RBS 2009 Annual Report Download - page 337

Download and view the complete annual report

Please find page 337 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

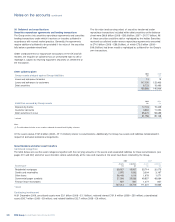

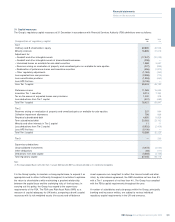

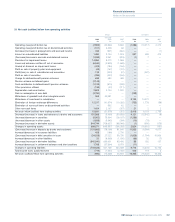

335RBS Group Annual Report and Accounts 2009

Financial statements

Notes on the accounts

In particular there is continuing political and regulatory scrutiny of the

operation of the retail banking and consumer credit industries in the

United Kingdom and elsewhere. The nature and impact of future

changes in policies and regulatory action are not predictable and are

beyond the Group’s control but could have an adverse impact on the

Group’s businesses and earnings.

Retail banking

In the European Union, regulatory actions included an inquiry into retail

banking initiated on 13 June 2005 in all of the then 25 member states by

the European Commission’s Directorate General for Competition. The

inquiry examined retail banking in Europe generally. On 31 January

2007, the European Commission announced that barriers to competition

in certain areas of retail banking, payment cards and payment systems

in the European Union had been identified. The European Commission

indicated that it will consider using its powers to address these barriers

and will encourage national competition authorities to enforce European

and national competition laws where appropriate.

Multilateral interchange fees

In 2007, the European Commission issued a decision that while

interchange is not illegal per se, MasterCard’s current multilateral

interchange fee (“MIF”) arrangement for cross border payment card

transactions with MasterCard and Maestro branded consumer credit

and debit cards in the European Union are in breach of competition law.

MasterCard was required by the decision to withdraw the relevant

cross-border MIFs (i.e. set these fees to zero) by 21 June 2008.

MasterCard appealed against the decision to the European Court of

First Instance on 1 March 2008, and the Group has intervened in the

appeal proceedings. In addition, in Summer 2008, MasterCard

announced various changes to its scheme arrangements. The European

Commission was concerned that these changes might be used as a

means of circumventing the requirements of the infringement decision.

In April 2009 MasterCard agreed an interim settlement on the level of

cross-border MIF with the European Commission pending the outcome

of the appeal process and, as a result, the European Commission has

advised it will no longer investigate the non-compliance issue (although

MasterCard is continuing with its appeal).

Visa’s cross-border MIFs were exempted in 2002 by the European

Commission for a period of five years up to 31 December 2007 subject

to certain conditions. On 26 March 2008, the European Commission

opened a formal inquiry into Visa’s current MIF arrangements for cross

border payment card transactions with Visa branded debit and

consumer credit cards in the European Union and on 6 April 2009 the

European Commission announced that it had issued Visa with a formal

Statement of Objections. At the same time Visa announced changes to

its interchange levels and introduced some changes to enhance

transparency. There is no deadline for the closure of the inquiry.

In the UK, the OFT has carried out investigations into Visa and

MasterCard domestic credit card interchange rates. The decision by the

OFT in the MasterCard interchange case was set aside by the

Competition Appeal Tribunal (the “CAT”) in June 2006. The OFT’s

investigations in the Visa interchange case and a second MasterCard

interchange case are ongoing. On 9 February 2007, the OFT

announced that it was expanding its investigation into domestic

interchange rates to include debit cards. In January 2010 the OFT

advised that it did not anticipate issuing a Statement of Objections prior

to the European Court’s judgment, although it has reserved the right to

do so if it considers it appropriate.

The outcome of these investigations is not known, but they may have an

impact on the consumer credit industry in general and, therefore, on the

Group’s business in this sector.

Payment Protection Insurance

Having conducted a market study relating to Payment Protection

Insurance (“PPI”), on 7 February 2007 the OFT referred the PPI market

to the Competition Commission (“CC”) for an in-depth inquiry. The CC

published its final report on 29 January 2009 and announced its

intention to order a range of remedies, including a prohibition on

actively selling PPI at point of sale of the credit product (and for 7 days

thereafter), a ban on single premium policies and other measures to

increase transparency (in order to improve customers’ ability to search

and improve price competition). Barclays Bank PLC subsequently

appealed certain CC findings to the Competition Appeal Tribunal

(“CAT”). On 16 October 2009, the CAT handed down a judgment

quashing the ban on selling PPI at the point of sale of credit products

and remitted the matter back to the CC for review. The CC’s current

Administrative Timetable is to publish a supplementary report by

Summer 2010 and give further consideration to its full range of

recommended remedies and a draft order to implement them during

Autumn 2010.

The FSA has been conducting a broad industry thematic review of PPI

sales practices and in September 2008, the FSA announced that it

intended to escalate its level of regulatory intervention. Substantial

numbers of customer complaints alleging the mis-selling of PPI policies

have been made to banks and to the FOS and many of these are being

upheld by the FOS against the banks.

In September 2009, the FSA issued a consultation paper on guidance

on the fair assessment of PPI mis-selling complaints and, where

necessary, the provision of an appropriate level of redress. The

consultation also covers proposed rules requiring firms to re-assess

(against the new guidance) all PPI mis-selling complaints received and

rejected since 14 January 2005. A policy statement containing final

guidance and rules is expected in early 2010. Separately, discussions

continue between the FSA and the Group in respect of concerns

expressed by the FSA over certain categories of historical PPI sales.

Personal current accounts

On 16 July 2008, the OFT published the results of its market study into

personal current accounts in the United Kingdom. The OFT found

evidence of competition and several positive features in the personal

current account market but believes that the market as a whole is not

working well for consumers and that the ability of the market to function

well has become distorted.

On 7 October 2009, the OFT published a follow-up report summarising

the initiatives agreed between the OFT and personal current account

providers to address the OFT’s concerns about transparency and

switching, following its market study. Personal current account providers

will take a number of steps to improve transparency, including providing

customers with an annual summary of the cost of their account and

making charges prominent on monthly statements. To improve the

switching process, a number of steps are being introduced following

work with BACS, the payment processor, including measures to reduce

the impact on consumers of any problems with transferring direct

debits.