RBS 2009 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

Credit risk continued

Retail collections and recoveries continued

In the UK and Ireland, the Group has introduced new forbearance

policies for customers in financial difficulty based on various

government sponsored schemes, customer affordability and prospects.

In the US there has been an increase in agreed loan modification

programmes, including those sponsored by the US government.

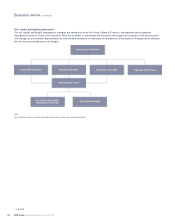

Credit risk framework

The approach taken to managing credit risk varies significantly between

wholesale portfolios (loans, and other products giving rise to credit risk,

to all but the smaller corporate customers, to financial institutions and to

government entities) and retail portfolios (secured and unsecured loans

and related products to individuals and small businesses).

Wholesale portfolios

Wholesale risk limits are aggregated at the counterparty level to

determine the level of credit approval required and to facilitate

consolidated credit risk management.

The credit approval process has two stages, assessment and decision.

Credit applications for corporate customers are prepared by

relationship managers in the units originating the credit exposures or by

the relationship management team with lead responsibility for a

counterparty where a customer has relationships with different divisions

and business units across the Group. This includes the assignment of

risk parameter estimates (probability of default, loss given default and

exposure at default) using approved models.

Credit approval authority is discharged by way of a framework of

individual delegated authorities that requires at least two individuals to

approve each credit decision, one from the business and one from the

credit risk management function. Both parties must hold sufficient

delegated authority under the Group-wide authority grid. The level of

authority granted to an individual is dependent on their experience and

expertise with only a small number of senior executives holding the

highest authority provided under the framework.

Daily monitoring of individual counterparty limits is undertaken. For

certain counterparties early warning indicators are also in place to

detect deteriorating trends of concern in limit utilisation or account

performance. A framework is also in place to monitor changes in credit

quality at the portfolio level.

As a minimum, credit relationships are reviewed and re-approved

annually. The renewal process addresses: borrower performance,

including reconfirmation or adjustment of risk parameter estimates; the

adequacy of security; and compliance with terms and conditions.

Retail portfolios

Retail business operations require a large volume of small scale credit

decisions, typically involving an application for a new product or a

change in facilities on an existing product. The majority of these

decisions are based upon automated strategies utilising best practice

credit and behaviour scoring techniques. Scores and strategies are

typically segmented by product, brand and other significant drivers of

credit risk. These data driven strategies utilise a wide range of credit

information relating to a customer including, where appropriate,

information across a customer’s holdings.

A small number of credit decisions are subject to additional manual

underwriting by authorised approvers in specialist units. These include

higher value more complex small business transactions and some

residential mortgage applications.

Divisional risk management committees focus on portfolio level decisions

which drive credit quality, changes to policy and strategy, and the setting of

credit scorecard cut-offs. The divisional risk management committees are

also responsible for reviewing ongoing performance of the business and, if

necessary, making or recommending adjustments to risk appetite.

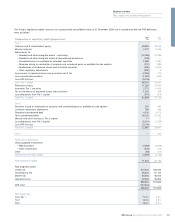

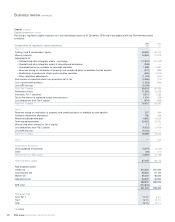

Credit risk measurement

Credit risk models are used throughout the Group to support the

quantitative risk assessment element of the credit approval process,

ongoing credit risk management, monitoring and reporting and portfolio

analytics. Credit risk models used by the Group may be divided into

three categories.

Probability of default/customer credit grade (PD)

These models assess the probability that a customer will fail to make full

and timely repayment of their obligations. The probability of a customer

failing to do so is measured over a one year period through the

economic cycle, although certain retail scorecards use longer periods

for business management purposes.

•Wholesale businesses: each counterparty is assigned an internal

credit grade which is in turn assigned to a default probability range.

There are a number of different credit grading models in use across

the Group, each of which considers risk characteristics particular to

that type of customer. The credit grading models score a

combination of quantitative inputs (for example, recent financial

performance) and qualitative inputs, (for example, management

performance or sector outlook). Scores are then mapped to grades

within each model. Grades are calibrated centrally to default

probabilities. Obligor grades can, under certain circumstances, be

cascaded to other borrowing entities within the obligor group where

there is sufficient dependence on the graded entity. The credit

grades for sovereign and central bank entities are assigned by a

specialist country risk analysis team using a sovereign grading

model. This team is independent of the origination function and is

comprised of economists. Certain grading models also cover

customers or transactions categorised as specialised lending (for

example certain types of investment property and asset finance

such as shipping).

•Retail businesses: each customer account is separately scored using

models based on the most material drivers of default. In general,

scorecards are statistically derived using customer data. Customers

are assigned a score which in turn, is mapped to a probability of

default. The probability of default is used within the credit approval

process and ongoing credit risk management, monitoring and

reporting. The probabilities of default are used to group customers

into risk pools. Pools are then assigned a weighted average

probability of default using regulatory default definitions.

RBS Group Annual Report and Accounts 2009128