Bank of America 2011 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2011 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

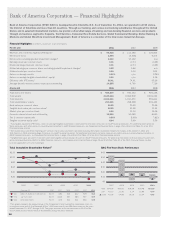

24 Bank of America 2011

Credit Ratings

On December 15, 2011, Fitch Ratings (Fitch) downgraded the

Corporation’s and BANA’s long-term and short-term debt ratings

as a result of Fitch’s decision to lower its “support floor” for

systemically important U.S. financial institutions. On November

29, 2011, S&P downgraded our long-term and short-term debt

ratings as well as BANA’s long-term debt rating as a result of S&P’s

implementation of revised methodologies for determining Banking

Industry Country Risk Assessments and bank ratings. On

September 21, 2011, Moody’s Investors Service, Inc. (Moody’s)

downgraded our long-term and short-term debt ratings as well as

BANA’s long-term debt rating as a result of Moody’s lowering the

amount of uplift for potential U.S. government support it

incorporates into ratings. On February 15, 2012, Moody’s placed

the Corporation’s long-term debt ratings and BANA’s long-term and

short-term debt ratings on review for possible downgrade as part

of its review of financial institutions with global capital markets

operations. Any adjustment to our ratings will be determined based

on Moody’s review; however, the agency offered guidance that

downgrades to our ratings, if any, would likely be limited to one

notch.

Currently, our long-term/short-term senior debt ratings and

outlooks expressed by the rating agencies are as follows: Baa1/

P-2 (negative) by Moody’s, A-/A-2 (negative) by S&P and A/F1

(stable) by Fitch. The rating agencies could make further

adjustments to our ratings at any time and there can be no

assurance that additional downgrades will not occur.

Under the terms of certain over-the-counter (OTC) derivative

contracts and other trading agreements, in the event of a

downgrade of our credit ratings or certain subsidiaries’ credit

ratings, counterparties to those agreements may require us or

certain subsidiaries to provide additional collateral or to terminate

those contracts or agreements or provide other remedies.

For information regarding the risks associated with adverse

changes in our credit ratings, see Liquidity Risk – Credit Ratings

on page 73, Note 4 – Derivatives to the Consolidated Financial

Statements and Item 1A. Risk Factors of this Annual Report on

Form 10-K.

European Union Sovereign Credit Risks

Certain European countries, including Greece, Ireland, Italy,

Portugal and Spain, continue to experience varying degrees of

financial stress. Uncertainty in the progress of debt restructuring

negotiations and the lack of a clear resolution to the crisis has

led to continued volatility in European as well as global financial

markets, and if the situation worsens, may further adversely affect

these markets. In December 2011, the European Central Bank

announced initiatives to address European bank liquidity and

funding concerns by providing low-cost, three-year loans to banks,

and expanding collateral eligibility. While reducing systemic risk,

there remains considerable uncertainty as to future developments

regarding the European debt crisis. In early 2012, S&P, Fitch and

Moody’s downgraded the credit ratings of several European

countries, and S&P downgraded the credit rating of the EFSF,

adding to concerns about investor appetite for continued support

in stabilizing the affected countries. Our total sovereign and non-

sovereign exposure to Greece, Italy, Ireland, Portugal and Spain,

was $15.3 billion at December 31, 2011 compared to $16.6 billion

at December 31, 2010. Our total net sovereign and non-sovereign

exposure to these countries was $10.5 billion at December 31,

2011 compared to $12.4 billion at December 31, 2010, after

taking into account net credit default protection. At December 31,

2011 and 2010, the fair value of net credit default protection

purchased was $4.9 billion and $4.2 billion. Losses could still

result because our credit protection contracts only pay out under

certain scenarios. For a further discussion of our direct sovereign

and non-sovereign exposures in Europe, see Non-U.S. Portfolio on

page 98 and for more information about the risks associated with

our non-sovereign exposures in Europe, see Item 1A. Risk Factors

of this Annual Report on Form 10-K.

Project New BAC

Project New BAC is a two-phase, enterprise-wide initiative to

simplify and streamline workflows and processes, align

businesses and expenses more closely with our overall strategic

plan and operating principles, and increase revenues. Phase 1

evaluations, which were completed in September 2011, focused

on the consumer businesses, including Deposits, Card Services

and CRES, and related support, technology and operations

functions. Phase 2 evaluations began in October 2011 and are

focused on Global Commercial Banking, GBAM and GWIM, and

related support, technology and operations functions not subject

to evaluation in Phase 1. Phase 2 evaluations are expected to

continue through April 2012.

Implementation of Phase 1 recommendations began in 2011.

Phase 1 has a stated goal of a reduction of approximately 30,000

positions, with natural attrition and the elimination of unfilled

positions expected to represent a significant part of the reduction.

A stated goal of the full implementation of Phase 1 is to reduce

certain costs by $5 billion per year by 2014 and we anticipate that

more than 20 percent of these cost savings could be achieved by

the end of 2012. As implementation of the Phase 1

recommendations continues and Phase 2 begins, reductions in

staffing levels in the affected areas are expected to result in some

incremental costs including severance.

Reductions in the areas subject to evaluation for Phase 2 have

not yet been fully identified, and accordingly, potential cost savings

cannot be estimated at this time; however, they are expected to

be lower than Phase 1 because the businesses have lower

headcount. All aspects of New BAC are expected to be

implemented by the end of 2014. There were no material expenses

related to New BAC recorded in 2011. For information about the

risks associated with Project New BAC, see Item 1A. Risk Factors

of this Annual Report on Form 10-K.