RBS 2009 Annual Report Download - page 381

Download and view the complete annual report

Please find page 381 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

371 -

372

372 -

373

373 -

374

374 -

375

375 -

376

376 -

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390

|

|

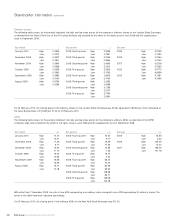

Shareholder information

379RBS Group Annual Report and Accounts 2009

Ordinary shares, preference shares, ordinary ADSs and

preference ADSs

Taxation of dividends

For the purposes of the Treaty, the Estate Tax Treaty and the US Internal

Revenue Code of 1986 as amended (the Code), US Holders of ordinary

ADSs and preference ADSs should be treated as owners of the ordinary

shares and the non-cumulative dollar preference shares underlying such

ADSs.

The US Treasury has expressed concerns that parties to whom

depositary receipts are released before shares are delivered to the

depositary, or intermediaries, in the chain of ownership between US

holders and the issuer of the security underlying the depositary receipts

may be taking actions that are inconsistent with the claiming of foreign

tax credits for US holders of depositary receipts. Such actions would

also be inconsistent with the claiming of the reduced rate of US tax

applicable to dividends received by certain non-corporate US holders.

Accordingly, the availability of the reduced tax rate for dividends

received by certain non-corporate US holders of ordinary ADSs could

be affected by actions taken by such parties or intermediaries.

The company is not required to withhold UK tax at source from dividend

payments it makes or from any amount (including any amounts in

respect of accrued dividends) distributed by the company. US Holders

who are not resident or ordinarily resident in the UK and who do not

carry on a trade, profession or vocation in the UK through a branch,

agency or permanent establishment in connection with which their

ordinary shares, non-cumulative preference shares, ordinary ADSs or

preference ADSs are held, used or acquired will not be subject to UK

tax in respect of any dividends received on the relevant shares or ADSs.

Distributions by the company (other than certain pro rata distributions of

ordinary shares or rights to receive such shares) will constitute foreign

source dividend income for US federal income tax purposes to the

extent paid out of the current or accumulated earnings and profits of

the company, as determined for US federal income tax purposes.

Because the company does not maintain calculations of its earnings

and profits under US federal income tax principles, it is expected that

distributions will be reported to US Holders as dividends. Payments will

not be eligible for the dividends-received deduction generally allowed to

corporate US holders.

Subject to applicable limitations that may vary depending upon a

holder’s individual circumstances, dividends paid to certain non-

corporate US Holders in taxable years beginning before 1 January 2011

will be taxable at a maximum tax rate of 15%. Non-corporate US

Holders should consult their own tax advisers to determine whether they

are subject to any special rules that limit their ability to be taxed at this

favourable rate.

Dividends will be included in a US Holder’s income on the date of the

US Holder’s (or in the case of ADSs, the depositary’s) receipt of the

dividend. The amount of any dividend paid in pounds sterling or euros

to be taken into income by a US Holder will be the US dollar amount

calculated by reference to the relevant exchange rate in effect on the

date of such receipt regardless of whether the payment is in fact

converted into US dollars. If the dividend is converted into US dollars on

the date of receipt, the US Holder generally should not be required to

recognise foreign currency gain or loss in respect of the dividend

income. If the amount of such dividend is not converted into US dollars

on the date of receipt, the US Holder may have foreign currency gain or

loss.

Taxation of capital gains

A US Holder that is not resident (or, in the case of an individual,

ordinarily resident) in the UK will not normally be liable for UK tax on

capital gains realised on the disposition of an ordinary share, a non-

cumulative dollar preference share, an ordinary ADS or a preference

ADS unless at the time of the disposal, in the case of a corporate US

Holder, such US Holder carries on a trade in the UK through a

permanent establishment or, in the case of any other US Holder, such

US Holder carries on a trade, profession or vocation in the UK through a

UK branch or agency and, in each case, such ordinary share, non-

cumulative dollar preference share, ordinary ADS or preference ADS is

or has been used, held or acquired by or for the purposes of such trade

(or profession or vocation), carried on through such permanent

establishment, branch or agency. Special rules apply to individuals who

are temporarily not resident or ordinarily resident in the UK.

A US Holder will, upon the sale or other disposition of an ordinary

share, a non-cumulative dollar preference share, an ordinary ADS or a

preference ADS, or upon the redemption of a non-cumulative dollar

preference share or preference ADS, generally recognise capital gain or

loss for US federal income tax purposes (assuming that in the case of a

redemption of a non-cumulative dollar preference share or a preference

ADS, such US Holder does not own, and is not deemed to own, any

ordinary shares or ordinary ADSs of the company) in an amount equal

to the difference between the amount realised (excluding in the case of

a redemption any amount treated as a dividend for US federal income

tax purposes, which will be taxed accordingly) and the US Holder’s tax

basis in such share or ADS. This capital gain or loss will be long-term

capital gain or loss if the US Holder held the share or ADS so sold,

disposed or redeemed for more than one year.

A US Holder who is liable for both UK and US tax on a gain recognised

on the disposal of an ordinary share, a non-cumulative dollar preference

share, an ordinary ADS or a preference ADS will generally be entitled,

subject to certain limitations, to credit the UK tax against its US federal

income tax liability in respect of such gain.