Bank of America 2011 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 77

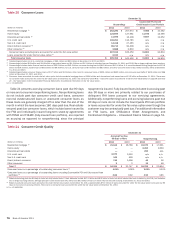

Table 22 presents net charge-offs and related ratios for consumer loans and leases for 2011 and 2010.

Table 22

(Dollars in millions)

Residential mortgage

Home equity

Discontinued real estate

U.S. credit card

Non-U.S. credit card

Direct/Indirect consumer

Other consumer

Total

Consumer Net Charge-offs and Related Ratios

Net Charge-offs

2011

$ 3,832

4,473

92

7,276

1,169

1,476

202

$ 18,520

2010

$ 3,670

6,781

68

13,027

2,207

3,336

261

$ 29,350

Net Charge-off Ratios (1)

2011

1.45%

3.42

0.75

6.90

4.86

1.64

7.32

2.94

2010

1.49%

4.65

0.49

11.04

7.88

3.45

8.89

4.51

(1) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans excluding loans accounted for under the fair value option.

Net charge-off ratios excluding the Countrywide PCI and fully-

insured loan portfolios were 2.27 percent and 1.86 percent for

residential mortgage, 3.77 percent and 5.10 percent for home

equity, 7.14 percent and 4.20 percent for discontinued real estate

and 3.62 percent and 5.08 percent for the total consumer portfolio

for 2011 and 2010. These are the only product classifications

materially impacted by the Countrywide PCI and fully-insured loan

portfolios for 2011 and 2010.

Legacy Asset Servicing within CRES manages our exposures to

certain residential mortgage, home equity and discontinued real

estate products. Legacy Asset Servicing manages both our owned

loans, as well as loans serviced for others, that meet certain

criteria. The criteria generally represent home lending standards

which we do not consider as part of our continuing core business.

The Legacy Asset Servicing portfolio includes the following:

Discontinued real estate loans including subprime and pay

option

Residential mortgage loans and home equity loans for products

we no longer originate including reduced document loans and

interest-only loans not underwritten to fully amortizing payment

Loans that would not have been originated under our

underwriting standards at December 31, 2010 including

conventional loans with an original loan-to-value (LTV) greater

than 95 percent and government-insured loans for which the

borrower has a FICO score less than 620

Countrywide PCI loan portfolios

Certain loans that met a pre-defined delinquency and probability

of default threshold as of January 1, 2011

For more information on Legacy Asset Servicing within CRES,

see page 37.

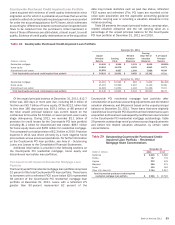

Table 23 presents outstandings, nonperforming balances and

net charge-offs by the Core portfolio and the Legacy Asset Servicing

portfolio for the home loans portfolio.

Table 23

(Dollars in millions)

Core portfolio

Residential mortgage

Home equity

Legacy Asset Servicing portfolio

Residential mortgage (1)

Home equity

Discontinued real estate (1)

Home loans portfolio

Residential mortgage

Home equity

Discontinued real estate

Total home loans portfolio

Home Loans Portfolio

December 31

Outstandings

2011

$ 178,337

67,055

83,953

57,644

11,095

262,290

124,699

11,095

$ 398,084

2010

$166,927

71,519

91,046

66,462

13,108

257,973

137,981

13,108

$409,062

Nonperforming

2011

$ 2,414

439

13,556

2,014

290

15,970

2,453

290

$ 18,713

2010

$ 1,510

107

16,181

2,587

331

17,691

2,694

331

$ 20,716

Net

Charge-offs

2011

$ 348

501

3,484

3,972

92

3,832

4,473

92

$ 8,397

(1) Balances exclude consumer loans accounted for under the fair value option of $906 million for residential mortgage loans and $1.3 billion for discontinued real estate loans at December 31, 2011.

There were no consumer loans accounted for under the fair value option at December 31, 2010. See Note 23 – Fair Value Option to the Consolidated Financial Statements for additional information

on the fair value option.

We believe that the presentation of information adjusted to

exclude the impact of the Countrywide PCI loan portfolio, the fully-

insured loan portfolio and loans accounted for under the fair value

option is more representative of the ongoing operations and credit

quality of the business. As a result, in the following discussions

of the residential mortgage, home equity and discontinued real

estate portfolios, we provide information that excludes the impact

of the Countrywide PCI loan portfolio, the fully-insured loan portfolio

and loans accounted for under the fair value option in certain credit

quality statistics. We separately disclose information on the

Countrywide PCI loan portfolios on page 83.