Bank of America 2011 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

44 Bank of America 2011

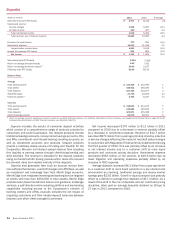

Income tax expense included a $774 million charge to reduce

the carrying value of the deferred tax assets as a result of a

reduction in the U.K. corporate income tax rate enacted during

2011 compared to a charge of $388 million for a rate reduction

enacted in 2010. For additional information related to the U.K.

corporate income tax rate reduction, see Financial Highlights –

Income Tax Expense on page 28.

The return on average economic capital decreased due to lower

net income partially offset by a 33 percent decrease in average

economic capital due to reductions in credit risk driven by improved

risk ratings, lower counterparty credit risk and a decline in market

risk-related trading exposures. Average allocated equity decreased

due to the same reasons as economic capital. For more

information regarding economic capital and allocated equity, see

Supplemental Financial Data on page 32.

Sales and trading revenue and investment banking fees may

continue to be adversely affected in 2012 by lower client activity

and challenging market conditions as a result of, among other

things, the European sovereign debt crisis, uncertainty regarding

the outcome of the evolving domestic regulatory landscape, our

credit ratings and market volatility.

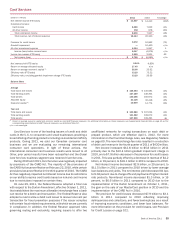

Components of Global Banking & Markets

Sales and Trading Revenue

Sales and trading revenue is segregated into fixed income

including investment and non-investment grade corporate debt

obligations, commercial mortgage-backed securities, residential

mortgage-backed securities (RMBS), swaps and collateralized

debt obligations (CDOs); currencies including interest rate and

foreign exchange contracts; commodities including primarily

futures, forwards and options; and equity income from equity-linked

derivatives and cash equity activity.

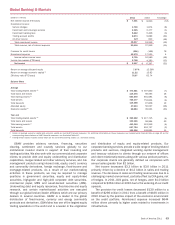

Sales and Trading Revenue (1)

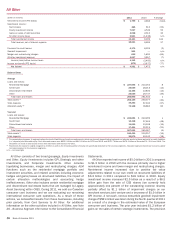

(Dollars in millions)

Fixed income, currencies and commodities

Equity income

Total sales and trading revenue

2011

$ 8,868

3,968

$ 12,836

2010

$ 12,857

4,155

$ 17,012

(1) Includes a FTE adjustment of $202 million and $274 million for 2011 and 2010. For additional

information on sales and trading revenue, including sales and trading investment and brokerage

services and net interest income, see Note 4 – Derivatives to the Consolidated Financial

Statements.

Fixed income, currencies and commodities (FICC) revenue

decreased $4.0 billion, or 31 percent, to $8.9 billion in 2011

compared to 2010 primarily due to lower client activity and

continued adverse market conditions impacting our mortgage

products, credit, and rates and currencies businesses, partially

offset by DVA gains, net of hedges. Equity income decreased $187

million, or five percent, to $4.0 billion in 2011 compared to 2010

primarily due to lower equity derivative trading volumes. Sales and

trading revenue included total commissions and brokerage fee

revenue of $2.3 billion ($2.2 billion from equities and $144 million

from FICC) in 2011 compared to $2.4 billion ($2.2 billion from

equities and $148 million from FICC) in 2010.

In conjunction with regulatory reform measures and our

initiative to optimize our balance sheet, we exited our stand-alone

proprietary trading business as of June 30, 2011, which involved

trading activities in a variety of products, including stocks, bonds,

currencies and commodities. Proprietary trading revenue was

$434 million for the six months ended June 30, 2011 compared

to $1.4 billion for 2010. For additional information on restrictions

on proprietary trading, see Regulatory Matters – Limitations on

Proprietary Trading on page 60.

Investment Banking Fees

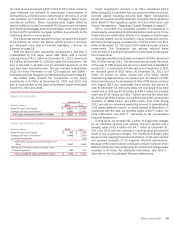

Product specialists within GBAM provide advisory services, and

underwrite and distribute debt and equity issuances and other loan

products. The table below presents total investment banking fees

for GBAM which represent a majority of the Corporation’s total

investment banking income, with the remainder reported in GWIM

and Global Commercial Banking.

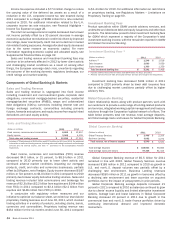

Investment Banking Fees (1)

(Dollars in millions)

Advisory (2)

Debt issuance

Equity issuance

Total investment banking fees

2011

$ 1,246

2,693

1,303

$ 5,242

2010

$ 1,018

3,059

1,329

$ 5,406

(1) Includes self-led deals of $372 million and $264 million for 2011 and 2010.

(2) Advisory includes fees on debt and equity advisory services and mergers and acquisitions.

Investment banking fees decreased $164 million in 2011

compared to 2010 primarily driven by lower debt issuance fees

due to challenging market conditions partially offset by higher

advisory fees.

Global Corporate Banking

Client relationship teams along with product partners work with

our customers to provide a wide range of lending-related products

and services, integrated working capital management and treasury

solutions through the Corporation’s global network of offices. The

table below presents total net revenue, total average deposits,

and total average loans and leases for Global Corporate Banking.

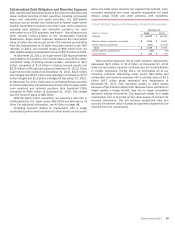

Global Corporate Banking

(Dollars in millions)

Global Treasury Services

Business Lending

Total revenue, net of interest expense

Total average deposits

Total average loans and leases

2011

$ 2,448

3,092

$ 5,540

$ 108,663

97,346

2010

$ 2,259

3,272

$ 5,531

$ 90,083

81,415

Global Corporate Banking revenue of $5.5 billion for 2011

remained in line with 2010. Global Treasury Services revenue

increased $189 million in 2011 compared to 2010 as growth in

U.S. and non-U.S. deposit volumes was partially offset by a

challenging rate environment. Business Lending revenues

decreased $180 million in 2011 as growth in loans was offset by

a declining rate environment and lower accretion on acquired

portfolios due to the impact of prepayments in prior periods.

Global Corporate Banking average deposits increased 21

percent in 2011 compared to 2010 as balances continued to grow

due to clients’ excess liquidity and limited alternative investment

options. Average loan and lease balances in Global Corporate

Banking increased 20 percent in 2011 due to growth in the

commercial loan and non-U.S. trade finance portfolios driven by

continuing international demand and improved domestic

momentum.