RBS 2009 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009136

* unaudited

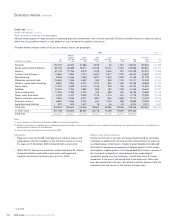

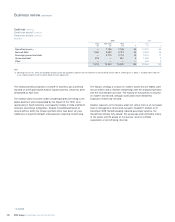

Personal lending

The Group’s personal lending portfolio includes credit cards, unsecured loans, auto finance and overdrafts. The majority of personal lending

exposures exist in the UK and the US. New defaults as a proportion of average loans and receivables were:

2009 2008

Impairment Impairment

Average charge as a % Average charge as a %

loans and of loans and loans and of loans and

receivables receivables receivables receivables

Personal lending £m % £m %

UK Retail cards (1) 6,101 8.7 6,617 6.4

UK Retail loans (1) 12,062 5.9 13,545 3.3

$m % $m %

Citizens cards (2) 2,286 8.9 2,275 4.9

Citizens auto loans (2) 9,759 1.2 11,386 1.1

Notes:

(1) The charge for UK Retail assets refers to impairment on assets in the year.

(2) The charge for Citizens assets refers to charge offs in the year, net of recoveries realised in the year.

Credit risk continued

Credit risk assets*continued

The SBO portfolio consists of purchased pools of home equity loans

and lines whose current LTV (95.6% on a weighted average basis at 31

December 2009) and geographic profiles (74% outside of Citizen’s

footprint states and a 30% concentration in California, Arizona and

Nevada) have, in the current economic climate, resulted in an

annualised write-off rate of 10.7% in 2009. The SBO book has been

closed to new purchases since the third quarter of 2007 and is in run-

off, with exposure down from $7.0 billion at 31 December 2008 to $5.5

billion at 31 December 2009.

The current weighted average LTV of the real estate portfolio rose

slightly during the year to 72.0% at 31 December 2009 (67.5%

excluding the SBO portfolio), driven by significant price declines

throughout the US. Based on the latest Case-Shiller forecast for the US

market, economists still anticipate significant decreases in the first half

of 2010 with improvements expected in late 2010 or early 2011.

The arrears rate increased significantly from 0.9% at 31 December 2008

to 1.5% at 31 December 2009. In part, this reflects the contraction of

the portfolio caused by fewer new loans added, Citizen choosing to

exercise its option to sell certain mortgages to the secondary market

under long-term agreements, and higher run-off or pay-down rates

across all residential products.

The UK personal lending portfolio, of which 97% is in Core businesses,

comprises credit cards, unsecured loans and overdrafts and totalled £20.3

billion at 31 December 2009, a decrease of 10% from 31 December 2008

(£22.5 billion) due to a general market trend of customers repaying debt

on credit cards and loan balances and a reduction in new lending.

Risk appetite continues to be actively managed across all unsecured

products, reflecting the challenging economic environment. Support

continues for customers in financial difficulties through breathing space

initiatives on all unsecured products, whereby a thirty day period allows

customers to work with a not-for-profit debt advice agency to establish a

debt repayment plan. During this time the Group suspends collection

activity. A further extension of thirty days can be granted if progress is

made and discussions are continuing. Investment in collection and

recovery processes continues, addressing both continued support for our

customers and the management of impairments.

Default rates on both cards and loans in the UK increased in 2009, driven

by the deterioration in the economic environment and, to a lesser extent,

the reduction in total balances. Default rates are still sensitive to economic

developments, notably unemployment rates.

The Citizens credit card portfolio totalled US$2.3 billion, at

31 December 2009. Core assets comprised 58% of the portfolio.

The Citizens cards business adopts conservative risk strategies compared

to the US market as illustrated by the business generally performing better

than industry benchmarks (provided by VISA). The latest available metrics

(December 2009) show the rate for 60+ days delinquency as a percentage

of total outstandings at 4.4% (compared to an industry figure of 4.7%) and

net contractual charge-offs as a percentage of total outstandings at 7.1%

(compared to an industry figure of 7.4%).

For new customers, lending criteria have been tightened and initial

credit lines reduced. Existing customers are regularly monitored for

changes in asset quality and behaviour and, where appropriate,

proactive measures are taken to limit or reduce credit exposure.

Citizens is a leading provider of retail auto financing to US consumers

through a network of 3,500 auto dealers located in 23 US states. It

maintains a conservative, prime indirect auto lending credit programme

with loss rates that have historically been below national averages.

Current outstanding retail auto loan balances totalled $8.8 billion as of

31 December 2009, when the 30-day delinquency rate stood at 2.6%.

This compares to data reported by the American Bankers’ Association

(latest available is at 30 September 2009) showing the nationwide

indirect auto lending delinquency rate at 2.8%. Citizens recently shifted

its focus on auto financing, moving from a nationwide emphasis to its

regional lending footprint. This, together with enhanced collection

activities, has resulted in better than expected loss results. Total portfolio

losses fell from $129.6 million in 2008 to $120.6 million in 2009.