Bank of America 2011 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 91

the transfer of securities-based lending loans to the consumer

portfolio earlier in 2011, which together totaled $5.3 billion.

Reservable criticized balances and nonperforming loans and

leases declined $5.5 billion and $1.3 billion in 2011. The declines

were broad-based in terms of clients and industries and were driven

by improved client credit profiles and liquidity. Net charge-offs

decreased $686 million in 2011 due to broad-based declines from

credit quality improvements mentioned above, driving lower charge-

offs and higher recoveries.

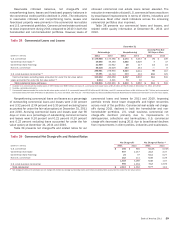

Commercial Real Estate

The commercial real estate portfolio is predominantly managed in

Global Commercial Banking and consists of loans made primarily

to public and private developers, homebuilders and commercial

real estate firms. Outstanding loans decreased $9.8 billion in

2011 due to paydowns and sales, which outpaced new originations

and renewals. Over 90 percent of this decrease occurred within

reservable criticized.

The portfolio remains diversified across property types and

geographic regions. California represented the largest state

concentration of commercial real estate loans and leases at 20

percent and 18 percent at December 31, 2011 and 2010. For

more information on geographic and property concentrations, see

Table 42.

Credit quality for commercial real estate continued to show

signs of improvement; however, we expect that elevated

unemployment and ongoing pressure on vacancy and rental rates

will continue to affect primarily the non-homebuilder portfolio.

Nonperforming commercial real estate loans and foreclosed

properties decreased 31 percent in 2011, split evenly across the

homebuilder and non-homebuilder portfolios. The decline in

nonperforming loans and foreclosed properties in the non-

homebuilder portfolio was driven by decreases in the shopping

centers/retail, land and land development, and office property

types. Reservable criticized balances decreased $9.0 billion

primarily due to declines in the office, shopping centers/retail and

multi-family rental property types in the non-homebuilder portfolio

and improvement in the homebuilder portfolio. Net charge-offs

declined $1.1 billion in 2011 due to improvement in both the

homebuilder and non-homebuilder portfolio.

Table 42 presents outstanding commercial real estate loans

by geographic region which is based on the geographic location of

the collateral and property type. Commercial real estate primarily

includes commercial loans and leases secured by non-owner-

occupied real estate which is dependent on the sale or lease of

the real estate as the primary source of repayment.

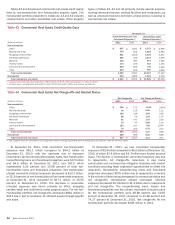

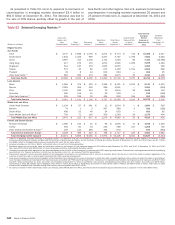

Table 42

(Dollars in millions)

By Geographic Region

California

Northeast

Southwest

Southeast

Midwest

Florida

Illinois

Midsouth

Northwest

Non-U.S.

Other (1)

Total outstanding commercial real estate loans (2)

By Property Type

Non-homebuilder

Office

Multi-family rental

Shopping centers/retail

Industrial/warehouse

Multi-use

Hotels/motels

Land and land development

Other

Total non-homebuilder

Homebuilder

Total outstanding commercial real estate loans (2)

Outstanding Commercial Real Estate Loans

December 31

2011

$ 7,957

6,554

5,243

4,844

4,051

2,502

1,871

1,751

1,574

1,824

1,425

$39,596

$ 7,571

6,105

5,985

3,988

3,218

2,653

1,599

6,050

37,169

2,427

$39,596

2010

$ 9,012

7,639

6,169

5,806

5,301

3,649

2,811

2,627

2,243

2,515

1,701

$ 49,473

$ 9,688

7,721

7,484

5,039

4,266

2,650

2,376

5,950

45,174

4,299

$ 49,473

(1) Other states primarily represents properties in the states of Colorado, Utah, Hawaii, Wyoming and Montana.

(2) Includes commercial real estate loans accounted for under the fair value option of $79 million at December 31, 2010, none at December 31, 2011.

During 2011, we continued to see improvement in the

homebuilder portfolio. Certain portions of the non-homebuilder

portfolio remain at risk as occupancy rates, rental rates and

commercial property prices remain under pressure. We use a

number of proactive risk mitigation initiatives to reduce utilized

and potential exposure in the commercial real estate portfolios

including refinement of our credit standards, additional transfers

of deteriorating exposures to management by independent special

asset officers and the pursuit of alternative resolution methods

to achieve the best results for our customers and the Corporation.