Bank of America 2011 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

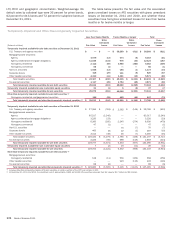

178 Bank of America 2011

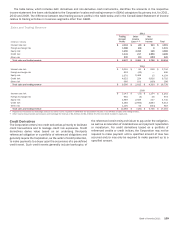

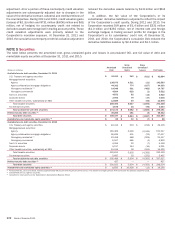

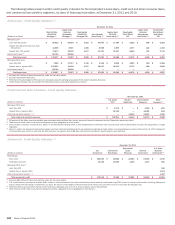

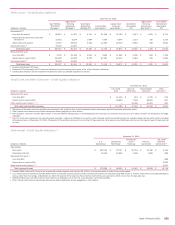

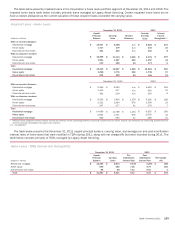

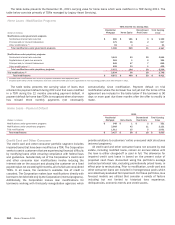

(Dollars in millions)

Home loans

Core portfolio

Residential mortgage (5)

Home equity

Legacy Asset Servicing portfolio

Residential mortgage

Home equity

Discontinued real estate (6)

Credit card and other consumer

U.S. credit card

Non-U.S. credit card

Direct/Indirect consumer (7)

Other consumer (8)

Total consumer

Commercial

U.S. commercial

Commercial real estate (9)

Commercial lease financing

Non-U.S. commercial

U.S. small business commercial

Total commercial loans

Commercial loans accounted for

under the fair value option (10)

Total commercial

Total loans and leases

Percentage of outstandings

December 31, 2010

30-59 Days

Past Due (1)

$ 1,160

186

3,999

1,096

68

1,398

439

1,086

65

9,497

432

250

82

25

189

978

978

$ 10,475

1.11%

60-89 Days

Past Due (1)

$ 236

12

2,879

792

39

1,195

316

522

25

6,016

222

70

18

2

158

470

470

$ 6,486

0.69%

90 Days or

More

Past Due (2)

$ 1,255

105

31,985

2,186

419

3,320

599

1,104

50

41,023

3,689

5,876

135

239

529

10,468

10,468

$ 51,491

5.48%

Total Past

Due 30 Days

or More

$ 2,651

303

38,863

4,074

526

5,913

1,354

2,712

140

56,536

4,343

6,196

235

266

876

11,916

11,916

$ 68,452

7.28%

Total Current

or Less Than

30 Days

Past Due (3)

$ 164,276

71,216

41,591

49,798

930

107,872

26,111

87,596

2,690

552,080

171,241

43,036

21,707

31,722

13,843

281,549

281,549

$ 833,629

88.64%

Purchased

Credit-

impaired (4)

$—

—

10,592

12,590

11,652

—

—

—

—

34,834

2

161

—

41

—

204

204

$ 35,038

3.73%

Loans

Accounted

for Under

the Fair

Value Option

$ 3,321

3,321

$ 3,321

0.35%

Total

Outstandings

$ 166,927

71,519

91,046

66,462

13,108

113,785

27,465

90,308

2,830

643,450

175,586

49,393

21,942

32,029

14,719

293,669

3,321

296,990

$ 940,440

(1) Home loans includes $2.4 billion of fully-insured loans, $818 million of nonperforming loans and $156 million of TDRs that were removed from the Countrywide PCI loan portfolio prior to the adoption

of accounting guidance on PCI loans effective January 1, 2010.

(2) Home loans includes $16.8 billion of fully-insured loans and $372 million of TDRs that were removed from the Countrywide PCI loan portfolio prior to the adoption of accounting guidance on PCI

loans effective January 1, 2010.

