Bank of America 2011 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 75

We proactively refine our underwriting and credit management

practices as well as credit standards to meet the changing

economic environment. To actively mitigate losses and enhance

customer support in our consumer businesses, we have expanded

collections, loan modification and customer assistance

infrastructures. We also have implemented a number of actions

to mitigate losses in the commercial businesses including

increasing the frequency and intensity of portfolio monitoring,

hedging activity and our practice of transferring management of

deteriorating commercial exposures to independent special asset

officers as credits enter criticized categories.

Since January 2008, and through 2011, Bank of America and

Countrywide have completed over one million loan modifications

with customers. During 2011, we completed over 225,000

customer loan modifications with a total unpaid principal balance

of approximately $49.9 billion, including approximately 104,000

permanent modifications under the government’s Making Home

Affordable Program. Of the loan modifications completed in 2011,

in terms of both the volume of modifications and the unpaid

principal balance associated with the underlying loans, most were

in the portfolio serviced for investors and were not on our balance

sheet. The most common types of modifications include a

combination of rate reduction and capitalization of past due

amounts which represent 60 percent of the volume of

modifications completed in 2011, while principal forbearance

represented 19 percent, principal reductions and forgiveness

represented six percent and capitalization of past due amounts

represented eight percent. These modification types are generally

considered troubled debt restructurings (TDRs). For more

information on TDRs and portfolio impacts, see Nonperforming

Consumer Loans and Foreclosed Properties Activity on page 86

and Note 6 – Outstanding Loans and Leases to the Consolidated

Financial Statements.

Certain European countries, including Greece, Ireland, Italy,

Portugal and Spain, continue to experience varying degrees of

financial stress. In early 2012, S&P, Fitch and Moody’s downgraded

the credit ratings of several European countries, and S&P

downgraded the credit rating of the EFSF, adding to concerns about

investor appetite for continued support in stabilizing the affected

countries. Uncertainty in the progress of debt restructuring

negotiations and the lack of a clear resolution to the crisis has

led to continued volatility in the European financial markets, and

if the situation worsens, may spread into the global financial

markets. In December 2011, the ECB announced initiatives to

address European bank liquidity and funding concerns by providing

low-cost three-year loans to banks, and expanding collateral

eligibility. While these initiatives may reduce systemic risk, there

remains considerable uncertainty as to future developments

regarding the European debt crisis. For additional information on

our direct sovereign and non-sovereign exposures in non-U.S.

countries, see Non-U.S. Portfolio on page 98 and Item 1A. Risk

Factors of this Annual Report on Form 10-K.

Consumer Portfolio Credit Risk Management

Credit risk management for the consumer portfolio begins with

initial underwriting and continues throughout a borrower’s credit

cycle. Statistical techniques in conjunction with experiential

judgment are used in all aspects of portfolio management

including underwriting, product pricing, risk appetite, setting credit

limits, and establishing operating processes and metrics to

quantify and balance risks and returns. Statistical models are built

using detailed behavioral information from external sources such

as credit bureaus and/or internal historical experience. These

models are a component of our consumer credit risk management

process and are used in part to help make both new and existing

credit decisions and portfolio management strategies, including

authorizations and line management, collection practices and

strategies, determination of the allowance for loan and lease

losses, and economic capital allocations for credit risk.

For information on our accounting policies regarding

delinquencies, nonperforming status, charge-offs and TDRs for the

consumer portfolio, see Note 1 – Summary of Significant

Accounting Principles to the Consolidated Financial Statements.

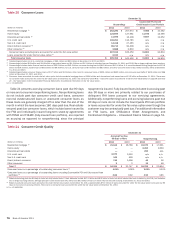

Consumer Credit Portfolio

Improvement in the U.S. economy and labor markets during 2011

resulted in lower credit losses in most consumer portfolios during

2011 compared to 2010. However, continued stress in the housing

market, including declines in home prices, continued to adversely

impact the home loans portfolio.

Table 20 presents our outstanding consumer loans and the

Countrywide PCI loan portfolio. Loans that were acquired from

Countrywide and considered credit-impaired were recorded at fair

value upon acquisition. In addition to being included in the

“Outstandings” columns in Table 20, these loans are also shown

separately, net of purchase accounting adjustments, in the

“Countrywide Purchased Credit-impaired Loan Portfolio” column.

For additional information, see Note 6 – Outstanding Loans and

Leases to the Consolidated Financial Statements. The impact of

the Countrywide PCI loan portfolio on certain credit statistics is

reported where appropriate. See Countrywide Purchased Credit-

impaired Loan Portfolio on page 83 for more information. Under

certain circumstances, loans that were originally classified as

discontinued real estate loans upon acquisition have been

subsequently modified from pay option or subprime loans into

loans with more conventional terms and are now included in the

residential mortgage portfolio, but continue to be classified as PCI

loans as shown in Table 20.