RBS 2009 Annual Report Download - page 157

Download and view the complete annual report

Please find page 157 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

Risk, capital and liquidity management

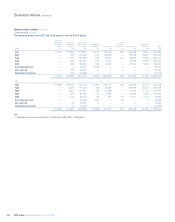

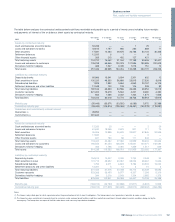

155RBS Group Annual Report and Accounts 2009

Stress testing

The Group performs stress tests to simulate how events may impact its

funding and liquidity capabilities. Such tests assist in the planning of the

overall balance sheet structure, help define suitable limits for control of

the risk arising from the mismatch of maturities across the balance

sheet and from undrawn commitments and other contingent obligations,

and feed into the risk appetite and contingency funding plan. The form

and content of stress tests are updated where required as market

conditions evolve. These stresses include the following scenarios:

•Idiosyncratic stress: an unforeseen, name-specific, liquidity stress, with

the initial short-term period of stress lasting for at least two weeks;

•Market stress: an unforeseen, market-wide liquidity stress of three

months duration;

•Idiosyncratic and market stress: a combination of idiosyncratic and

market stress;

•Rating downgrade: one and two notch long-term credit rating

downgrade scenarios; and

•Daily market lockout: no access to unsecured funding and no

funding rollovers are possible.

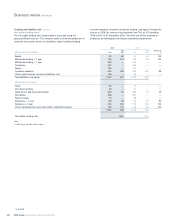

Contingency planning

Contingency funding plans have been developed which incorporate

early warning indicators to monitor market conditions. The Group

reviews its contingency funding plans in the light of evolving market

conditions and stress test results. The contingency funding plans cover:

the available sources of contingent funding to supplement cash flow

shortages; the lead times to obtain such funding; the roles and

responsibilities of those involved in the contingency plans; the

communication and escalation requirements when early warning

indicators signal deteriorating market conditions; and the ability and

circumstances within which the Group accesses central bank liquidity.

Monitoring

Liquidity risk is constantly monitored to evaluate the Group’s position

having regard to its risk appetite and key metrics. Daily, weekly and

monthly monitoring and control processes are in place, which allow

management to take appropriate action. Actions taken to improve the

liquidity risk include a focus on improving the loan to deposit ratio,

issuing longer-term wholesale funding, both guaranteed and

unguaranteed, and the size of the conduit commitments. Metrics

include, but are not limited to;

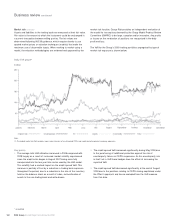

Wholesale funding > one year: As the wholesale funding markets have

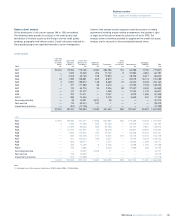

improved over the course of 2009 the Group has been better able to

manage both its short and longer-term funding requirements and has

significantly reduced its reliance on central bank funding. In 2009, the

Group issued £21 billion of public, private and structured unguaranteed

debt securities with a maturity greater than one year including issuances

with maturities of ten years and five years of £3 billion and £2 billion

respectively. To provide protection from liquidity risk in these markets the

Group targets a ratio of wholesale funding greater than one year. The

proportion of outstanding debt instruments issued with a remaining

maturity of greater than 12 months has increased from 45% at 31

December 2008 to 50% at 31 December 2009, reflecting a lengthening

of the maturity profile of debt issuance over the period. The Group is

also targeting an absolute funding reliance (unsecured wholesale

funding with a residual maturity of less than one year) of less than £150

billion by 2013. The 2013 target can also be segmented further into

bank deposits of less than £65 billion and other unsecured wholesale

funding of less than £85 billion. The reliance on wholesale funding has

improved from £343 billion at 31 December 2008 to £249 billion at

December 2009 (and this figure includes

£109 billion of bank deposits).

In common with other UK banks, the Group has benefited from the UK

Government’s scheme to guarantee debt issuance. At 31 December

2009 the Group had debt securities in issue amounting to £52 billion

(2008 – £32 billion), which is approximately 38% of the total UK

Government guaranteed debt.

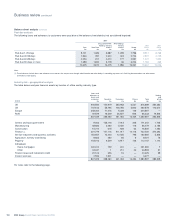

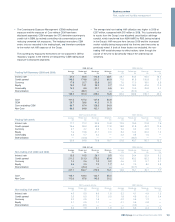

Loan to deposit ratio: The Group monitors the loan to deposit ratio as

a key metric. This ratio has decreased from 118% at 31 December 2008

to 104% at 31 December 2009 for Core and from 151% at 31 December

2008 to 134% at 31 December 2009 for the Group. The Group has a

target of 100% for 2013. The gap between customer loans and

customer deposits (excluding repos) narrowed by £91 billion from £233

billion at 31 December 2008 to £142 billion at 31 December 2009.