Bank of America 2011 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

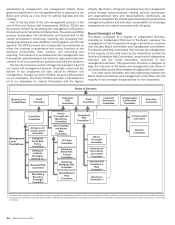

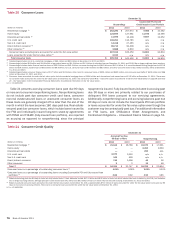

68 Bank of America 2011

If implemented by U.S. banking regulators as proposed, Basel

III could significantly increase our capital requirements. Basel III

and the Financial Reform Act propose the disqualification of Trust

Securities from Tier 1 capital, with the Financial Reform Act

proposing that the disqualification be phased in from 2013 to

2015. Basel III also proposes the deduction of certain assets from

capital (deferred tax assets, MSRs, investments in financial firms

and pension assets, among others, within prescribed limitations),

the inclusion of accumulated OCI in capital, increased capital for

counterparty credit risk, and new minimum capital and buffer

requirements. For additional information on deferred tax assets

and MSRs, see Note 21 – Income Taxes and Note 25 – Mortgage

Servicing Rights to the Consolidated Financial Statements. The

phase-in period for the capital deductions is proposed to occur in

20 percent increments from 2014 through 2018 with full

implementation by December 31, 2018. An increase in capital

requirements for counterparty credit risk is proposed to be

effective January 2013. The phase-in period for the new minimum

capital requirements and related buffers is proposed to occur

between 2013 and 2019. U.S. banking regulators have not yet

issued proposed regulations that will implement these

requirements.

Preparing for the implementation of the new capital rules is a

top strategic priority, and we expect to comply with the final rules

when issued and effective. We intend to continue to build capital

through retaining earnings, actively reducing legacy asset

portfolios and implementing other capital related initiatives,

including focusing on reducing both higher risk-weighted assets

and assets currently deducted, or expected to be deducted under

Basel III, from capital. We expect non-core asset sales to play a

less prominent role in our capital strategy in future periods.

On June 17, 2011, U.S. banking regulators proposed rules

requiring all large bank holding companies (BHCs) to submit a

comprehensive capital plan to the Federal Reserve as part of an

annual Comprehensive Capital Analysis and Review (CCAR). The

proposed regulations require BHCs to demonstrate adequate

capital to support planned capital actions, such as dividends,

share repurchases or other forms of distributing capital. CCAR

submissions are subject to the review and approval of the Federal

Reserve. The Federal Reserve may require BHCs to provide prior

notice under certain circumstances before making a capital

distribution. On January 5, 2012, we submitted a capital plan to

the Federal Reserve consistent with the proposed rules. The

capital plan includes the ICAAP and related results, analysis and

support for the capital guidelines, and planned capital actions.

The ICAAP incorporates capital forecasts, stress test results,

economic capital, qualitative risk assessments and assessment

of regulatory changes, all of which influence the capital adequacy

assessment.

On July 19, 2011, the Basel Committee published the

consultative document “Globally systemic important banks:

Assessment methodology and the additional loss absorbency

requirement” which sets out measures for global, systemically

important financial institutions including the methodology for

measuring systemic importance, the additional capital required

(the SIFI buffer), and the arrangements by which they will be phased

in. As proposed, the SIFI buffer would be met with additional Tier

1 common equity ranging from one percent to 2.5 percent, and in

certain circumstances, 3.5 percent. This will be phased in from

2016 through 2018. U.S. banking regulators have not yet provided

similar rules for U.S. implementation of a SIFI buffer.

Given that the U.S. regulatory agencies have issued neither

proposed rulemaking nor supervisory guidance on Basel III,

significant uncertainty exists regarding the eventual impacts of

Basel III on U.S. financial institutions, including us. These

regulatory changes also require approval by the U.S. regulatory

agencies of analytical models used as part of our capital

measurement and assessment, especially in the case of more

complex models. If these more complex models are not approved,

it could require financial institutions to hold additional capital,

which in some cases could be significant.

Based on the assumed approval of these models and our

current assessment of Basel III, continued focus on capital

management, expectations of future performance and continued

efforts to build a fortress balance sheet, we currently anticipate

that our Tier 1 common equity ratio will be between 7.25 percent

and 7.50 percent by the end of 2012, assuming phase-in per the

regulations at that time of all deductions scheduled to occur

between 2013 and 2019.

On December 20, 2011, the Federal Reserve issued proposed

rules to implement enhanced supervisory and prudential

requirements and the early remediation requirements established

under the Financial Reform Act. The enhanced standards include

risk-based capital and leverage requirements, liquidity standards,

requirements for overall risk management, single-counterparty

credit limits, stress test requirements and a debt-to-equity limit

for certain companies determined to pose a threat to financial

stability. Comments on the proposed rules are due by March 31,

2012. The final rules are likely to influence our regulatory capital

and liquidity planning process, and may impose additional

operational and compliance costs on us.

For additional information regarding Basel II, Basel III, Market

Risk Rules and other proposed regulatory capital changes, see

Note 18 – Regulatory Requirements and Restrictions to the

Consolidated Financial Statements.