RBS 2009 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009162

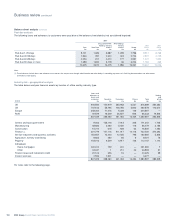

Market risk continued

Assets and liabilities in the trading book are measured at their fair value.

Fair value is the amount at which the instrument could be exchanged in

a current transaction between willing parties. The fair values are

determined following IAS 39 guidance, which requires banks to use

quoted market prices or valuation techniques (models) that make the

maximum use of observable inputs. When marking to market using a

model, the valuation methodologies are reviewed and approved by the

market risk function. Group Risk provides an independent evaluation of

the model for transactions deemed by the Group Model Product Review

Committee (GMPRC) to be large, complex and/or innovative. Any profits

or losses on the revaluation of positions are recognised in the daily

profit and loss.

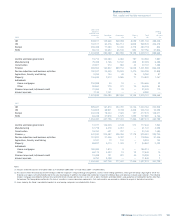

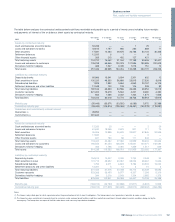

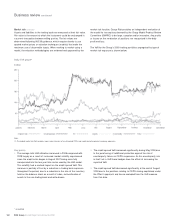

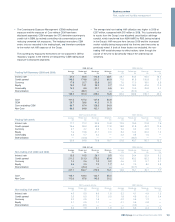

The VaR for the Group’s 2009 trading portfolios segregated by type of

market risk exposure is shown below.

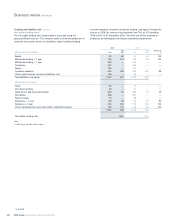

Daily VaR graph*

Key points

•The average total VaR utilisation increased in 2009 compared with

2008 largely as a result of increased market volatility experienced

since the credit crisis began in August 2007 being more fully

incorporated into the two year time series used by the VaR model.

This volatility had a marked impact on the credit spread VaR. This

increase is partially off-set by a reduction in trading book exposure

throughout the period, due to a reduction in the size of the inventory

held on the balance sheet as a result of sales, reclassification of

assets to the non-trading book and write-downs.

•The credit spread VaR increased significantly during May 2009 due

to the purchasing of additional protection against the risk of

counterparty failure on CDPCs exposures. As this counterparty risk

is itself not in VaR these hedges have the effect of increasing the

reported VaR.

•The credit spread VaR decreased significantly at the end of August

2009 due to the positions relating to CDPCs being capitalised under

the Pillar II approach and hence excluded from the VaR measure

from that date.

* unaudited

Note:

(1) The traded market risk VaR excludes super senior tranches of asset backed CDOs and credit derivative product company exposures.