RBS 2009 Annual Report Download - page 386

Download and view the complete annual report

Please find page 386 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

376 -

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390

|

|

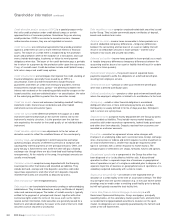

Shareholder information continued

RBS Group Annual Report and Accounts 2009384

Credit derivative product company (CDPC) is a special purpose entity

that sells credit protection under credit default swaps or certain

approved forms of insurance policies. Sometimes they can also buy

credit protection. CDPCs are similar to monoline insurers. However,

unlike monoline insurers, they are not regulated as insurers.

Credit derivatives are contractual agreements that provide protection

against a credit event on one or more reference entities or financial

assets. The nature of a credit event is established by the protection

buyer and protection seller at the inception of a transaction, and such

events include bankruptcy, insolvency or failure to meet payment

obligations when due. The buyer of the credit derivative pays a periodic

fee in return for a payment by the protection seller upon the occurrence,

if any, of a credit event. Credit derivatives include credit default swaps,

total return swaps and credit swap options.

Credit enhancements are techniques that improve the credit standing of

financial obligations; generally those issued by an SPE in a

securitisation. External credit enhancements include financial

guarantees and letters of credit from third-party providers. Internal

enhancements include excess spread – the difference between the

interest rate received on the underlying portfolio and the coupon on the

issued securities; and over-collateralisation – on securitisation, the value

of the underlying portfolio is greater than the securities issued.

Credit risk assets – loans and advances (including overdraft facilities),

instalment credit, finance lease receivables and other traded

instruments across all customer types.

Credit risk spread is the difference between the coupon on a debt

instrument and the benchmark or the risk-free interest rate for the

instrument’s maturity structure. It is the premium over the risk-free

rate required by the market for the credit quality of an individual debt

instrument.

Credit valuation adjustments are adjustments to the fair values of

derivative assets to reflect the creditworthiness of the counterparty.

Currency swap – an arrangement in which two parties exchange

specific principal amounts of different currencies at inception and

subsequently interest payments on the principal amounts. Often, one

party will pay a fixed interest rate, while the other will pay a floating

exchange rate (though there are also fixed-fixed and floating-floating

arrangements). At the maturity of the swap, the principal amounts are

usually re-exchanged.

Customer accounts comprise money deposited with the Group by

counterparties other than banks and classified as liabilities. They

include demand, savings and time deposits; securities sold under

repurchase agreements; and other short term deposits. Deposits

received from banks are classified as deposits by banks.

Debt restructuring – see renegotiated loans.

Debt securities are transferable instruments creating or acknowledging

indebtedness. They include debentures, bonds, certificates of deposit,

notes and commercial paper. The holder of a debt security is typically

entitled to the payment of principal and interest, together with other

contractual rights under the terms of the issue, such as the right to

receive certain information. Debt securities are generally issued for a

fixed term and redeemable by the issuer at the end of that term. Debt

securities can be secured or unsecured.

Debt securities in issue comprise unsubordinated debt securities issued

by the Group. They include commercial paper, certificates of deposit,

bonds and medium-term notes.

Deferred tax asset – income taxes recoverable in future periods as a

result of deductible temporary differences – temporary differences

between the accounting and tax base of an asset or liability that will

result in tax deductible amounts in future periods – and the carry-

forward of tax losses and unused tax credits.

Deferred tax liability – income taxes payable in future periods as a result

of taxable temporary differences (temporary differences between the

accounting and tax base of an asset or liability that will result in taxable

amounts in future periods).

Defined benefit obligation – the present value of expected future

payments required to settle the obligations of a defined benefit plan

resulting from employee service.

Defined benefit plan – pension or other post-retirement benefit plan

other than a defined contribution plan.

Defined contribution plan – pension or other post-retirement benefit plan

where the employer’s obligation is limited to its contributions to the fund.

Delinquency - a debt or other financial obligation is considered

delinquent when one or more contractual payments are overdue.

Delinquency is usually defined in terms of days past due. Delinquent

and in arrears are synonymous.

Deposits by banks comprise money deposited with the Group by banks

and recorded as liabilities. They include money-market deposits,

securities sold under repurchase agreements, federal funds purchased

and other short term deposits. Deposits received from customers are

recorded as customer accounts.

Derivative – a contract or agreement whose value changes with

changes in an underlying index such as interest rates, foreign exchange

rates, share prices or indices and which requires no initial investment or

an initial investment that is smaller than would be required for other

types of contracts with a similar response to market factors. The

principal types of derivatives are: swaps, forwards, futures and options.

Discontinued operation is a component of the Group that either has

been disposed of or is classified as held for sale. A discontinued

operation is either: a separate major line of business or geographical

area of operations or part of a single co-ordinated plan to dispose of a

separate major line of business or geographical area of operations; or a

subsidiary acquired exclusively with a view to resale.

Exposure at default (EAD) – an estimate of the expected level of

utilisation of a credit facility at the time of a borrower’s default. The EAD

may be higher than the current utilisation (e.g. in the case where further

drawings may be made under a revolving credit facility prior to default)

but will not typically exceed the total facility limit.

Fannie Mae (Federal National Mortgage Association) is a US

Government Sponsored Enterprise. It buys mortgages, principally

issued by banks, on the secondary market, pools them, and sells them

as residential mortgage-backed securities to investors on the open

market. Its obligations are not explicitly guaranteed by the full faith and

credit of the US Government.