(3) Home loans includes $1.1 billion of nonperforming loans as all principal and interest are not current or the loans are TDRs that have not demonstrated sustained repayment performance.

(4) PCI loan amounts are shown gross of the valuation allowance and exclude $1.6 billion of PCI home loans from the Merrill Lynch acquisition which are included in their appropriate aging categories.

(5) Total outstandings includes non-U.S. residential mortgages of $90 million at December 31, 2010.

(6) Total outstandings includes $11.8 billion of pay option loans and $1.3 billion of subprime loans at December 31, 2010. The Corporation no longer originates these products.

(7) Total outstandings includes dealer financial services loans of $43.3 billion, consumer lending loans of $12.4 billion, U.S. securities-based lending margin loans of $16.6 billion, student loans of

$6.8 billion, non-U.S. consumer loans of $8.0 billion and other consumer loans of $3.2 billion at December 31, 2010.

(8) Total outstandings includes consumer finance loans of $1.9 billion, other non-U.S. consumer loans of $803 million and consumer overdrafts of $88 million at December 31, 2010.

(9) Total outstandings includes U.S. commercial real estate loans of $46.9 billion and non-U.S. commercial real estate loans of $2.5 billion at December 31, 2010.

(10) Certain commercial loans are accounted for under the fair value option and include U.S. commercial loans of $1.6 billion, non-U.S. commercial loans of $1.7 billion and commercial real estate loans

of $79 million at December 31, 2010. See Note 22 – Fair Value Measurements and Note 23 – Fair Value Option for additional information.

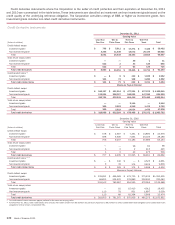

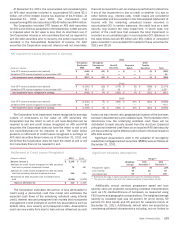

The Corporation mitigates a portion of its credit risk on the

residential mortgage portfolio through the use of synthetic

securitization vehicles. These vehicles issue long-term notes to

investors, the proceeds of which are held as cash collateral. The

Corporation pays a premium to the vehicles to purchase mezzanine

loss protection on a portfolio of residential mortgages owned by

the Corporation. Cash held in the vehicles is used to reimburse

the Corporation in the event that losses on the mortgage portfolio

exceed 10 basis points (bps) of the original pool balance, up to

the remaining amount of purchased loss protection of $783 million

and $1.1 billion at December 31, 2011 and 2010. The vehicles

from which the Corporation purchases credit protection are VIEs.

The Corporation does not have a variable interest in these vehicles.

Accordingly, these vehicles are not consolidated by the

Corporation. Amounts due from the vehicles are recorded in other

income (loss) when the Corporation recognizes a reimbursable

loss, as described above. Amounts are collected when

reimbursable losses are realized through the sale of the underlying

collateral. At December 31, 2011 and 2010, the Corporation had

a receivable of $359 million and $722 million from these vehicles

for reimbursement of losses, and principal of $23.9 billion and

$53.9 billion of residential mortgage loans was referenced under

these agreements. The Corporation records an allowance for credit

losses on these loans without regard to the existence of the

purchased loss protection as the protection does not represent a

guarantee of individual loans.

In addition, the Corporation has entered into long-term credit

protection agreements with FNMA and FHLMC on principal totaling

$23.8 billion and $12.9 billion at December 31, 2011 and 2010,

providing full protection on residential mortgage loans that become

severely delinquent. All of these loans are individually insured and

therefore the Corporation does not record an allowance for credit

losses related to these loans.

Nonperforming Loans and Leases

The Credit Quality table presents the Corporation’s nonperforming

loans and leases including nonperforming TDRs and loans

accruing past due 90 days or more at December 31, 2011 and

2010. Nonperforming loans and leases exclude performing TDRs

and loans accounted for under the fair value option. Nonperforming

LHFS are excluded from nonperforming loans and leases as they

are recorded at either fair value or the lower of cost or fair value.