RBS 2009 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009166

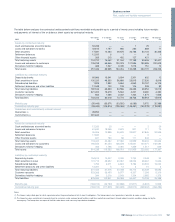

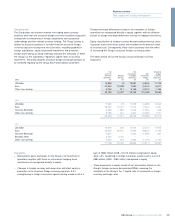

Percent increase/(decrease)

in CFG EVE(1)

2% parallel 2% parallel

upward downward

movement movement

in US in US

interest rates interest rates(2)

Period end (4.3) (23.4)

Maximum (4.3) (24.6)

Minimum 4.6 (18.4)

Average (0.8) (22.2)

Notes:

(1) Economic value of equity is the net present value (NPV) of assets and liabilities calculated by discounting expected cash flows of each instrument over its expected life. Risk to EVE is quantified

by calculating the impact of interest rate changes on the net present value of equity and is expressed as a percentage of CFG regulatory capital.

(2) No negative rates allowed.

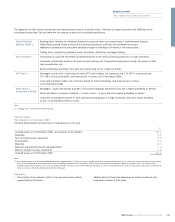

Sensitivity of net interest income*

There have been no material changes to the Group’s measurement of,

and management philosophy towards, sensitivity of net interest income

to movement in interest rates. The Group aims to be relatively neutral to

directional shifts in interest rates. It seeks to mitigate the effect of

prospective interest movements which could reduce future net interest

income, whilst balancing the cost of such hedging activities on the

current net revenue stream.

The following table shows the sensitivity of net interest income over

the next twelve months to an immediate up and down 1% change to all

interest rates.

Market risk continued

Structural interest rate risk continued

Citizens Economic Value of Equity (EVE)*

Generally, Citizens is the main contributor to overall non-trading interest

rate VaR. Citizens aims, through its management of market risk in non-

trading portfolios, to mitigate the effect of prospective interest

movements which could reduce future net interest income, whilst

balancing the cost of such hedging activities on the current net revenue

stream. To do so it uses a variety of income simulation and valuation risk

measures that more effectively capture the risk to earnings due to

mortgage prepayment and competitive deposit pricing behaviour than a

VaR-based methodology. IRRBB is managed within approved limits on

interest rate risk, liquidity and capitalisation, with a goal of optimising

yield.

In addition to net interest income sensitivity Citizens also measures the

sensitivity of the value of the net interest margin to changes in interest

rates on a monthly basis. This measure is called EVE sensitivity. The

table below details this sensitivity at the end of 2009 and the maximum

and minimum month-end figures.

2009 2008

£m £m

+ 100bp shift in yield curves 510 139

– 100bp shift in yield curves (687) (234)

The base case projected net interest income is based on the Group’s

current balance sheet, forwards rate paths implied by the yield curve as

at 31 December 2009 and using contractual repricing dates. Where

contractual repricing dates are not held an estimate of the likely timing

and extent of any rate change is used. The projection also includes the

expected effects of behavioural options such as the prepayment of

residential mortgages.

The above sensitivities show how this projected net interest income would

change in response to an immediate parallel shift to all market rates.

The scenarios used are simplified in that they assume all interest rates

for all currencies and maturities move at the same time and by the same

amount and therefore do not reflect the potential effect on net interest

income of some rates changing whilst others remain the same. The

scenarios also do not incorporate actions that would be taken by the

business units to mitigate the effect of this interest rate risk.

The Group’s asset sensitive position has increased in 2009. The primary

contributors to the change are enhanced modelling of embedded

deposit floors, active position management to benefit from the impact of

a tightening US monetary policy regime by Citizens Financial Group and

the impact of not fully hedging the interest rate exposure related to the

APS capital proceeds which were received in late December.

The projections do not take into account the effect on net interest

income of anticipated differences in changes between interest rates

and interest rates linked to other bases (such as central bank rates or

product rates for which the entity has discretion over the timing and

extent of rate changes). The projections make other simplifying

assumptions, including that all positions run to maturity and that there

are no negative interest rates.

* unaudited