RBS 2009 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

RBS Group Annual Report and Accounts 2009

22

UK Retail

Brian Hartzer

Chief Executive,

UK Retail, Wealth

and Ulster Bank

MFor biographies

see pages 8-11

Our NatWest and RBS brands serve more

than 15 million retail customers, making us the

number two player in the UK banking market.

We offer a full range of products, including

current accounts, mortgages, credit/charge

cards and deposit accounts. We also help our

customers with their financial planning.

The recession made 2009 a very difficult year for our customers and

for UK Retail. Although the bottom-line figures are disappointing, we

continued to make the kind of progress that we need to return to good

health. In Branch Banking, customer deposits grew 11% on 2008,

reflecting the strength of our franchises. Customers opened an extra 2.2

million savings accounts – a 20% rise – and savings balances were up

by 11%. The number of current accounts increased by 3%. In Private

Banking & Advice, we also saw resilient returns, with performance for

mortgages and savings particularly good. Overall investment sales

increased by 3% on the previous year and our Independent Financial

Services business experienced a similar trend. Our Financial Planning

business also performed robustly, with a market share of 14%.

We appreciate the support that the UK taxpayer continued to give RBS

Group. In return, the Group agreed with the Government to support the

mortgage market by lending, subject to demand, £9 billion – net –

in the 12 months to the end of February 2010. The Group is on track to

exceed this target on net lending by £3 billion. One result of our

commitment to keep the mortgage market moving is that our share of

gross mortgage lending nearly doubled, from 7% in 2008 to 12% in 2009.

As compensation for the state aid we received, we also reached an

agreement with the European Commission to divest some businesses,

including the RBS branches in England and Wales, and the NatWest

branches in Scotland. A distinct management team is in place to

manage the transition carefully. Their job is to look after the day-to-day

needs of these branches and the support functions that back them up

so that customers continue to receive the right standard of service.

We have worked hard to address the challenges we face. In July 2009,

Brian Hartzer became Chief Executive of the UK Retail, Wealth and

Ulster Bank Division. Brian joined from Australia and New Zealand

Banking Group Ltd (ANZ) where he was Chief Executive Australia for

all ANZ business lines.

UK Retail offers a comprehensive range

of banking products and related financial

services to the personal market. It serves

customers through the RBS and NatWest

networks of branches and ATMs, and also

through telephone and internet channels.

2009 2008

£m £m

Net interest income 3,452 3,187

Non-interest income 1,495 1,751

Total income 4,947 4,938

Expenses (3,039) (3,196)

Operating profit before impairment losses 1,908 1,742

Impairment losses (1,679) (1,019)

Operating profit 229 723

Risk-weighted assets (£bn) 51.3 45.7

Return on equity 4.2% 13.1%

Net interest margin 3.59% 3.58%

Cost:income ratio 59.8% 62.4%

Loan:deposit ratio (excluding repos) 115% 116%

11%

increase in customer deposits in the year

10%

increase in mortgage customers in the year

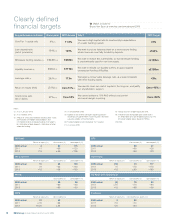

Target Return on equity (%) Cost:income (%) Loan:deposit (%)

2011 >1 <60 <120

2013 >15 c.50 <105