RBS 2009 Annual Report Download - page 203

Download and view the complete annual report

Please find page 203 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

Risk, capital and liquidity management

201RBS Group Annual Report and Accounts 2009

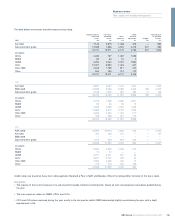

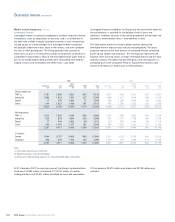

The table below analyses the movements in leveraged finance exposures for the year.

Drawn Undrawn Total

£m £m £m

Balance at 1 January 2009 12,619 3,150 15,769

Transfers in (from credit trading business) 563 41 604

Sales (247) (144) (391)

Repayments and facility reductions (934) (392) (1,326)

Funded deals 166 (166) —

Lapsed/collapsed deals — (19) (19)

Changes in fair value (31) — (31)

Accretion of interest 100 — 100

Impairment provisions (1,041) — (1,041)

Exchange and other movements (655) (190) (845)

Balance at 31 December 2009 10,540 2,280 12,820

Key points

•Since the beginning of the credit market dislocation in the second half of 2007, investor appetite for leveraged loans and similar risky assets has

fallen dramatically, with higher perceived risk of default due to the leverage involved. Furthermore, secondary prices of leveraged loans traded fell

due to selling pressure and margins increasing, as well as reduced activity in the primary market.

•During 2009 the Group’s sterling exposure has declined, largely as a result of the weakening of the US dollar and euro against sterling during the

period.

•There have also been a number of credit impairments and write-offs during 2009, including some names which the Group previously held as part

of its syndicate portfolio.

•Early repayments as a result of re-financings have further reduced the exposure.

Not included in the table above are:

•UK Corporate leveraged finance net exposures of £7.1 billion at 31 December 2009 (2008 – £6.9 billion) related to debt and banking facilities

provided to UK mid-corporates. Of this, £1.4 billion related to facilities provided to client in the retail sector and £2.1 billion to the industrial sector

(2008 – £1.4 billion and £2.5 billion respectively).

•Ulster Bank leveraged finance net exposures of £0.6 billion at 31 December 2009 (2008 – £0.7 billion).

Special purpose entities (SPEs)

The Group arranges securitisations to facilitate client transactions and

undertakes securitisations to sell financial assets or to fund specific

portfolios of assets. The Group also acts as an underwriter and depositor

in securitisation transactions involving both client and proprietary

transactions. In a securitisation, assets, or interests in a pool of assets,

are transferred generally to a special purpose entity (SPE) which then

issues liabilities to third party investors. SPEs are vehicles established for

a specific, limited purpose, usually do not carry out a business or trade

and typically have no employees. They take a variety of legal forms –

trusts, partnerships and companies – and fulfil many different functions.

As well as being a key element of securitisations, SPEs are also used in

fund management activities to segregate custodial duties from the fund

management advice provided by the Group.

It is primarily the extent of risks and rewards assumed that determines

whether these entities are consolidated in the Group’s financial

statements. The following section aims to address the significant

exposures which arise from the Group’s activities through specific types

of SPEs.

The Group sponsors and arranges own-asset securitisations, whereby

the sale of assets or interests in a pool of assets into an SPE is financed

by the issuance of securities to investors. The pool of assets held by the

SPE may be originated by the Group, or (in the case of whole loan

programmes) purchased from third parties, and may be of varying

credit quality. Investors in the debt securities issued by the SPE are

rewarded through credit-linked returns, according to the credit rating of

their securities. The majority of securitisations are supported through

liquidity facilities, other credit enhancements and derivative hedges

extended by financial institutions, some of which offer protection against

initial defaults in the pool of assets. Thereafter, losses are absorbed by

investors in the lowest ranking notes in the priority of payments.

Investors in the most senior ranking debt securities are typically

shielded from loss, since any subsequent losses may trigger repayment

of their initial principal.