Bank of America 2011 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 85

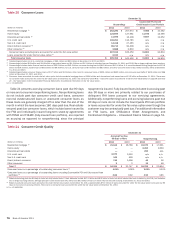

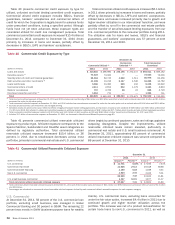

Table 33 presents certain state concentrations for the U.S. credit card portfolio.

Table 33

(Dollars in millions)

California

Florida

Texas

New York

New Jersey

Other U.S.

Total U.S. credit card portfolio

U.S. Credit Card State Concentrations

December 31

Outstandings

2011

$ 15,246

7,999

6,885

6,156

4,183

61,822

$ 102,291

2010

$ 17,028

9,121

7,581

6,862

4,579

68,614

$113,785

Accruing Past Due

90 Days or More

2011

$352

221

131

126

86

1,154

$ 2,070

2010

$ 612

376

207

192

132

1,801

$ 3,320

Net Charge-offs

2011

$ 1,402

838

429

403

275

3,929

$ 7,276

2010

$ 2,752

1,611

784

694

452

6,734

$ 13,027

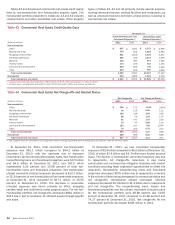

Non-U.S. Credit Card

During 2011, we sold our Canadian consumer card business and

we are evaluating our remaining international consumer card

portfolios. In light of these actions, the international consumer

card portfolios were moved from Card Services to All Other.

Outstandings in the non-U.S. credit card portfolio decreased

$13.0 billion in 2011 primarily due to the sale of the Canadian

consumer credit card portfolio, lower origination volume and

charge-offs. Net charge-offs decreased $1.0 billion in 2011 to

$1.2 billion due to the sale of previously charged-off loans, portfolio

sales, and improvements in delinquencies, collections and

insolvencies.

Unused lines of credit for non-U.S. credit card totaled

$36.8 billion and $60.3 billion at December 31, 2011 and 2010.

The $23.5 billion decrease was driven primarily by the sale of the

Canadian consumer credit card portfolio.

Table 34 presents certain key credit statistics for the non-U.S.

credit card portfolio.

Table 34

(Dollars in millions)

Outstandings

Accruing past due 30 days or more

Accruing past due 90 days or more

Net charge-offs

Net charge-off ratios (1)

Non-U.S. Credit Card – Key Credit Statistics

December 31

2011

$ 14,418

610

342

2011

$ 1,169

4.86%

2010

$ 27,465

1,354

599

2010

$ 2,207

7.88%

(1) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans

and leases.

Direct/Indirect Consumer

At December 31, 2011, approximately 48 percent of the direct/

indirect portfolio was included in Global Commercial Banking

(dealer financial services - automotive, marine, aircraft and

recreational vehicle loans), 36 percent was included in GWIM

(principally other non-real estate-secured, unsecured personal

loans and securities-based lending margin loans), nine percent

was included in Card Services (consumer personal loans) and the

remainder was in All Other (student loans).

Outstanding loans and leases decreased $595 million to $89.7

billion in 2011 due to lower outstandings in the Card Services

unsecured consumer lending portfolio partially offset by growth in

securities-based lending and product transfers from U.S.

commercial. For 2011, net charge-offs decreased $1.9 billion to

$1.5 billion, or 1.64 percent of total average direct/indirect loans

compared to 3.45 percent for 2010. This decrease was primarily

driven by improvements in delinquencies, collections and

bankruptcies in the unsecured consumer lending portfolio as a

result of an improved economic environment as well as reduced

outstandings. An additional driver was lower net charge-offs in the

dealer financial services portfolio due to the impact of higher credit

quality originations and higher resale values.

Net charge-offs in the unsecured consumer lending portfolio

decreased $1.6 billion to $1.1 billion in 2011, or 10.93 percent

of total average unsecured consumer lending loans compared to

17.24 percent for 2010. Net charge-offs in the dealer financial

services portfolio decreased $199 million to $293 million in 2011,

or 0.69 percent of total average dealer financial services loans

compared to 1.08 percent for 2010. Direct/indirect loans that

were past due 30 days or more and still accruing interest declined

$745 million to $1.9 billion at December 31, 2011 compared to

$2.6 billion at December 31, 2010 due to improvements in both

the unsecured consumer lending and dealer financial services

portfolios.