RBS 2009 Annual Report Download - page 282

Download and view the complete annual report

Please find page 282 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Notes on the accounts continued

RBS Group Annual Report and Accounts 2009280

Credit valuation adjustments (CVA) represent an estimate of the

adjustment to fair value that a market participant would make to

incorporate the credit risk inherent in counterparty derivative exposures.

The Group makes such credit adjustments to derivative exposures it has

to counterparties, as well as debit valuation adjustments to liabilities

issued by the Group. CVA is discussed in Risk, capital and liquidity

management – Market turmoil exposures – Credit valuation adjustments

(pages 193 to 199). Bid-offer and liquidity reserves and own credit are

discussed below.

Bid-offer and liquidity reserves

Trading positions are adjusted to bid (for assets) or offer (for liabilities)

levels, by marking individual cash based positions directly to bid or offer

or by taking bid-offer reserves calculated on a portfolio basis for

derivatives.

The bid-offer approach is based on current market spreads and

standard market bucketing of risk. Risk data is used as the primary

source of information within bid-offer calculations and is aggregated

when it is more granular than market standard buckets.

Bid-offer adjustments for each risk factor are determined by

aggregating similar risk exposures arising on different products.

Additional basis bid/offer reserves are taken where these are charged in

the market. Risk associated with non identical underlying exposures is

not netted down unless there is evidence that the cost of closing the

combined risk exposure is less than the cost of closing on an individual

basis. For example: interest rate delta bid-offer methodology (when

viewed in isolation) allows aggregation of risk across different tenor

bases. Tenor basis bid-offer reserves are then applied to compensate

for the netting within the (original) delta bid-offer calculation.

Bid-offer spreads vary by maturity and risk type to reflect different

spreads in the market. For positions where there is no observable quote,

the bid-offer spreads are widened in comparison to proxies to reflect

reduced liquidity or observability. Bid-offer methodologies also

incorporate liquidity triggers whereby wider spreads are applied to risks

above pre-defined thresholds.

Netting is applied across risk buckets where there is market evidence to

support this. For example calendar netting and cross strike netting

effects are taken into account where such trades occur regularly within

the market. Netting will also apply where long and short risk in two

different risk buckets can be closed out in a single market transaction at

less cost than via two separate transactions (closing out the individual

bucketed risk in isolation).

Vanilla risk on exotic products is typically reserved as part of the overall

portfolio based calculation e.g. delta and vega risk is included within the

delta and vega bid-offer calculations. Aggregation of risk arising from

different models is in line with the Group’s risk management practices;

the model review control process considers the appropriateness of

model selection in this respect.

Product related risks such as correlation risk attract specific bid to offer

reserves. Additional reserves are provided for exotic products to ensure

overall reserves match market close-out costs. These market close-out

costs inherently incorporate risk decay and cross-effects which are

unlikely to be adequately reflected in the static hedge based on vanilla

instruments.

Where there is limited bid-offer information for a product a conservative

approach is taken, taking into account pricing approach and risk

management strategy.

Market risk close-out costs excluding CVA were £2,814 million as at 31

December 2009 (2008 – £3,260 million; 2007 – £1,154 million).

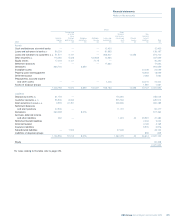

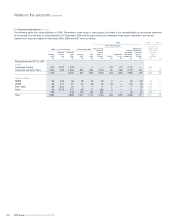

11 Financial instruments continued

Valuation reserves

When valuing financial instruments in the trading book, adjustments are made to mid-market valuations to cover bid-offer spread, liquidity and

credit risk.

Valuation reserves and adjustments comprise:

2009 2008 2007

£m £m £m

Credit valuation adjustments:

Monoline insurers 3,796 5,988 862

CDPCs 499 1,311 44

Other counterparties 1,588 1,738 263

5,883 9,037 1,169

Bid-offer and liquidity reserves 2,814 3,260 1,154

8,697 12,297 2,323

Debit valuation adjustments:

Debt securities in issue (2,331) (2,373) (456)

Derivatives (467) (450) —

Total debit valuation adjustments (2,798) (2,823) (456)

Total reserves 5,899 9,474 1,867