Bank of America 2011 Annual Report Download - page 249

Download and view the complete annual report

Please find page 249 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 247

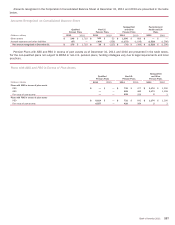

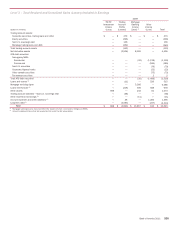

The Corporation concluded that no valuation allowance is

necessary to reduce the U.K. NOLs, U.S. NOL and general business

credit carryforwards since estimated future taxable income will be

sufficient to utilize these assets prior to their expiration. During

2011, the valuation allowance decreased due to the utilization of

the remaining acquired capital loss carryforward and increased

primarily against net operating loss carryforwards in non-U.S. and

state jurisdictions.

At December 31, 2011 and 2010, U.S. federal income taxes

had not been provided on $18.5 billion and $17.9 billion of

undistributed earnings of non-U.S. subsidiaries earned prior to

1987 and after 1997 that have been reinvested for an indefinite

period of time. If the earnings were distributed, an additional $2.5

billion and $2.6 billion of tax expense, net of credits for non-U.S.

taxes paid on such earnings and for the related non-U.S.

withholding taxes, would have resulted as of December 31, 2011

and 2010.

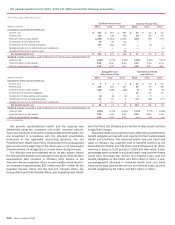

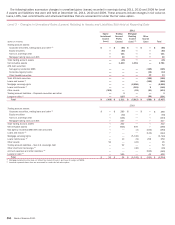

NOTE 22 Fair Value Measurements

Under applicable accounting guidance, fair value is defined as the

exchange price that would be received for an asset or paid to

transfer a liability (an exit price) in the principal or most

advantageous market for the asset or liability in an orderly

transaction between market participants on the measurement

date. The Corporation determines the fair values of its financial

instruments based on the fair value hierarchy established under

applicable accounting guidance which requires an entity to

maximize the use of observable inputs and minimize the use of

unobservable inputs when measuring fair value. There are three

levels of inputs used to measure fair value. For more information

regarding the fair value hierarchy and how the Corporation

measures fair value, see Note 1 – Summary of Significant

Accounting Principles. The Corporation accounts for certain

financial instruments under the fair value option. For more

information, see Note 23 – Fair Value Option.

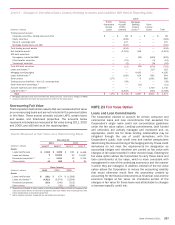

Level 1, 2 and 3 Valuation Techniques

Financial instruments are considered Level 1 when the valuation

is based on quoted prices in active markets for identical assets

or liabilities. Level 2 financial instruments are valued using quoted

prices for similar assets or liabilities, quoted prices in markets

that are not active, or models using inputs that are observable or

can be corroborated by observable market data for substantially

the full term of the assets or liabilities. Financial instruments are

considered Level 3 when their values are determined using pricing

models, discounted cash flow methodologies or similar

techniques, and at least one significant model assumption or input

is unobservable and when determination of the fair value requires

significant management judgment or estimation.

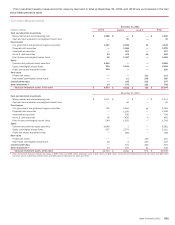

Trading Account Assets and Liabilities and Available-for-

Sale Debt Securities

The fair values of trading account assets and liabilities are primarily

based on actively traded markets where prices are based on either

direct market quotes or observed transactions. The fair values of

AFS debt securities are generally based on quoted market prices

or market prices for similar assets. Liquidity is a significant factor

in the determination of the fair values of trading account assets

and liabilities and AFS debt securities. Market price quotes may

not be readily available for some positions, or positions within a

market sector where trading activity has slowed significantly or

ceased. Some of these instruments are valued using a discounted

cash flow model, which estimates the fair value of the securities

using internal credit risk, interest rate and prepayment risk models

that incorporate management’s best estimate of current key

assumptions such as default rates, loss severity and prepayment

rates. Principal and interest cash flows are discounted using an

observable discount rate for similar instruments with adjustments

that management believes a market participant would consider in

determining fair value for the specific security. Other instruments

are valued using a net asset value approach which considers the

value of the underlying securities. Underlying assets are valued

using external pricing services, where available, or matrix pricing

based on the vintages and ratings. Situations of illiquidity generally

are triggered by the market’s perception of credit uncertainty

regarding a single company or a specific market sector. In these

instances, fair value is determined based on limited available

market information and other factors, principally from reviewing

the issuer’s financial statements and changes in credit ratings

made by one or more rating agencies.

Derivative Assets and Liabilities

The fair values of derivative assets and liabilities traded in the

OTC market are determined using quantitative models that utilize

multiple market inputs including interest rates, prices and indices

to generate continuous yield or pricing curves and volatility factors

to value the position. The majority of market inputs are actively

quoted and can be validated through external sources, including

brokers, market transactions and third-party pricing services.

When third-party pricing services are used, the methods and

assumptions used are reviewed by the Corporation. Estimation

risk is greater for derivative asset and liability positions that are

either option-based or have longer maturity dates where

observable market inputs are less readily available, or are

unobservable, in which case, quantitative-based extrapolations of

rate, price or index scenarios are used in determining fair values.

The fair values of derivative assets and liabilities include

adjustments for market liquidity, counterparty credit quality and

other instrument-specific factors, where appropriate. In addition,

the Corporation incorporates within its fair value measurements

of OTC derivatives a valuation adjustment to reflect the credit risk

associated with the net position. Positions are netted by

counterparty, and fair value for net long exposures is adjusted for

counterparty credit risk while the fair value for net short exposures

is adjusted for the Corporation’s own credit risk. An estimate of

severity of loss is also used in the determination of fair value,

primarily based on market data.

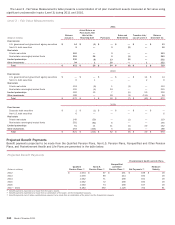

Loans and Loan Commitments

The fair values of loans and loan commitments are based on

market prices, where available, or discounted cash flow analyses

using market-based credit spreads of comparable debt

instruments or credit derivatives of the specific borrower or

comparable borrowers. Results of discounted cash flow

calculations may be adjusted, as appropriate, to reflect other

market conditions or the perceived credit risk of the borrower.