RBS 2009 Annual Report Download - page 260

Download and view the complete annual report

Please find page 260 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

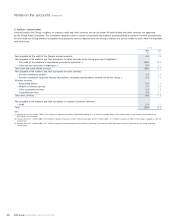

Accounting policies continued

RBS Group Annual Report and Accounts 2009258

Accounting developments

International Financial Reporting Standards

The International Accounting Standards Board (IASB) published a

revised IFRS 3 ‘Business Combinations’ and related revisions to IAS 27

‘Consolidated and Separate Financial Statements’ following the

completion in January 2008 of its project on the acquisition and

disposal of subsidiaries. The standards improve convergence with US

GAAP and provide new guidance on accounting for changes in interests

in subsidiaries. The cost of an acquisition will comprise only

consideration paid to vendors for equity; other costs will be expensed

immediately. Groups will only account for goodwill on acquisition of a

subsidiary; subsequent changes in interest will be recognised in equity

and only on a loss of control will there be a profit or loss on disposal to

be recognised in income. The changes are effective for accounting

periods beginning on or after 1 July 2009 but both standards may be

adopted together for accounting periods beginning on or after 1 July

2007. These changes will affect the Group’s accounting for future

acquisitions and disposals of subsidiaries.

The IASB issued amendments to a number of standards in April 2009

as part of its annual improvements project. The amendments are

effective for annual periods beginning on or after 1 July 2009 and are

not expected to have a material effect on the Group or the company.

The IASB issued an amendment, ‘Group Cash-settled Share-based

Payment Transactions‘, to IFRS 2 ‘Share-based Payment’ in June 2009

that will change the accounting for share awards by permitting

accounting for equity settlement only by entities that either grant awards

over their own equity or have no obligation to settle a share-based

payment transaction. The amendment is effective for annual periods

beginning on or after 1 January 2010 and is not expected to have a

material effect on the Group or the company.

The IASB published an amendment ‘Classification of Rights Issues’ to

IAS 32 ‘Financial Instruments: Presentation’ and consequential revisions

to other standards in October 2009 to improve the accounting for issues

of equity for consideration fixed other than in the reporting entity’s

functional currency. The amendment is effective for annual periods

beginning on or after 1 February 2010 but it may be adopted earlier. It is

not expected to have a material affect on the Group or the company.

The IASB reissued IAS 24, ‘Related Party Disclosures’, in November

2009 clarifying the existing standard and to provide certain exemptions

for entities under government control. The revised standard is effective

for annual periods beginning on or after 1 January 2011.

The IASB issued IFRS 9 ‘Financial Instruments’ in November 2009

simplifying the classification and measurement requirements in IAS 39

‘Financial Instruments: Recognition and Measurement’ in respect of

financial assets. The standard reduces the measurement categories for

financial assets to two: fair value and amortised cost. A financial asset

is classified on the basis of the entity’s business model for managing

the financial asset and the contractual cash flow characteristics of the

financial asset. Only assets with contractual terms that give rise to cash

flows on specified dates that are solely payments of principal and

interest on the principal amount outstanding and which are held within a

business model whose objective is to hold assets in order to collect

contractual cash flows are classified as amortised cost. All other

financial assets are measured at fair value. Changes in the value of

financial assets measured at fair value are generally taken to profit or

loss. The standard is effective for annual periods beginning on or after 1

January 2013; early application is permitted.

This standard makes major changes to the framework for the

classification and measurement of financial assets and will have a

significant effect on the Group’s financial statements. The Group is

assessing this impact which is likely to depend on the outcome of the

other phases of IASB’s IAS 39 replacement project.

The International Financial Reporting Interpretations Committee (IFRIC)

issued interpretation IFRIC 17 ‘Distributions of Non-Cash Assets to

Owners’ and the IASB made consequential amendments to IFRS 5 ‘Non-

Current Assets Held for Sale and Discontinued Operations’ in December

2008. The interpretation requires distributions to be presented at fair

value with any surplus or deficit recognised in income. The amendment

to IFRS 5 extends the definition of disposal groups and discontinued

operations to disposals by way of distribution. The interpretation is

effective for annual periods beginning on or after 1 July 2009, to be

adopted at the same time as IFRS 3 ‘Business Combinations’ (revised

2008), and is not expected to have a material effect on the company.

The interpretation may affect the accounting treatment in the Group's

financial statements of the ABN AMRO businesses to be acquired by

the State of Netherlands following the reorganisation of ABN AMRO

Bank N.V. described in Note 16.

The IFRIC issued interpretation IFRIC 18 ‘Transfers of Assets from

Customers’ in January 2009. The interpretation addresses the

accounting by suppliers for assets received from customers, requiring

such assets to be measured at fair value. The interpretation is effective

for assets from customers received on or after 1 July 2009 and is not

expected to have a material effect on the Group or the company.

The IFRIC issued interpretation IFRIC 19 ‘Extinguishing Financial

Liabilities with Equity Instruments’ in December 2009. The interpretation

clarifies that the profit or loss on extinguishing liabilities by issuing equity

instruments should be measured by reference to fair value, preferably of

the equity instruments. The interpretation, effective for the Group for

annual periods beginning on or after 1 January 2011, is not expected to

have a material effect on the Group or the company.