Bank of America 2011 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 39

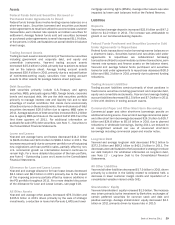

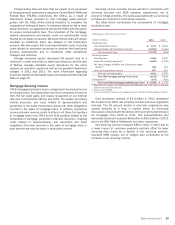

Compensatory fees are fees that we expect to be assessed

by the government-sponsored enterprises, Fannie Mae (FNMA) and

Freddie Mac (FHLMC) (collectively, the GSEs), as a result of

foreclosure delays pursuant to first mortgage seller/servicer

guides with the GSEs which provide timelines to complete the

liquidation of delinquent loans. In instances where we fail to meet

these timelines, our agreements provide the GSEs with the option

to assess compensatory fees. The remainder of the mortgage-

related assessments and waivers costs are out-of-pocket costs

that we do not expect to recover. We expect these costs will remain

elevated as additional loans are delayed in the foreclosure

process. We also expect that continued elevated costs, including

costs related to resources necessary to perform the foreclosure

process assessments and to implement other operational

changes, will continue.

Average economic capital decreased 30 percent due to a

reduction in credit risk driven by lower loan balances, and the sale

of Balboa. Average allocated equity decreased for the same

reasons as economic capital as well as the goodwill impairment

charges in 2011 and 2010. For more information regarding

economic capital and allocated equity, see Supplemental Financial

Data on page 32.

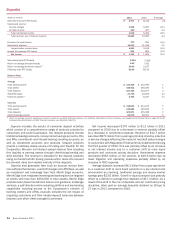

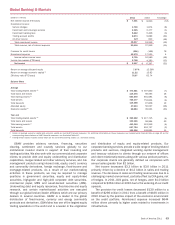

Mortgage Banking Income

CRES mortgage banking income is categorized into production and

servicing income. Core production income is comprised of revenue

from the fair value gains and losses recognized on our interest

rate lock commitments (IRLCs) and LHFS, the related secondary

market execution, and costs related to representations and

warranties in the sales transactions along with other obligations

incurred in the sales of mortgage loans. In addition, production

income includes revenue, which is offset in All Other, for transfers

of mortgage loans from CRES to the ALM portfolio related to the

Corporation’s mortgage production retention decisions. Ongoing

costs related to representations and warranties and other

obligations that were incurred in the sales of mortgage loans in

prior periods are also included in production income.

Servicing income includes income earned in connection with

servicing activities and MSR valuation adjustments, net of

economic hedge activities. The costs associated with our servicing

activities are included in noninterest expense.

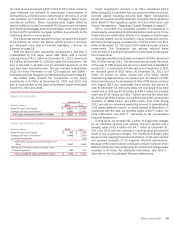

The table below summarizes the components of mortgage

banking income.

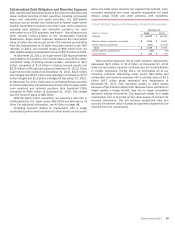

Mortgage Banking Income

(Dollars in millions)

Production loss:

Core production revenue

Representations and warranties provision

Total production loss

Servicing income:

Servicing fees

Impact of customer payments (1)

Fair value changes of MSRs, net of economic hedge

results (2)

Other servicing-related revenue

Total net servicing income

Total CRES mortgage banking income (loss)

Eliminations (3)

Total consolidated mortgage banking income (loss)

2011

$ 2,797

(15,591)

(12,794)

5,959

(2,621)

656

607

4,601

(8,193)

(637)

$ (8,830)

2010

$ 6,182

(6,785)

(603)

6,475

(3,759)

376

675

3,767

3,164

(430)

$ 2,734

(1) Represents the change in the market value of the MSR asset due to the impact of customer

payments received during the year.

(2) Includes sale of MSRs.

(3) Includes the effect of transfers of mortgage loans from CRES to the ALM portfolio in All Other.

Core production revenue of $2.8 billion in 2011 decreased

$3.4 billion from 2010 due primarily to lower new loan origination

volumes. The 52 percent decline in new loan originations was

caused primarily by a drop in market share, as previously

discussed, combined with the decline in the overall market demand

for mortgages from 2010 to 2011. The representations and

warranties provision increased $8.8 billion to $15.6 billion in 2011

due to the BNY Mellon Settlement and other exposures.

Net servicing income increased $834 million in 2011 due to

a lower impact of customer payments partially offset by lower

servicing fees driven by a decline in the servicing portfolio.

Improved MSR results, net of hedges also contributed to the

increase in net servicing income.