RBS 2009 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

97RBS Group Annual Report and Accounts 2009

Business review

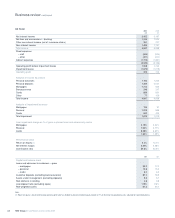

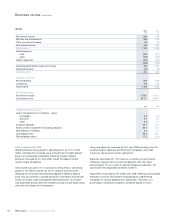

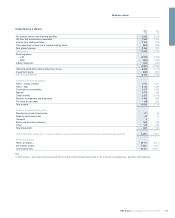

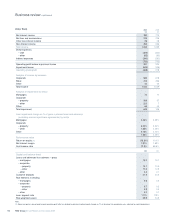

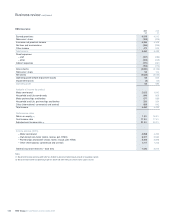

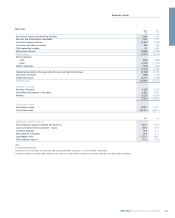

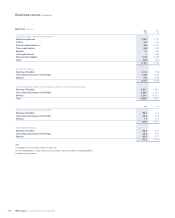

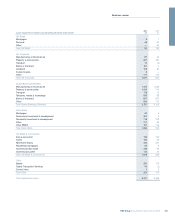

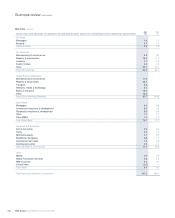

2009 compared with 2008

Operating results were in line with expectations but deteriorated during

2009 as economic conditions across the island of Ireland worsened,

with an operating loss for the year of £368 million.

Net interest income declined by 7% in constant currency terms, largely

as a result of tightening deposit margins in an increasingly competitive

market, partly offset by asset repricing initiatives. Net interest margin for

the year at 1.87% remained broadly stable despite the challenging

market conditions.

At constant exchange rates loans to customers decreased by 4% from

the prior year as new business demand weakened. Customer deposits

reduced by 5% in 2009 in constant currency terms, reflecting an

increasingly competitive Irish deposit market and reductions in

wholesale funding during the first quarter. During the second half of the

year the market stabilised and the division recorded strong growth in

customer balances resulting in an improved funding profile.

Non-interest income declined by 12% in constant currency terms due to

lower fee income driven by reduced activity levels across all business

lines.

Total costs for the year were flat on a constant currency basis. Direct

expenses were down 12% in constant currency terms during 2009,

driven by the bank’s restructuring programme, which incorporates the

merger of the First Active and Ulster Bank businesses. The rollout of the

programme has resulted in a downward trend in direct expenses

throughout 2009. The reduction in direct expenses has been offset by a

17% increase in indirect expenses primarily reflecting provisions relating

to the bank’s own property recognised in the fourth quarter.

Impairment losses increased to £649 million from £106 million driven by

the continued deterioration in the Irish economic environment and

resultant impact on loan performance across the retail and wholesale

portfolios.

Necessary fiscal budgetary action allied to the well-entrenched

downturn in property markets in Ireland has fed through to higher loan

losses. Mortgage impairments have been driven by rising

unemployment and lower incomes. Loans to the property sector

experienced a substantial rise in defaults as the Irish property market

declined, reflecting the difficult economic backdrop and the uncertainty

surrounding the possible effect of the Irish Government's National Asset

Management Agency on asset values. Sectors driven by consumer

spending have been affected by the double digit decline in 2009 with

rising default rates evident.

Customer account numbers increased by 3% during 2009, with growth

fuelled by strong current account activity and new-to-bank savings

customers.