RBS 2009 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

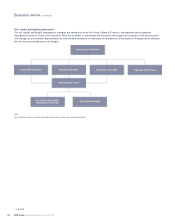

Risk, capital and liquidity management

In addition to the calculation of minimum capital requirements for credit,

market and operational risk, banks are required to undertake an

Individual Capital Adequacy Assessment Process (ICAAP) for other

risks. The Group’s ICAAP, in particular, focuses on pension fund risk,

interest rate risk in the banking book together with stress tests to assess

the adequacy of capital over one year and the economic cycle.

The Group publishes its Pillar 3 (Market disclosures) on its website,

providing a range of additional information relating to Basel II and risk

and capital management across the Group. The disclosures focus on

Group level capital resources and adequacy, discuss a range of credit

risk approaches and their associated RWAs under various Basel II

approaches such as credit risk mitigation, counterparty credit risk and

provisions. Detailed disclosures are also made on equity, securitisation,

operational and market risk, as well as providing Interest Rate Risk in

the Banking Book disclosures.

Stress and scenario testing

Stress testing forms part of the Group’s risk and capital framework and

an integral component of Basel II. As a key risk management tool,

stress testing highlights to senior management potential adverse

unexpected outcomes related to a mixture of risks and provides an

indication of how much capital might be required to absorb losses,

should adverse scenarios occur. Stress testing is used at both a

divisional and Group level to assess risk concentrations, estimate the

impact of stressed earnings, impairments and write-downs on capital. It

determines the overall capital adequacy under a variety of adverse

scenarios. The principal business benefits of the stress testing

framework include: understanding the impact of recessionary

scenarios; assessing material risk concentrations; forecasting the

impact of market stress and scenarios on the Group’s balance sheet

liquidity.

At Group level, a series of stress events are monitored on a regular

basis to assess the potential impact of an extreme yet plausible event

on the Group. There are four core elements of scenario stress testing:

•Macroeconomic stress testing considers the impact on both

earnings and capital for a range of scenarios. They entail multi-year

systemic shocks to assess the Group’s ability to meet its capital

requirements and liabilities as they fall due under a downturn in the

business cycle and/or macroeconomic environment;

•Enterprise wide stress testing considers scenarios that are not

macroeconomic in nature but are sufficiently broad in nature to

impact across multiple risks or divisions and are likely to impact

earnings, capital and funding;

•Cross-divisional stress testing includes scenarios which have

impacts across divisions relating to sensitivity to a common risk

factor(s). This would include sector based stress testing across

corporate portfolios and sensitivity analysis to stress in market

factors. These stress tests are discussed with senior divisional

management and are reported to senior committees across the

Group; and

•Divisional and risk specific stress testing is undertaken to support

risk identification and management. Current examples include the

daily product based stress testing using a hybrid of hypothetical and

historical scenarios within market risk.

Portfolio analysis, using historic performance and forward looking

indicators of change, uses stress testing to facilitate the measurement

of potential exposure to events and seeks to quantify the impact of an

adverse change in factors which drive the performance and profitability

of a portfolio.

125RBS Group Annual Report and Accounts 2009