RBS 2009 Annual Report Download - page 191

Download and view the complete annual report

Please find page 191 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

Risk, capital and liquidity management

189RBS Group Annual Report and Accounts 2009

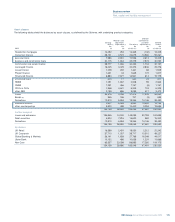

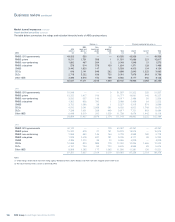

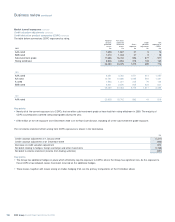

Key points

•Total asset-backed securities decreased from £111.1 billion at 31

December 2008 to £88.2 billion at 31 December 2009, due principally

to exchange rate movements and the significant sell-down activity

which took place in the first half of the year. In addition, credit

spreads widened in the first half of the year, further reducing carrying

values, although this was off-set to some extent by spreads tightening

in the second half of the year. Sales have been limited in the second

half of the year, however maturities have continued to reduce the

balance sheet exposures.

•Life-to-date net valuation losses on ABS held at 31 December 2009,

including impairment provisions, were £20.1 billion comprising:

– RMBS: £3.6 billion, of which £0.7 billion was in US sub-prime and

£2.3 billion in European assets;

– CMBS: £1.2 billion;

– CDOs: £9.4 billion and CLOs: £3.3 billion, significantly all in Non-

Core; and

– Other ABS: £2.6 billion.

•The majority of the Group’s exposure to ABS is through government-

backed RMBS, amounting to £43.6 billion at 31 December 2009 (2008

– £51.6 billion), and includes:

– US government -backed securities, comprising mainly current year

vintage positions, were £27.0 billion (2008 – £33.5 billion). Due to

the US government backing, explicit or implicit, for these securities,

the counterparty credit risk exposure is low. This is comprised of:

– HFT securities of £13.4 billion (2008 – £18.6 billion). These

securities are actively transacted and possess a high degree of

liquidity. Trading in this portfolio has shifted to more recent

vintages;

– AFS securities of £13.6 billion (2008 – £14.9 billion) relating to

liquidity portfolios held by US Retail & Commercial; and

– The decrease in exposure over the year was due to foreign

exchange movements driven by the strengthening of sterling

against the US dollar in the first half of the year and a decrease

in the balances in the second half of the year.

– Other European government-backed exposures of £16.2 billion. This

largely comprises liquidity portfolios of £15.6 billion held by Group

Treasury (2008 – £17.7 billion) in European government-backed

RMBS, referencing primarily Dutch and Spanish government-backed

loans and covered mortgage bonds. The portfolio reduced during

the year, driven primarily by exchange rate movements, partially off-

set by improved prices, mainly during the second half of the year.

•The Group has other portfolios of RMBS from secondary trading

activities, warehoused positions previously acquired with the intention

of securitisation, and a portfolio of assets from the unwinding of the

Group’s securities arbitrage conduit in 2008.

•Material disposals of prime RMBS occurred in the first half of the

year, in particular £1.5 billion of 2005 vintage US securities, £0.5

billion of Spanish and Portuguese mortgages and £0.6 billion of

positions which were hedged.

•CDOs decreased from £9.0 billion at 31 December 2008 to £3.9

billion at 31 December 2009, driven primarily by significant declines in

prices, together with foreign exchange movements, in the first half of

the year.

•Subprime balances decreased across ratings, geographies and

vintages, due to pay-downs, maturities and sales during the year,

while non-conforming exposures fell mainly due to UK AAA-rated AFS

redemptions. During the third quarter, improved prices off-set the

effect of redemptions in some portfolios.

•US Mortgage trading in GBM, US Retail and Commercial are in Core.

•Many of the assets, primarily CDOs and CLOs, in Non-Core Trading

have market hedges in place which gives rise to a significant

difference between the carrying value and the net exposure.

•AAA-rated assets decreased from £93.9 billion at 31 December 2008

to £65.6 billion at 31 December 2009 primarily as a result of the sell-

down activity of prime and government-backed securities.

•There was no significant change in the percentage of asset-backed

securities classified as level 2 and level 3 assets year-on-year (2009 –

87% and 4% respectively, 2008 – 87% and 5% respectively).

•There were significant downgrades of AAA-rated CLOs to BBB during

the year.

The remainder of this section provides additional information and

analysis of specific ABS portfolios.

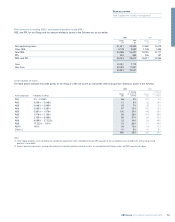

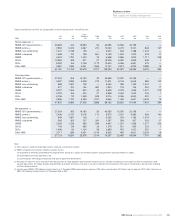

Residential mortgage-backed securities (RMBS)

RMBS are securities that represent an interest in a portfolio of

residential mortgages. Repayments made on the underlying mortgages

are used to make payments to holders of the RMBS. The risk of the

RMBS will vary primarily depending on the quality and geographic

region of the underlying mortgage assets and the credit enhancement

of the securitisation structure. Several tranches of notes are issued,

each secured against the same portfolio of mortgages, but providing

differing levels of seniority to match the risk appetite of investors. The

most junior (or equity) notes will suffer early capital and interest losses

experienced by the referenced mortgage collateral, with each more

senior note benefiting from the protection provided by the subordinated

notes below. Additional credit enhancements may be provided to the

holder of senior RMBS notes, including guarantees over the value of the

exposures, often provided by monoline insurers.

The main categories of mortgages that serve as collateral to RMBS held

by the Group are described below. The US market has more established

definitions of differing underlying mortgage quality and these are used

as the basis for the Group’s RMBS categorisation.