Bank of America 2011 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

54 Bank of America 2011

estimated range of possible loss. Additionally, if recent court

rulings related to monoline litigation, including one related to us,

that have allowed sampling of loan files instead of requiring a loan-

by-loan review to determine if a representations and warranties

breach has occurred are followed generally by the courts, private-

label securitization investors may view litigation as a more

attractive alternative as compared to a loan-by-loan review. For

additional information regarding these issues, see MBIA litigation

in Litigation and Regulatory Matters in Note 14 – Commitments

and Contingencies to the Consolidated Financial Statements.

Finally, although we believe that the representations and

warranties typically given in non-GSE transactions are less rigorous

and actionable than those given in GSE transactions, we do not

have significant loan-level experience in non-GSE transactions to

measure the impact of these differences on the probability that a

loan will be required to be repurchased.

The liability for obligations under representations and

warranties with respect to GSE and non-GSE exposures and the

corresponding estimated range of possible loss for non-GSE

representations and warranties exposures do not include any

losses related to litigation matters disclosed in Note 14 –

Commitments and Contingencies to the Consolidated Financial

Statements, nor do they include any separate foreclosure costs

and related costs, assessments and compensatory fees or any

possible losses related to potential claims for breaches of

performance of servicing obligations (except as such losses are

included as potential costs of the BNY Mellon Settlement),

potential securities law or fraud claims or potential indemnity or

other claims against us, including claims related to loans insured

by the FHA. We are not able to reasonably estimate the amount

of any possible loss with respect to any such servicing, securities

law (except to the extent reflected in the aggregate range of

possible loss for litigation and regulatory matters disclosed in Note

14 – Commitments and Contingencies to the Consolidated Financial

Statements), fraud or other claims against us; however, such loss

could be material.

Government-sponsored Enterprises Experience

Our current repurchase claims experience with the GSEs is

predominantly concentrated in the 2004 through 2008 origination

vintages where we believe that our exposure to representations

and warranties liability is most significant. Our repurchase claims

experience related to loans originated prior to 2004 has not been

significant and we believe that the changes made to our operations

and underwriting policies have reduced our exposure related to

loans originated after 2008.

Bank of America and legacy Countrywide sold approximately

$1.1 trillion of loans originated from 2004 through 2008 to the

GSEs. As of December 31, 2011, 11 percent of the loans in these

vintages have defaulted or are 180 days or more past due (severely

delinquent). At least 25 payments have been made on

approximately 65 percent of severely delinquent or defaulted

loans. Through December 31, 2011, we have received $32.4

billion in repurchase claims associated with these vintages,

representing approximately three percent of the loans sold to the

GSEs in these vintages. Including the agreement reached with

FNMA on December 31, 2010, we have resolved $25.7 billion of

these claims with a net loss experience of approximately 31

percent. The claims resolved and the loss rate do not include $839

million in claims extinguished as a result of the agreement with

FHLMC due to the global nature of the agreement and, specifically,

the absence of a formal apportionment of the agreement amount

between current and future claims. Our collateral loss severity rate

on approved repurchases has averaged approximately 45 to 55

percent.

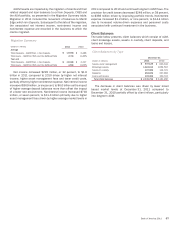

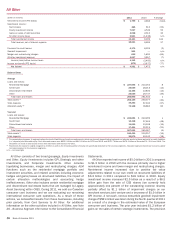

Table 11 highlights our experience with the GSEs related to

loans originated from 2004 through 2008. Outstanding GSE

claims increased to $6.3 billion, primarily attributable to $14.3

billion in new repurchase claims submitted by the GSEs for both

legacy Countrywide originations not covered by the GSE

Agreements and legacy Bank of America originations. The high

level of new claims was partially offset by the resolution of claims

with the GSEs.

Table 11

(Dollars in billions)

Original funded balance

Principal payments

Defaults

Total outstanding balance at December 31, 2011

Outstanding principal balance 180 days or more past due (severely delinquent)

Defaults plus severely delinquent

Payments made by borrower:

Less than 13

13-24

25-36

More than 36

Total payments made by borrower

Outstanding GSE representations and warranties claims (all vintages)

As of December 31, 2010

As of December 31, 2011

Cumulative GSE representations and warranties losses (2004-2008 vintages)

Overview of GSE Balances – 2004-2008 Originations

Legacy Originator

Countrywide

$ 846

(452)

(56)

$338

$50

106

Other

$ 272

(153)

(9)

$110

$12

21

Total

$ 1,118

(605)

(65)

$448

$62

127

$15

30

34

48

$127

$ 2.8

6.3

$ 9.2

Percent of

Total

12%

23

27

38

100%