RBS 2009 Annual Report Download - page 201

Download and view the complete annual report

Please find page 201 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

Risk, capital and liquidity management

199RBS Group Annual Report and Accounts 2009

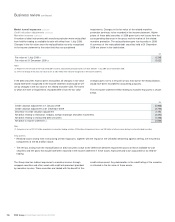

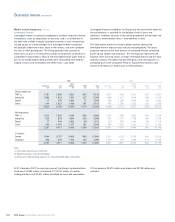

CVA attributable to other counterparties

The CVA for all other counterparties is calculated on a portfolio basis

reflecting an estimate of the amount a third party would charge to

assume the credit risk.

Expected losses are determined from the market implied probability of

defaults and internally assessed recovery levels. The probability of

default is calculated with reference to observable credit spreads and

observable recovery levels. For counterparties where observable data

do not exist, the probability of default is determined from the average

credit spreads and recovery levels of baskets of similarly rated entities.

A weighting of 50% to 100% is applied to arrive at the CVA. The

weighting reflects portfolio churn and varies according to the

counterparty credit quality.

Expected losses are applied to estimated potential future exposures

which are modelled to reflect the volatility of the market factors which

drive the exposures and the correlation between those factors. Potential

future exposures arising from vanilla products (including interest rate

and foreign exchange derivatives) are modelled jointly using the Group’s

core counterparty risk systems. At 31 December 2009, over 75% of the

Group’s CVA held in relation to other counterparties arises on these

vanilla products. The exposures arising from all other product types are

modelled and assessed individually. The potential future exposure to

each counterparty is the aggregate of the exposures arising on the

underlying product types.

Correlation between exposure and counterparty risk is also

incorporated within the CVA calculation where this risk is considered

significant. The risk primarily arises on trades with emerging market

counterparties where the gross mark-to-market value of the trade, and

therefore the counterparty exposure, increases as the strength of the

local currency declines.

Collateral held under a credit support agreement is factored into the

CVA calculation. In such cases where the Group holds collateral against

counterparty exposures, CVA is held to the extent that residual risk

remains.

CVA is held against exposures to all counterparties with the exception

of the CDS protection that the Group has purchased from HMT, as part

of its participation in the APS, due to the unique features of this

derivative.

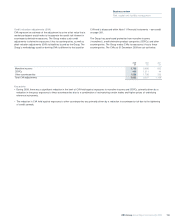

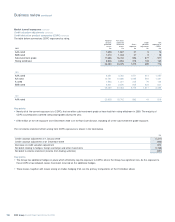

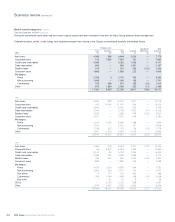

The net income statement effect arising from the change in level of CVA for all other counterparties and related trades is shown in the table below.

£m

Credit valuation adjustment at 1 January 2009 (1,738)

Credit valuation adjustment at 31 December 2009 (1,588)

Decrease in credit valuation adjustment 150

Net debit relating to hedges, foreign exchange and other movements (841)

Net debit to income statement (income from trading activities) (691)

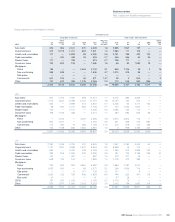

Key points

•Losses arose on trades hedging the CVA held against other counterparties due to the tightening of credit spreads. These losses, together with

realised losses from counterparty defaults, are the primary cause of the loss arising on foreign exchange, hedges, realisations and other

movements.

•The net income statement effect was driven by updates to the CVA methodology, hedges and realised defaults off-setting CVA movements.

–The primary update applied to the CVA methodology reflected a market wide shift in the approach to pricing and managing counterparty risk.

The methodology change related to the calculation of the probability of default. The basis for this calculation moved from a blended market

implied and historic measure to the market implied methodology set out above. Other updates to the methodology were made to reflect the

correlation between exposure and counterparty risk.

–Prior to the update to the CVA methodology, CVA moves driven by changes to the historic element of the blended measure were not hedged,

resulting in losses during the year arising from related CVA increases.

–The CVA is calculated on a portfolio basis and reflects an estimate of the losses that will arise across the portfolio due to counterparty defaults.

It is not possible to perfectly hedge the risks driving the CVA and this leads to differences between CVA and hedge movements. Differences

also arise between realised default losses and the proportion of CVA held in relation to individual counterparties.