RBS 2009 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

Risk, capital and liquidity management

Credit risk

Credit risk is the risk arising from the possibility that the Group will incur

losses owing to the failure of customers to meet their financial

obligations. The quantum and nature of credit risk assumed in the

Group’s different businesses varies considerably, while the overall credit

risk outcome usually exhibits a high degree of correlation to the

macroeconomic environment. Certain disclosures in this section (pages

127 to 148) are unaudited and are labelled with an asterisk (*).

Principles for credit risk management

The key principles for credit risk management in the Group are as follows:

•A credit risk assessment of the customer and credit facilities is

undertaken prior to approval of credit exposure. Typically, this

includes both quantitative and qualitative elements including: the

purpose of the credit and sources of repayment; compliance with

affordability tests; repayment history; ability to repay; sensitivity to

economic and market developments; and risk-adjusted return based

on credit risk measures appropriate to the customer and facility type;

•Credit risk authority is specifically granted in writing to individuals

involved in the approval of credit extensions. In exercising credit

authority, individuals are required to act independently of business

considerations and must declare any conflicts of interest;

•Credit exposures, once approved, are monitored, managed and

reviewed periodically against approved limits. Lower quality

exposures are subject to more frequent analysis and assessment;

•Credit risk management works with business functions on the ongoing

management of the credit portfolio, including decisions on mitigating

actions taken against individual exposures or broader portfolios;

•Customers with emerging credit problems are identified early and

classified accordingly. Remedial actions are implemented promptly

and are intended to restore the customer to a satisfactory status and

minimise any potential loss to the Group; and

•Stress testing of portfolios is undertaken to assess the potential credit

impact of non-systemic scenarios and wider macroeconomic events

on the Group’s income and capital.

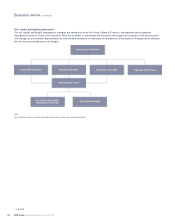

Credit risk organisation

The credit risk function is organised within a divisionally aligned

structure to ensure appropriate proximity to the businesses it covers and

to develop and provide the specialisation required to manage the

associated credit risk. The function comprises a number of activities:

credit approval; transaction/customer assessment; policy formulation

and development (in the context of the Group-wide policy framework);

portfolio reporting; and quantitative portfolio analytics.

In addition to the activities undertaken within divisional functions, a

Group-wide credit risk function sets the overall framework and highest

level credit risk policy standards; produces Group-wide credit risk

portfolio reporting and analysis; and approves credit transactions which

exceed divisional credit authority.

The Group Risk Committee (GRC) considers detailed reports of credit

risk performance such as monthly risk portfolio performance trend

information. The Group Credit Risk Policy Committee, a subcommittee of

the GRC, approves material new credit risk policy standards.

For wholesale credit portfolios, an updated Group-wide credit approval

and authority framework was introduced in early 2009, replacing the

previous structure of credit committees. The authority held by an

individual in respect of a particular extension of credit is determined by

a Group-wide credit approval grid which links total credit limit amount

for a customer group with customer credit quality (expressed as a credit

grade) and the individual’s credit experience and expertise (which

determines the authority level assigned to them). The Executive Credit

Group (ECG) considers credit decisions which exceed the delegated

authorities of individuals throughout the Group.

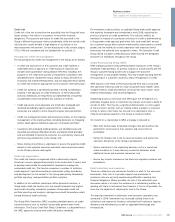

Global Restructuring Group (GRG)

GRG manages problem and potential problem exposures in the Group’s

wholesale credit portfolios. Its primary function is to work closely with the

Group’s customer facing businesses to support the proactive

management of any problem lending. This may include assisting with the

restructuring of a customer’s business and/or renegotiation of credit.

GRG reports to the Head of Restructuring and Risk and is structured

with specialist teams focused on: large corporate cases (higher value,

multiple lenders); small and medium size business cases (lower value,

bilateral relationships); and recovery/litigations.

Originating business units liaise with GRG upon the emergence of a

potentially negative event or trend that may impact a borrower’s ability to

service its debt. This may be a significant deterioration in some aspect

of the borrower’s activity, such as trading, where a breach of covenant

is likely or where a borrower has missed or is expected to miss a

material contractual payment to the Group or another creditor.

On transfer of a relationship to GRG a strategy is devised to:

•Work with the borrower to facilitate changes that will maximise the

potential for turnaround of their situation and return them to

profitability;

•Define the Group’s role in the turnaround situation and assess the

risk/return dimension of the Group’s participation;

•Return customers to the originating business unit in a sound and

stable condition or, if such recovery cannot be achieved, avoid

additional losses and maximise recoveries; and

•Ensure key lessons learned are fed back into origination policies and

procedures.

Retail collections and recoveries

There are collections and recoveries functions in each of the consumer

businesses. Their role is to provide support and assistance to

customers who are currently experiencing difficulties meeting their

financial obligations. Where possible, the aim of the collections and

recoveries teams is to return the customer to a satisfactory position, by

working with them to restructure their finances. If this is not possible, the

team has the objective of reducing the loss to the Group.

The ongoing investment in collections and recoveries operations has

continued in 2009. Investment has increased staffing levels in all

collections and recoveries functions, enhanced staff training to improve

efficiency and effectiveness as well as upgraded technology and

infrastructure.

127RBS Group Annual Report and Accounts 2009