Bank of America 2011 Annual Report Download - page 154

Download and view the complete annual report

Please find page 154 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

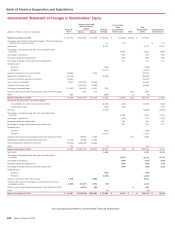

152 Bank of America 2011

Bank of America Corporation and Subsidiaries

Notes to Consolidated Financial Statements

NOTE 1 Summary of Significant Accounting

Principles

Bank of America Corporation (collectively with its subsidiaries, the

Corporation), a financial holding company, provides a diverse range

of financial services and products throughout the U.S. and in

certain international markets. The term “the Corporation” as used

herein may refer to the Corporation individually, the Corporation

and its subsidiaries, or certain of the Corporation’s subsidiaries

or affiliates.

The Corporation conducts its activities through banking and

nonbanking subsidiaries. The Corporation operates its banking

activities primarily under two charters: Bank of America, National

Association (Bank of America, N.A. or BANA) and FIA Card Services,

National Association (FIA Card Services, N.A.).

Principles of Consolidation and Basis of Presentation

The Consolidated Financial Statements include the accounts of

the Corporation and its majority-owned subsidiaries, and those

variable interest entities (VIEs) where the Corporation is the

primary beneficiary. Intercompany accounts and transactions have

been eliminated. Results of operations of acquired companies are

included from the dates of acquisition and for VIEs, from the dates

that the Corporation became the primary beneficiary. Assets held

in an agency or fiduciary capacity are not included in the

Consolidated Financial Statements. The Corporation accounts for

investments in companies for which it owns a voting interest and

for which it has the ability to exercise significant influence over

operating and financing decisions using the equity method of

accounting or at fair value under the fair value option. These

investments are included in other assets. Equity method

investments are subject to impairment testing and the

Corporation’s proportionate share of income or loss is included in

equity investment income.

The preparation of the Consolidated Financial Statements in

conformity with accounting principles generally accepted in the

United States of America requires management to make estimates

and assumptions that affect reported amounts and disclosures.

Realized results could differ from those estimates and

assumptions.

The Corporation evaluates subsequent events through the date

of filing with the Securities and Exchange Commission (SEC).

Certain prior period amounts have been reclassified to conform

to current period presentation.

New Accounting Pronouncements

In April 2011, the Financial Accounting Standards Board (FASB)

issued new accounting guidance on troubled debt restructurings

(TDRs), including criteria to determine whether a loan modification

represents a concession and whether the debtor is experiencing

financial difficulties. This new accounting guidance was effective

for the Corporation as of September 30, 2011 with retrospective

application back to January 1, 2011. As a result of the

retrospective application, the Corporation classified $1.1 billion

of commercial loan modifications as TDRs that in previous periods

had not been classified as TDRs. These loans were newly identified

as TDRs typically because the Corporation was not able to

demonstrate that the modified rate of interest, although

significantly higher than the rate prior to modification, was a market

rate of interest. These loans include $402 million of performing

commercial loans that had an aggregate allowance for credit

losses of $27 million at December 31, 2011. Also, as a result of

the new accounting guidance, loans that are participating in or

that have been offered a binding trial modification are classified

as TDRs. At December 31, 2011, the Corporation classified an

additional $2.6 billion of home loans, with an aggregate allowance

for credit losses of $154 million, as TDRs that were participating

in or had been offered a trial modification.

In April 2011, the FASB issued new accounting guidance that

addresses effective control in repurchase agreements and

eliminates the requirement for entities to consider whether the

transferor/seller has the ability to repurchase the financial assets

in a repurchase agreement. This new accounting guidance was

effective, on a prospective basis, for new transactions or

modifications to existing transactions on January 1, 2012. The

adoption of this guidance will not have a material impact on the

Corporation’s consolidated financial position or results of

operations.

In May 2011, the FASB issued amendments to the fair value

accounting guidance. The amendments clarify the application of

the highest and best use, and valuation premise concepts,

preclude the application of blockage factors in the valuation of all

financial instruments and include criteria for applying the fair value

measurement principles to portfolios of financial instruments. The

amendments additionally prescribe enhanced financial statement

disclosures for Level 3 fair value measurements. The new

amendments were effective on January 1, 2012. The adoption of

this guidance will not have a material impact on the Corporation’s

consolidated financial position or results of operations.

In June 2011, the FASB issued new accounting guidance on

the presentation of comprehensive income in financial

statements. The new guidance requires entities to report

components of comprehensive income in either a continuous

statement of comprehensive income or two separate but

consecutive statements. This new accounting guidance is effective

for the Corporation for the three months ended March 31, 2012.

In September 2011, the FASB issued new accounting guidance

that simplifies goodwill impairment testing. The new guidance

permits entities to make a qualitative assessment of whether it

is likely that the fair value of a reporting unit is less than its carrying

value. If, under this assessment, it is likely that the fair value of

a reporting unit is less than the carrying amount, an entity is

required to perform the two-step impairment test. The Corporation

early adopted the new accounting guidance for certain goodwill

impairment tests during the three months ended September 30,

2011.