Bank of America 2011 Annual Report Download - page 217

Download and view the complete annual report

Please find page 217 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 215

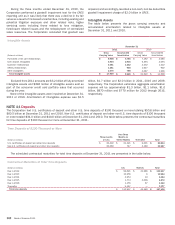

The Corporation has entered into agreements with providers of

market data, communications, systems consulting and other

office-related services. At December 31, 2011 and 2010, the

minimum fee commitments over the remaining terms of these

agreements totaled $1.9 billion and $2.1 billion.

Other Guarantees

Bank-owned Life Insurance Book Value Protection

The Corporation sells products that offer book value protection to

insurance carriers who offer group life insurance policies to

corporations, primarily banks. The book value protection is

provided on portfolios of intermediate investment-grade fixed-

income securities and is intended to cover any shortfall in the

event that policyholders surrender their policies and market value

is below book value. To manage its exposure, the Corporation

imposes significant restrictions on surrenders and the manner in

which the portfolio is liquidated and the funds are accessed. In

addition, investment parameters of the underlying portfolio are

restricted. These constraints, combined with structural

protections, including a cap on the amount of risk assumed on

each policy, are designed to provide adequate buffers and guard

against payments even under extreme stress scenarios. These

guarantees are recorded as derivatives and carried at fair value

in the trading portfolio. At both December 31, 2011 and 2010,

the notional amount of these guarantees totaled $15.8 billion and

the Corporation’s maximum exposure related to these guarantees

totaled $5.1 billion and $5.0 billion with estimated maturity dates

between 2030 and 2040. As of December 31, 2011, the

Corporation had not made a payment under these products. The

possibility of surrender or other payment associated with these

guarantees exists. The net fair value of the liability associated with

these guarantees was $48 million and $78 million at December

31, 2011 and 2010 and reflects the probability of surrender as

well as the multiple structural protection features in the contracts.

Employee Retirement Protection

The Corporation sells products that offer book value protection

primarily to plan sponsors of the Employee Retirement Income

Security Act of 1974 (ERISA) governed pension plans, such as 401

(k) plans and 457 plans. The book value protection is provided on

portfolios of intermediate/short-term investment-grade fixed-

income securities and is intended to cover any shortfall in the

event that plan participants continue to withdraw funds after all

securities have been liquidated and there is remaining book value.

The Corporation retains the option to exit the contract at any time.

If the Corporation exercises its option, the purchaser can require

the Corporation to purchase high-quality fixed-income securities,

typically government or government-backed agency securities, with

the proceeds of the liquidated assets to assure the return of

principal. To manage its exposure, the Corporation imposes

significant restrictions and constraints on the timing of the

withdrawals, the manner in which the portfolio is liquidated and

the funds are accessed, and the investment parameters of the

underlying portfolio. These constraints, combined with structural

protections, are designed to provide adequate buffers and guard

against payments even under extreme stress scenarios. These

guarantees are recorded as derivatives and carried at fair value

in the trading portfolio. At December 31, 2011 and 2010, the

notional amount of these guarantees totaled $28.8 billion and

$33.8 billion with estimated maturity dates up to 2015 if the exit

option is exercised on all deals. As of December 31, 2011, the

Corporation had not made a payment under these products.

Indemnifications

In the ordinary course of business, the Corporation enters into

various agreements that contain indemnifications, such as tax

indemnifications, whereupon payment may become due if certain

external events occur, such as a change in tax law. The

indemnification clauses are often standard contractual terms and

were entered into in the normal course of business based on an

assessment that the risk of loss would be remote. These

agreements typically contain an early termination clause that

permits the Corporation to exit the agreement upon these events.

The maximum potential future payment under indemnification

agreements is difficult to assess for several reasons, including

the occurrence of an external event, the inability to predict future

changes in tax and other laws, the difficulty in determining how

such laws would apply to parties in contracts, the absence of

exposure limits contained in standard contract language and the

timing of the early termination clause. Historically, any payments

made under these guarantees have been de minimis. The

Corporation has assessed the probability of making such

payments in the future as remote.

Merchant Services

During 2009, the Corporation contributed its merchant services

business to a joint venture in exchange for a 46.5 percent

ownership interest in the joint venture. In 2010, the joint venture

purchased the interest held by one of the three initial investors

bringing the Corporation’s ownership interest up to 49 percent.

For additional information on the joint venture agreement, see Note

5 – Securities.

In accordance with credit and debit card association rules, the

Corporation sponsors merchant processing servicers that process

credit and debit card transactions on behalf of various merchants.

In connection with these services, a liability may arise in the event

of a billing dispute between the merchant and a cardholder that

is ultimately resolved in the cardholder’s favor. If the merchant

defaults on its obligation to reimburse the cardholder, the

cardholder, through its issuing bank, generally has until six months

after the date of the transaction to present a chargeback to the

merchant processor, which is primarily liable for any losses on

covered transactions. However, if the merchant processor fails to

meet its obligation to reimburse the cardholder for disputed

transactions, then the Corporation, as the sponsor, could be held

liable for the disputed amount. In 2011 and 2010, the sponsored

entities processed and settled $460.4 billion and $339.4 billion

of transactions and recorded losses of $11 million and $17 million.

At December 31, 2011 and 2010, the Corporation held as

collateral $238 million and $25 million of merchant escrow

deposits which may be used to offset amounts due from the

individual merchants.

The Corporation believes that the maximum potential exposure

is not representative of the actual potential loss exposure. The

Corporation believes the maximum potential exposure for

chargebacks would not exceed the total amount of merchant

transactions processed through Visa, MasterCard and Discover

for the last six months, which represents the claim period for the

cardholder, plus any outstanding delayed-delivery transactions. As

of December 31, 2011 and 2010, the maximum potential exposure

for sponsored transactions totaled approximately $236.0 billion