RBS 2009 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

RBS Group Annual Report and Accounts 200994

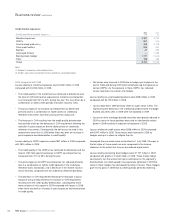

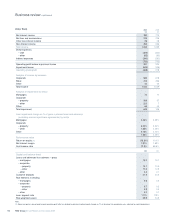

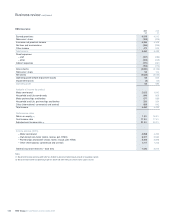

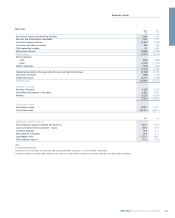

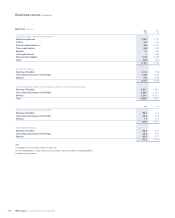

2009 compared with 2008

Operating profit improved to £5,709 million in 2009, compared with an

operating loss of £1,796 million in 2008. Although the buoyant market

conditions experienced in the first quarter levelled off over the course of

the year, the refocusing of the business on its core franchises was

successful. GBM has tightened its balance sheet management over the

course of the year, with disciplined deployment of capital to support its

targeted client base.

In an often volatile market environment, GBM responded quickly to its

clients’ needs to strengthen their balance sheets and to take advantage

of the attractive environment for debt and equity issues. RBS

participated in the five largest equity issues worldwide in 2009, and in

six out of the ten largest debt capital markets transactions.

Income grew significantly, reflecting a very strong first quarter benefiting

from market volatility, client activity and a marked improvement from

Credit Markets. Rates flow business, up 127%, benefited from good

client activity, while strong equity capital markets drove a fourfold

increase in Equities.

Portfolio management and origination grew 39% as financial institutions

and corporate clients refinanced through the debt capital markets. The

refocused Credit Markets delivered a much improved result from greater

liquidity and a more positive trading environment.

Despite quarterly movement in the Group’s credit spreads, overall

spreads remained broadly flat over the year resulting in a small loss

from movements in the fair value of own debt compared with a £357

million gain in 2008.

Expenses increased 17%, reflecting higher performance-related costs

and the impact of adverse exchange rate movements, partly offset by

restructuring and efficiency benefits. Less than half of the change in

staff costs related to increases in 2009 bonus awards.

Staff costs represented 27% of income. The Group introduced new

deferral policies in 2009, which have led to changes in accrual patterns.

Adjusting for both 2008 and 2009 deferrals, GBM’s compensation ratio

in 2009 would have been 28%.

Higher impairments principally reflected a large individual failure

recognised in the third quarter. Impairments represented 0.59% of loans

and advances to customers compared with 0.29% in the prior year,

reflecting the marked reduction in loans and advances.

Total third party assets, excluding derivatives, were down 17%, or 13%

at constant exchange rates, compared with 31 December 2008, driven

by a 43% reduction in loans and advances as customers took

advantage of favourable capital market conditions to raise alternative

forms of finance to bank debt. This reduction was partially offset by an

increase in liquid assets.

Risk-weighted assets decreased 19%, or 15% at constant exchange

rates, reflecting the fall in third party assets and the Group’s continued

focus on reducing its risk profile and balance sheet usage.

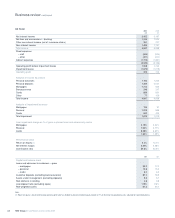

Global Banking & Markets continued

2009 2008

£bn £bn

Capital and balance sheet

Loans and advances (including banks) 127.8 224.2

Reverse repos 73.3 88.8

Securities 106.0 127.5

Cash and eligible bills 74.0 20.2

Other assets 31.1 38.0

Total third party assets (excluding derivatives mark to market) 412.2 498.7

Net derivative assets (after netting) 68.0 121.0

Customer deposits (excluding repos) 46.9 87.8

Risk elements in lending 1.8 0.9

Loan:deposit ratio 194% 192%

Risk-weighted assets 123.7 151.8

Business review continued