing risk management processes, we continually monitor

these exposures through a rigorous review process. Additionally,

internal communications surrounding certain at-risk

counterparties and/or sectors are regularly circulated ensuring

exposure levels are in compliance with established concentration

guidelines.

Monoline and Related Exposure

Monoline exposure is reported in the insurance industry and

managed under insurance portfolio industry limits.

We have indirect exposure to monolines primarily in the form

of guarantees supporting our loans, investment portfolios,

securitizations and credit-enhanced securities as part of our public

finance business and other selected products. Such indirect

exposure exists when we purchase credit protection from

monolines to hedge all or a portion of the credit risk on certain

credit exposures including loans and CDOs. We underwrite our

public finance exposure by evaluating the underlying securities.

We also have indirect exposure to monolines in the form of

guarantees supporting our mortgage and other loan sales. Indirect

exposure may exist when credit protection was purchased from

monolines to hedge all or a portion of the credit risk on certain

mortgage and other loan exposures. A loss may occur when we

are required to repurchase a loan and the market value of the loan

has declined, or we are required to indemnify or provide recourse

for a guarantor’s loss. For additional information regarding our

exposure to representations and warranties, see Off-Balance

Sheet Arrangements and Contractual Obligations –

Representations and Warranties on page 50 and Note 9 –

Representations and Warranties Obligations and Corporate

Guarantees to the Consolidated Financial Statements.