RBS 2009 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

99RBS Group Annual Report and Accounts 2009

Business review

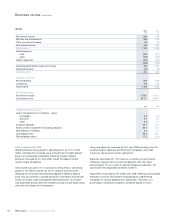

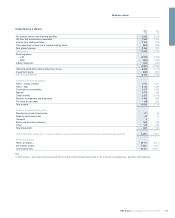

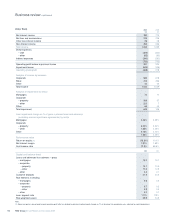

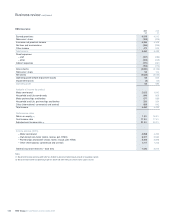

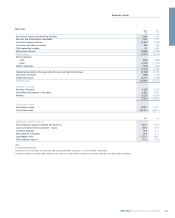

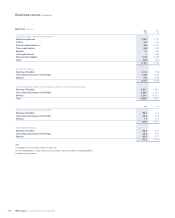

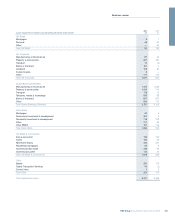

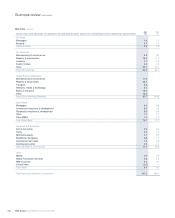

2009 compared with 2008

The recessionary economic environment, historically low interest rates

and deteriorating credit conditions resulted in an operating loss of $174

million. However, the business has now successfully refocused on its

core customer franchises in New England, the Mid-Atlantic region and

the Midwest.

The division achieved very strong growth in mortgage origination

volumes, with significantly higher penetration through the branch

network and improved profitability, particularly on recent origination

vintages. Cross-selling of card, deposit and checking account products

has increased substantially, with over 65% of new mortgage customers

also taking out a checking account. The division has also increased

commercial banking market penetration, with lead bank share within its

footprint increasing from 6% to 7% in the $5 million to $25 million

segment and from 6% to 8% in the $25 million to $500 million segment.

Net interest income was down 13%. Net interest margin was down

31bps for the full year, reflecting the decline in deposit margins resulting

from the low interest rate environment, though margins have been

partially rebuilt in the second half from the lows experienced in the first

half, as the business repriced lending rates and aggressively reduced

pricing on term and time deposits.

Expenses increased by 11%, reflecting increased FDIC deposit

insurance levies, higher employee benefit costs as well as increased

costs relating to loan workout and collection activity. Successful

execution of restructuring activities resulted in approximately $75 million

of cost savings.

Impairment losses increased to $1,099 million as charge-offs climbed to

0.90% of loans, an increase of 34bps compared with 2008.

Loans and advances were down 12%, reflecting subdued customer

demand.

Customer deposits increased 4% from the prior year. The deposit mix

improved significantly, with strong growth in checking balances

combined with migration away from higher priced term and time

deposits as the division adjusted its pricing strategies. Over 58,000

consumer checking accounts were added over the course of the year,

and more than 13,000 small business checking accounts. Consumer

checking balances grew by 8% and small business balances by 12%.