Bank of America 2011 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

86 Bank of America 2011

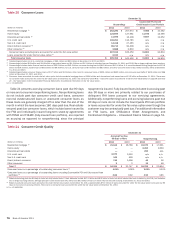

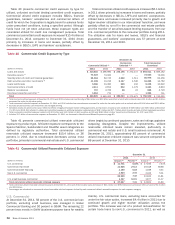

Table 35 presents certain state concentrations for the direct/indirect consumer loan portfolio.

Table 35

(Dollars in millions)

California

Texas

Florida

New York

Georgia

Other U.S./Non-U.S.

Total direct/indirect loan portfolio

Direct/Indirect State Concentrations

December 31

Outstandings

2011

$ 11,152

7,882

7,456

5,160

2,828

55,235

$ 89,713

2010

$ 10,558

7,885

6,725

4,770

2,814

57,556

$ 90,308

Accruing Past Due

90 Days or More

2011

$81

54

55

40

38

478

$746

2010

$ 132

78

80

56

44

668

$ 1,058

Net Charge-offs

2011

$222

117

148

79

61

849

$ 1,476

2010

$ 591

262

343

183

126

1,831

$ 3,336

Other Consumer

At December 31, 2011, approximately 96 percent of the $2.7

billion other consumer portfolio was associated with certain

consumer finance businesses that we previously exited and non-

U.S. consumer loan portfolios that are included in All Other. The

remainder is primarily deposit overdrafts in Deposits.

Consumer Loans Accounted for Under the Fair Value

Option

Outstanding consumer loans accounted for under the fair value

option were $2.2 billion at December 31, 2011 and include $1.3

billion of discontinued real estate loans and $906 million of

residential mortgage loans as a result of the consolidation of VIEs.

During 2011, we recorded losses of $837 million resulting from

changes in the fair value of the loan portfolio. These losses were

offset by gains recorded on the related long-term debt.

Nonperforming Consumer Loans and Foreclosed

Properties Activity

Table 36 presents nonperforming consumer loans and foreclosed

properties activity during 2011 and 2010. Nonperforming LHFS

are excluded from nonperforming loans as they are recorded at

either fair value or the lower of cost or fair value. Nonperforming

loans do not include past due consumer credit card loans and in

general, past due consumer loans not secured by real estate as

these loans are generally charged off no later than the end of the

month in which the loan becomes 180 days past due. The fully-

insured loan portfolio is not reported as nonperforming as principal

repayment is insured. Additionally, nonperforming loans do not

include the Countrywide PCI loan portfolio or loans that we account

for under the fair value option. For further information on

nonperforming loans, see Note 1 – Summary of Significant

Accounting Principles to the Consolidated Financial Statements.

Nonperforming loans declined to $18.8 billion at December 31,

2011 compared to $20.9 billion at December 31, 2010.

Delinquency inflows to nonperforming loans slowed compared to

the prior year due to favorable portfolio trends and were more than

offset by charge-offs, nonperforming loans returning to performing

status, and paydowns and payoffs.

The outstanding balance of a real estate-secured loan that is

in excess of the estimated property value, after reducing the

estimated property value for estimated costs to sell, is charged

off no later than the end of the month in which the loan becomes

180 days past due unless repayment of the loan is fully insured.

At December 31, 2011, $14.6 billion, or 71 percent, of

nonperforming consumer real estate loans and foreclosed

properties had been written down to their estimated property value

less estimated costs to sell, including $12.6 billion of

nonperforming loans 180 days or more past due and $2.0 billion

of foreclosed properties.

Foreclosed properties increased $742 million in 2011 as

additions outpaced liquidations. PCI loans are excluded from

nonperforming loans as these loans were written down to fair value

at the acquisition date. However, once the underlying real estate

is acquired by the Corporation upon foreclosure of the delinquent

PCI loan, it is included in foreclosed properties. Net changes to

foreclosed properties related to PCI loans increased $411 million

in 2011. Not included in foreclosed properties at December 31,

2011 was $1.4 billion of real estate that was acquired upon

foreclosure of delinquent FHA-insured loans. We hold this real

estate on our balance sheet until we convey these properties to

the FHA. We exclude these amounts from our nonperforming loans

and foreclosed properties activity as we will be reimbursed once

the property is conveyed to the FHA for principal and, up to certain

limits, costs incurred during the foreclosure process and interest

incurred during the holding period. For additional information on

the review of our foreclosure processes, see Off-Balance Sheet

Arrangements and Contractual Obligations – Other Mortgage-

related Matters on page 57.

Restructured Loans

Nonperforming loans also include certain loans that have been

modified in TDRs where economic concessions have been granted

to borrowers experiencing financial difficulties. These concessions

typically result from the Corporation’s loss mitigation activities and

could include reductions in the interest rate, payment extensions,

forgiveness of principal, forbearance or other actions. Certain

TDRs are classified as nonperforming at the time of restructuring

and may only be returned to performing status after considering

the borrower’s sustained repayment performance under revised

payment terms for a reasonable period, generally six months.

Nonperforming TDRs, excluding those modified loans in the

Countrywide PCI loan portfolio, are included in Table 36.

As a result of accounting guidance on PCI loans, beginning

January 1, 2010, modifications of loans in the PCI loan portfolio

do not result in removal of the loan from the PCI loan pool. TDRs

in the consumer real estate portfolio that were removed from the