RBS 2009 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009142

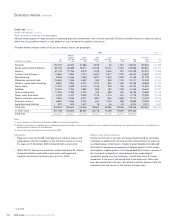

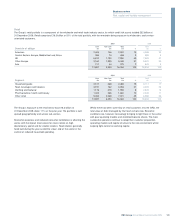

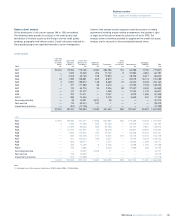

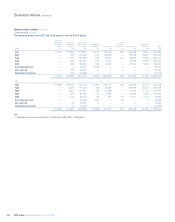

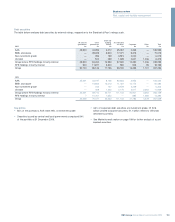

Risk elements in lending and potential problem loans by division Total

Total provision

REIL Total provision as as % of

REIL PPL & PPL provision % of REIL REIL & PPL

£m £m £m £m % %

2009

UK Retail 4,641 — 4,641 2,677 58 58

UK Corporate 2,330 97 2,427 1,271 55 52

Wealth 218 38 256 55 25 21

Global Banking & Markets 1,800 131 1,931 1,289 72 67

Global Transaction Services 197 4 201 189 96 94

Ulster Bank 2,260 2 2,262 962 43 43

US Retail & Commercial 643 — 643 478 74 74

Core 12,089 272 12,361 6,921 57 56

Non-Core 22,900 652 23,552 8,252 36 35

Group before RFS Holdings minority interest 34,989 924 35,913 15,173 43 42

RFS Holdings minority interest 3,260 85 3,345 2,110 65 63

38,249 1,009 39,258 17,283 45 44

2008

UK Retail 3,832 — 3,832 2,086 54 54

UK Corporate 1,254 74 1,328 696 56 52

Wealth 107 24 131 34 32 26

Global Banking & Markets 869 18 887 621 71 70

Global Transaction Services 53 — 53 43 81 81

Ulster Bank 1,196 1 1,197 491 41 41

US Retail & Commercial 424 — 424 298 70 70

Core 7,735 117 7,852 4,269 55 54

Non-Core 11,056 109 11,165 5,182 47 46

Group before RFS Holdings minority interest 18,791 226 19,017 9,451 50 50

RFS Holdings minority interest 2,470 — 2,470 1,565 63 63

21,261 226 21,487 11,016 52 51

2007

UK Retail 3,369 — 3,369 2,048 61 61

UK Corporate 1,187 16 1,203 737 62 61

Wealth 45 11 56 26 58 46

Global Banking & Markets 830 67 897 493 59 55

Global Transaction Services 73—73223030

Ulster Bank 442 1 443 314 71 71

US Retail & Commercial 229 — 229 220 96 96

Other ———30——

Core 6,175 95 6,270 3,890 63 62

Non-Core 2,076 36 2,112 1,082 52 51

Group before RFS Holdings minority interest 8,251 131 8,382 4,972 60 59

RFS Holdings minority interest 2,480 540 3,020 1,480 60 49

10,731 671 11,402 6,452 60 57

Key points

•Provision coverage fell during the year from 52% to 45% (REIL & PPL

coverage fell from 51% to 44%) as a consequence of the growth in

REIL being concentrated in secured, property-related loans. These

loans require relatively lower provisions in view of their collateralised

nature. With many of these being in Non-Core, the provision coverage

ratio is lower in Non-Core than in Core.

•Provision coverage in Core business improved from 55% to 57%.

•REIL in the Core businesses increased by £4.4 billion to £12.1 billion

while REIL in Non-Core more than doubled to £22.9 billion.

Credit risk continued

Risk elements and impairments

All the disclosures in this section (pages 142 to 148) are audited. The

Group classifies impaired assets as either risk elements in lending

(REIL) or potential problem loans (PPL). REIL represents non-accrual

loans, loans that are accruing but are past due 90 days and

restructured loans. PPL represents impaired assets which are not

included in REIL, but where information about possible credit problems

cause management to have serious doubts about the future ability of

the borrower to comply with loan repayment terms.

Both REIL and PPL are reported gross and take no account of the value

of any security held which could reduce the eventual loss should it

occur, nor of any provision marked. Therefore impaired assets which are

highly collateralised, such as mortgages, will have a low coverage ratio

of provisions held against the reported impaired balance.

The analyses of risk elements in lending and impairments as discussed

below, form a key part of the data provided to senior management on

the credit performance of the Group’s portfolios.