Bank of America 2011 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 121

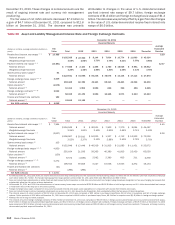

2010 Compared to 2009

The following discussion and analysis provides a comparison of

our results of operations for 2010 and 2009. This discussion

should be read in conjunction with the Consolidated Financial

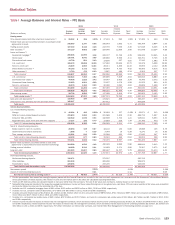

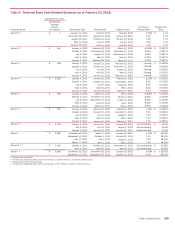

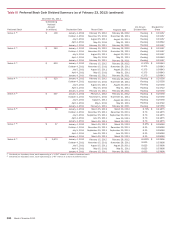

Statements and related Notes. Tables 7 and 8 contain financial

data to supplement this discussion.

Overview

Net Income/Loss

Net loss totaled $2.2 billion in 2010 compared to net income of

$6.3 billion in 2009. Including preferred stock dividends, the net

loss applicable to common shareholders was $3.6 billion, or

$(0.37) per diluted share. Those results compared to a net loss

applicable to common shareholders of $2.2 billion, or $(0.29) per

diluted share for 2009.

Net Interest Income

Net interest income on a FTE basis increased $4.3 billion to $52.7

billion for 2010 compared to 2009. The increase was due to the

impact of deposit pricing and the adoption of new consolidation

guidance which contributed $10.5 billion to net interest income

in 2010. The increase was partially offset by lower commercial

and consumer loan levels, the sale of First Republic in 2010 and

lower rates on core assets and trading assets and liabilities,

including derivative exposures. The net interest yield on a FTE

basis increased 13 bps to 2.78 percent for 2010 compared to

2009 due to the factors described above.

Noninterest Income

Noninterest income decreased $13.8 billion to $58.7 billion in

2010 compared to 2009. Card income decreased $245 million

due to the implementation of the CARD Act partially offset by the

impact of the new consolidation guidance and higher interchange

income. Service charges decreased $1.6 billion largely due to the

impact of overdraft policy changes in conjunction with Regulation

E, which became effective in the third quarter of 2010 and the

impact of our overdraft policy changes implemented in late 2009.

Equity investment income decreased $4.8 billion, as net gains on

the sales of certain strategic investments during 2010 were less

than gains in 2009 that included a $7.3 billion gain related to the

sale of a portion of our investment in CCB. Trading account profits

decreased $2.2 billion due to more favorable market conditions

in 2009 and investor concerns regarding sovereign debt fears and

regulatory uncertainty. DVA gains, net of hedges, on derivative

liabilities of $262 million for 2010 compared to losses of $662

million for 2009. Mortgage banking income decreased $6.1 billion

due to an increase of $4.9 billion in representations and warranties

provision and lower volume and margins. Gains on sales of debt

securities decreased $2.2 billion driven by a lower volume of sales

of debt securities. The decrease also included the impact of losses

in 2010 related to portfolio restructuring activities. Other income

(loss) improved by $2.4 billion. 2009 included a net negative fair

value adjustment related to our own credit of $4.9 billion on

structured liabilities compared to a net positive adjustment of $18

million in 2010, and 2009 also included a $3.8 billion gain on the

contribution of our merchant services business to a joint venture.

Legacy asset write-downs included in other income (loss) were

$1.7 billion in 2009 compared to net gains of $256 million in

2010. Impairment losses recognized in earnings on AFS debt

securities decreased $1.9 billion reflecting lower impairment write-

downs on non-agency RMBS and CDOs.

Provision for Credit Losses

The provision for credit losses decreased $20.1 billion to $28.4

billion for 2010 compared to 2009 due to improving portfolio

trends across the consumer and commercial portfolios. Net

charge-offs totaled $34.3 billion, or 3.60 percent of average loans

and leases for 2010 compared to $33.7 billion, or 3.58 percent

for 2009.

Noninterest Expense

Noninterest expense increased $16.4 billion to $83.1 billion for

2010 compared to 2009 largely due to goodwill impairment

charges of $12.4 billion. The increase was also driven by a $3.6

billion increase in personnel costs reflecting the build out of several

businesses, the recognition of expense on proportionally larger

2009 incentive deferrals and the U.K. payroll tax on certain year-

end incentive payments, as well as a $1.6 billion increase in

litigation costs. These increases were partially offset by a $901

million decline in merger and restructuring charges compared to

2009. Noninterest expense for 2009 included a special FDIC

assessment of $724 million.

Income Tax Expense

Income tax expense was $915 million for 2010 compared to a

benefit of $1.9 billion for 2009. The effective tax rate in 2010 was

not meaningful due to the impact of non-deductible goodwill

impairment charges of $12.4 billion. The effective tax rate for

2010 excluding goodwill impairment charges was 8.3 percent

compared to (44.0) percent in 2009. The change in the effective

tax rate from the prior year was primarily driven by an increase in

pre-tax income excluding the non-deductible goodwill impairment

charges. Also impacting the 2010 effective tax rate was a $392

million charge from a U.K. law change and a $1.7 billion tax benefit

from the release of a portion of the deferred tax asset valuation

allowance related to acquired capital loss carryforward tax benefits

compared to $650 million in 2009.

Business Segment Operations

Deposits

Net income decreased $1.3 billion to $1.4 billion in 2010 due to

a decline in revenue and higher noninterest expense. Net interest

income increased $1.1 billion to $8.3 billion as a result of a

customer shift to more liquid products and continued pricing

discipline, partially offset by a lower net interest income allocation

related to ALM activities. Noninterest income decreased $1.8

billion to $5.3 billion driven by the impact of overdraft policy

changes in conjunction with Regulation E, which was effective in

the third quarter of 2010, and our overdraft policy changes

implemented in late 2009. Noninterest expense increased $1.5

billion to $11.2 billion as a higher proportion of banking center

sales and service costs was aligned to Deposits from the other

segments, and increased litigation expenses partially offset by a

decrease in FDIC expenses as 2009 included a special

assessment.