Bank of America 2011 Annual Report Download - page 218

Download and view the complete annual report

Please find page 218 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

216 Bank of America 2011

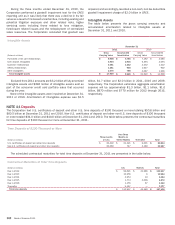

and $139.5 billion. The Corporation does not expect to make

material payments in connection with these guarantees.

Other Derivative Contracts

The Corporation funds selected assets, including securities issued

by CDOs and CLOs, through derivative contracts, typically total

return swaps, with third parties and VIEs that are not consolidated

on the Corporation’s Consolidated Balance Sheet. At December

31, 2011 and 2010, the total notional amount of these derivative

contracts was approximately $3.2 billion and $4.3 billion with

commercial banks and $1.8 billion and $1.7 billion with VIEs. The

underlying securities are senior securities and substantially all of

the Corporation’s exposures are insured. Accordingly, the

Corporation’s exposure to loss consists principally of counterparty

risk to the insurers. In certain circumstances, generally as a result

of ratings downgrades, the Corporation may be required to

purchase the underlying assets, which would not result in

additional gain or loss to the Corporation as such exposure is

already reflected in the fair value of the derivative contracts.

Other Guarantees

The Corporation sells products that guarantee the return of

principal to investors at a preset future date. These guarantees

cover a broad range of underlying asset classes and are designed

to cover the shortfall between the market value of the underlying

portfolio and the principal amount on the preset future date. To

manage its exposure, the Corporation requires that these

guarantees be backed by structural and investment constraints

and certain pre-defined triggers that would require the underlying

assets or portfolio to be liquidated and invested in zero-coupon

bonds that mature at the preset future date. The Corporation is

required to fund any shortfall between the proceeds of the

liquidated assets and the purchase price of the zero-coupon bonds

at the preset future date. These guarantees are recorded as

derivatives and carried at fair value in the trading portfolio. At

December 31, 2011 and 2010, the notional amount of these

guarantees totaled $300 million and $666 million. These

guarantees have various maturities ranging from two to five years.

As of December 31, 2011 and 2010, the Corporation had not

made a payment under these products and has assessed the

probability of payments under these guarantees as remote.

The Corporation has entered into additional guarantee

agreements and commitments, including lease-end obligation

agreements, partial credit guarantees on certain leases, real

estate joint venture guarantees, sold risk participation swaps,

divested business commitments and sold put options that require

gross settlement. The maximum potential future payment under

these agreements was approximately $3.7 billion and $3.4 billion

at December 31, 2011 and 2010. The estimated maturity dates

of these obligations extend up to 2033. The Corporation has made

no material payments under these guarantees.

In the normal course of business, the Corporation periodically

guarantees the obligations of its affiliates in a variety of

transactions including ISDA-related transactions and non ISDA-

related transactions such as commodities trading, repurchase

agreements, prime brokerage agreements and other transactions.

Payment Protection Insurance Claims Matter

In the U.K., the Corporation sells payment protection insurance

(PPI) through its international card services business to credit card

customers and has previously sold this insurance to consumer

loan customers. PPI covers a consumer’s loan for debt repayment

if certain events occur such as loss of job or illness. In response

to an elevated level of customer complaints of misleading sales

tactics across the industry, heightened media coverage and

pressure from consumer advocacy groups, the U.K. Financial

Services Authority (FSA) investigated and raised concerns about

the way some companies have handled complaints relating to the

sale of these insurance policies. In August 2010, the FSA issued

a policy statement (the FSA Policy Statement) on the assessment

and remediation of PPI claims that is applicable to the

Corporation’s U.K. consumer businesses and is intended to

address concerns among consumers and regulators regarding the

handling of PPI complaints across the industry. The FSA Policy

Statement sets standards for the sale of PPI that apply to current

and prior sales, and in the event a company does not or did not

comply with the standards, it is alleged that the insurance was

incorrectly sold, giving the customer rights to remedies. The FSA

Policy Statement also requires companies to review their sales

practices and to proactively remediate non-complaining customers

if evidence of a systematic breach of the newly articulated sales

standards is discovered, which could include refunding premiums

paid.

In October 2010, the British Bankers’ Association (BBA), on

behalf of its members, including the Corporation, challenged the

provisions of the FSA Policy Statement and its retroactive

application to sales of PPI to U.K. consumers through a judicial

review process against the FSA and the U.K. Financial Ombudsman

Service. On April 20, 2011, the U.K. court issued a judgment

upholding the FSA Policy Statement as promulgated and

dismissing the BBA’s challenge. The BBA did not appeal the

decision. Following the conclusion of the judicial review and the

subsequent completion of the detailed root cause analysis as

required by the FSA Policy Statement, the Corporation reassessed

its reserve for PPI claims during 2010. The total accrued liability

was $476 million and $700 million at December 31, 2011 and

2010.

Litigation and Regulatory Matters

In the ordinary course of business, the Corporation and its

subsidiaries are routinely defendants in or parties to many pending

and threatened legal actions and proceedings, including actions

brought on behalf of various classes of claimants. These actions

and proceedings are generally based on alleged violations of

consumer protection, securities, environmental, banking,

employment, contract and other laws. In some of these actions

and proceedings, claims for substantial monetary damages are

asserted against the Corporation and its subsidiaries.

In the ordinary course of business, the Corporation and its

subsidiaries are also subject to regulatory examinations,

information gathering requests, inquiries and investigations.

Certain subsidiaries of the Corporation are registered broker/

dealers or investment advisors and are subject to regulation by