Bank of America 2011 Annual Report Download - page 186

Download and view the complete annual report

Please find page 186 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

184 Bank of America 2011

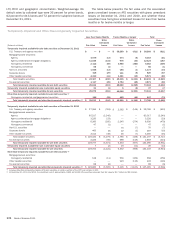

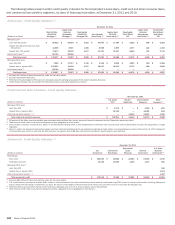

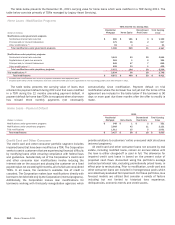

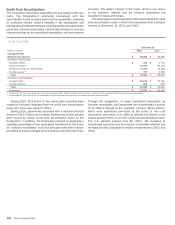

The table below presents the December 31, 2011 carrying value for home loans which were modified in a TDR during 2011. The

table below consists primarily of TDRs managed by Legacy Asset Servicing.

Home Loans - Modification Programs

(Dollars in millions)

Modifications under government programs

Contractual interest rate reduction

Principal and/or interest forbearance

Other modifications (1)

Total modifications under government programs

Modifications under proprietary programs

Contractual interest rate reduction

Capitalization of past due amounts

Principal and/or interest forbearance

Other modifications (1)

Total modifications under proprietary programs

Trial modifications (2)

Total modifications

TDRs Entered into During 2011

Residential

Mortgage

$ 969

179

18

1,166

3,441

381

845

405

5,072

2,634

$ 8,872

Home Equity

$ 181

36

3

220

83

1

47

33

164

96

$ 480

Discontinued

Real Estate

$9

2

—

11

20

2

7

1

30

18

$59

Total Carrying

Value

$ 1,159

217

21

1,397

3,544

384

899

439

5,266

2,748

$ 9,411

(1) Includes other modifications such as term or payment extensions and repayment plans.

(2) Includes $187 million of trial modifications that were considered TDRs prior to the application of new accounting guidance that was effective in 2011.

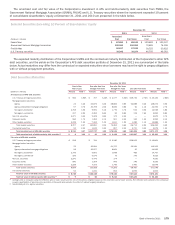

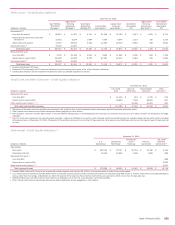

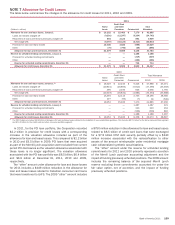

The table below presents the carrying value of loans that

entered into payment default during 2011 and that were modified

in a TDR during the 12 months preceding payment default. A

payment default for home loan TDRs is recognized when a borrower

has missed three monthly payments (not necessarily

consecutively) since modification. Payment default on trial

modification where the borrower has not yet met the terms of the

agreement are included in the table below if the borrower is 90

days or more past due three months after the offer to modify is

made.

Home Loans - Payment Default

(Dollars in millions)

Modifications under government programs

Modifications under proprietary programs

Trial modifications

Total modifications

2011

Residential

Mortgage

$348

2,068

1,011

$ 3,427

Home Equity

$1

42

15

$58

Discontinued

Real Estate

$2

11

5

$18

Total Carrying

Value

$ 351

2,121

1,031

$ 3,503

Credit Card and Other Consumer

The credit card and other consumer portfolio segment includes

impaired loans that have been modified as a TDR. The Corporation

seeks to assist customers that are experiencing financial difficulty

by modifying loans while ensuring compliance with federal laws

and guidelines. Substantially all of the Corporation’s credit card

and other consumer loan modifications involve reducing the

interest rate on the account and placing the customer on a fixed

payment plan not exceeding 60 months, all of which are considered

TDRs. In all cases, the customer’s available line of credit is

canceled. The Corporation makes loan modifications directly with

borrowers for debt held only by the Corporation (internal programs).

Additionally, the Corporation makes loan modifications for

borrowers working with third-party renegotiation agencies which

provide solutions to customers’ entire unsecured debt structures

(external programs).

All credit card and other consumer loans not secured by real

estate, including modified loans, remain on accrual status until

the loan is either charged-off or paid in full. The allowance for

impaired credit card loans is based on the present value of

projected cash flows discounted using the portfolio’s average

contractual interest rate, excluding promotionally priced loans, in

effect prior to restructuring. Prior to modification, credit card and

other consumer loans are included in homogeneous pools which

are collectively evaluated for impairment. For these portfolios, loss

forecast models are utilized that consider a variety of factors

including but not limited to historical loss experience,

delinquencies, economic trends and credit scores.