Bank of America 2011 Annual Report Download - page 201

Download and view the complete annual report

Please find page 201 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

Bank of America 2011 199

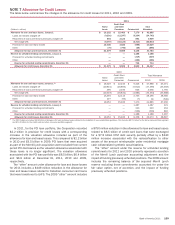

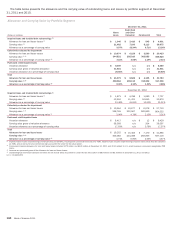

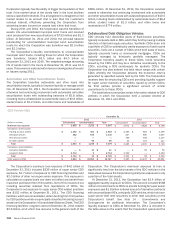

Other Asset-backed Financing Arrangements

The Corporation transferred pools of securities to certain

independent third parties and provided financing for approximately

75 percent of the purchase price under asset-backed financing

arrangements. At December 31, 2011 and 2010, the

Corporation’s maximum loss exposure under these financing

arrangements was $4.7 billion and $6.5 billion, substantially all

of which was classified as loans on the Corporation’s Consolidated

Balance Sheet. All principal and interest payments have been

received when due in accordance with the contractual terms. These

arrangements are not included in the Other VIEs table because

the purchasers are not VIEs.

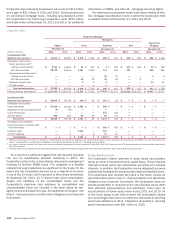

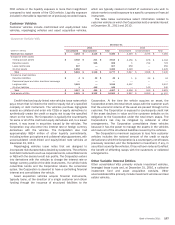

NOTE 9 Representations and Warranties

Obligations and Corporate Guarantees

Background

The Corporation securitizes first-lien residential mortgage loans,

generally in the form of MBS guaranteed by the GSEs or by GNMA

in the case of FHA-insured, VA-guaranteed and Rural Housing

Service-guaranteed mortgage loans. In addition, in prior years,

legacy companies and certain subsidiaries sold pools of first-lien

residential mortgage loans and home equity loans as private-label

securitizations (in certain of these securitizations, monolines or

financial guarantee providers insured all or some of the securities),

or in the form of whole loans. In connection with these transactions,

the Corporation or certain subsidiaries or legacy companies make

or have made various representations and warranties. These

representations and warranties, as set forth in the agreements,

related to, among other things, the ownership of the loan, the

validity of the lien securing the loan, the absence of delinquent

taxes or liens against the property securing the loan, the process

used to select the loan for inclusion in a transaction, the loan’s

compliance with any applicable loan criteria, including underwriting

standards, and the loan’s compliance with applicable federal, state

and local laws. Breaches of these representations and warranties

may result in the requirement to repurchase mortgage loans or to

otherwise make whole or provide other remedies to the GSEs, U.S.

Department of Housing and Urban Development (HUD) with

respect to FHA-insured loans, VA, whole-loan buyers, securitization

trusts, monoline insurers or other financial guarantors (collectively,

repurchases). In such cases, the Corporation would be exposed

to any credit loss on the repurchased mortgage loans after

accounting for any mortgage insurance (MI) or mortgage guaranty

payments that it may receive.

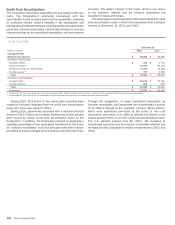

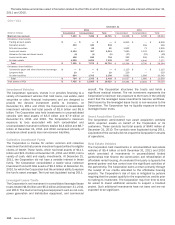

Subject to the requirements and limitations of the applicable

sales and securitization agreements, these representations and

warranties can be enforced by the GSEs, HUD, VA, the whole-loan

buyer, the securitization trustee or others as governed by the

applicable agreement or, in certain first-lien and home equity

securitizations where monoline insurers or other financial

guarantee providers have insured all or some of the securities

issued, by the monoline insurer or other financial guarantor. In the

case of loans sold to parties other than the GSEs or GNMA, the

contractual liability to repurchase typically arises only if there is a

breach of the representations and warranties that materially and

adversely affects the interest of the investor, or investors, in the

loan, or of the monoline insurer or other financial guarantor (as

applicable). Contracts with the GSEs do not contain equivalent

language, while GNMA generally limits repurchases to loans that

are not insured or guaranteed as required. The Corporation

believes that the longer a loan performs prior to default, the less

likely it is that an alleged underwriting breach of representations

and warranties had a material impact on the loan’s performance.

Historically, most demands for repurchase have occurred within

the first several years after origination, generally after a loan has

defaulted. However, the time horizon in which repurchase claims

are typically brought has lengthened primarily due to a significant

increase in GSE claims related to loans that had defaulted more

than 18 months prior to the claim and to loans where the borrower

made at least 25 payments.

The Corporation’s credit loss would be reduced by any recourse

it may have to organizations (e.g., correspondents) that, in turn,

had sold such loans to the Corporation based upon its agreements

with these organizations. When a loan is originated by a

correspondent or other third party, the Corporation typically has

the right to seek a recovery of related repurchase losses from that

originator. Many of the correspondent originators of loans in 2004

through 2008 are no longer in business, or are in a weakened

condition, and the Corporation’s ability to recover on valid claims

is therefore impacted, or eliminated accordingly. In the event a

loan is originated and underwritten by a correspondent who obtains

FHA insurance, even if they are no longer in business, any breach

of FHA guidelines is the direct obligation of the correspondent, not

the Corporation. At December 31, 2011, approximately 28 percent

of the outstanding repurchase claims relate to loans purchased

from correspondents or other parties compared to approximately

25 percent at December 31, 2010. During 2011, the Corporation

experienced a decline in recoveries from correspondents and other

parties; however, the actual recovery rate may vary from period to

period based upon the underlying mix of correspondents and other

parties.

The Corporation currently structures its operations to limit the

risk of repurchase and accompanying credit exposure by seeking

to ensure consistent production of mortgages in accordance with

its underwriting procedures and by servicing those mortgages

consistent with its contractual obligations. In addition, certain

securitizations include guarantees written to protect certain

purchasers of the loans from credit losses up to a specified

amount. The fair value of the obligations to be absorbed under the

representations and warranties and guarantees provided is

recorded as an accrued liability when the loans are sold. This

liability for probable losses is updated by accruing a

representations and warranties provision in mortgage banking

income. This is done throughout the life of the loan, as necessary

when additional relevant information becomes available.

The methodology used to estimate the liability for

representations and warranties is a function of the representations

and warranties given and considers a variety of factors, which

include, depending on the counterparty, actual defaults, estimated

future defaults, historical loss experience, estimated home prices,

other economic conditions, estimated probability that a

repurchase claim will be received, including consideration of

whether presentation thresholds will be met, number of payments

made by the borrower prior to default and estimated probability

that a loan will be required to be repurchased. The Corporation

also considers bulk settlements when determining its estimated

liability for representations and warranties. The estimate of the

liability for representations and warranties is based upon currently

available information, significant judgment, and a number of

factors, including those set forth above, that are subject to change.

Changes to any one of these factors could significantly impact the

estimate of the liability and could have a material adverse impact