RBS 2009 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

RBS Group Annual Report and Accounts 2009

24

UK Corporate

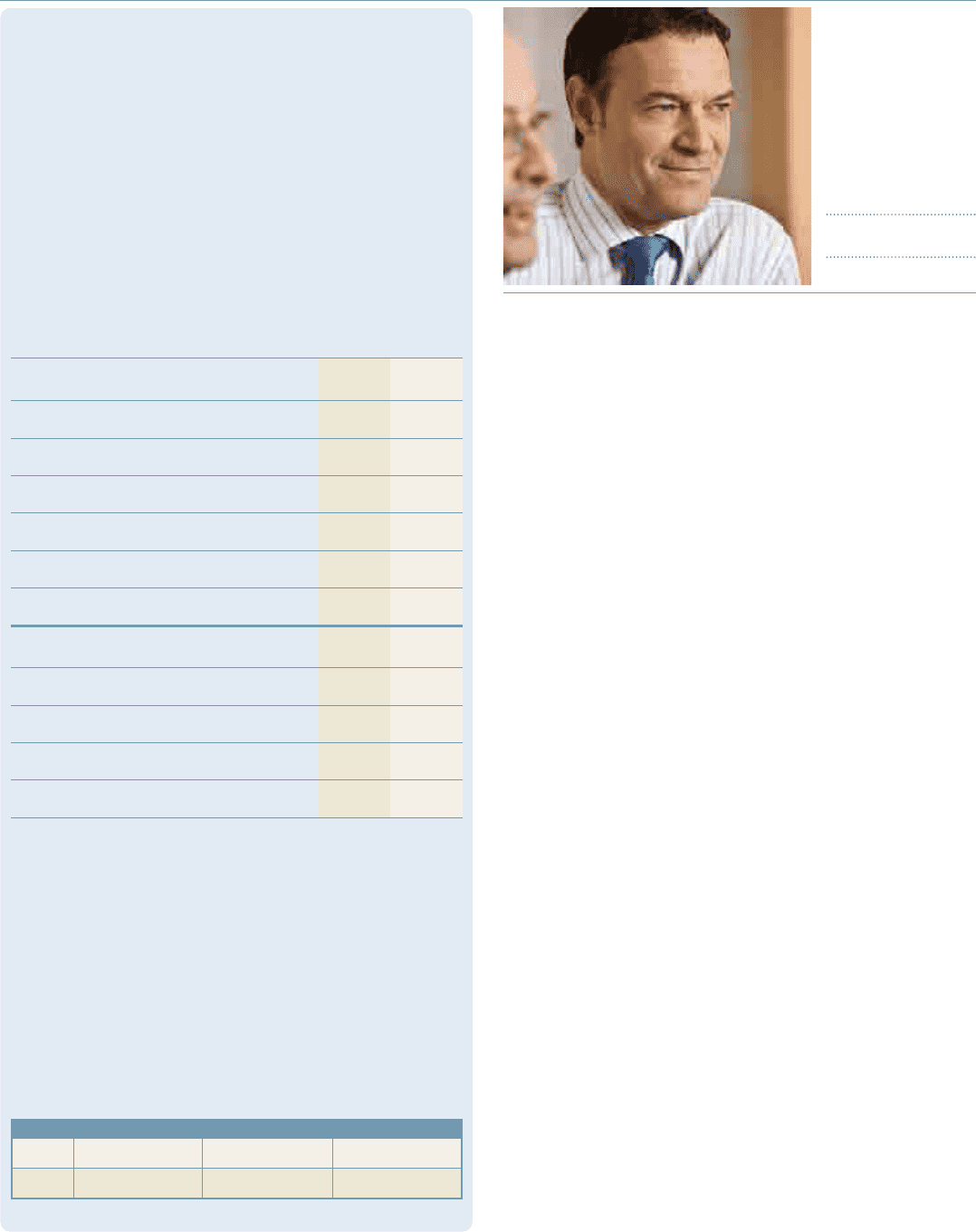

Chris Sullivan,

Chief Executive,

UK Corporate

MFor biographies

see pages 8-11

Shortly after he became Chief Executive of

our Corporate Banking Division in August 2009,

Chris Sullivan told a gathering of colleagues,

“The thing we are here to do is to support

business customers to run successful

businesses.”

The recession and the need to rebuild our own business could have

distracted us from that task. But it didn’t. Instead, we knew that as more

start–ups choose RBS over any other bank we had a responsibility to

support our customers in difficult times – and that is exactly what we did.

In October, we launched the Business Hotline. Staffed by a team of

experienced business bankers, from 8am to 8pm five days a week,

Business Hotline offers small and medium-sized enterprises (SMEs) free

advice and a second opinion in cases where their lending application

has been turned down. Business Hotline is open to all SMEs, not just

RBS or NatWest customers.

At its busiest times, Business Hotline has taken over 100 calls a day.

Although we believe that RBS and NatWest get it right most of the time,

we have changed a number of our decisions not to lend as a result of

calls to Business Hotline and we’ve also been able to lend to companies

who contacted us having been turned down by other banks.

In November, we published our first ever SME Customer Charter. It tells

businesses what they can expect from us and how we will behave. It

reaffirmed our Committed Overdraft Promise, extending it to the end of

2010. That means customers’ committed facilities will remain in place for

at least 12 months. We also promised not to increase overdraft pricing

unless there is a material increase in the risk associated with lending.

Where the risks fall, we will reduce SMEs’ prices.

We offer our customers a combination of a committed overdraft and a

price promise. As a result, nine out of 10 small business customers have

had their overdraft facilities renewed at the same or a lower margin.

We offer two years’ free banking to start-ups and opened more than

100,000 start-up accounts in the nine months to September 2009.

UK Corporate is a leading provider of

banking, finance, and risk management

services to the corporate and SME sector

in the United Kingdom. It offers a full range

of banking products and related financial

services through a nationwide network of

relationship managers, and also through

telephone and internet channels. The product

range includes asset finance through the

Lombard brand.

2009 2008

£m £m

Net interest income 2,292 2,448

Non-interest income 1,290 1,289

Total income 3,582 3,737

Expenses (1,530) (1,637)

Operating profit before impairment losses 2,052 2,100

Impairment losses (927) (319)

Operating profit 1,125 1,781

Risk-weighted assets (£bn) 90.2 85.7

Return on equity 10.3% 18.0%

Net interest margin 2.22% 2.40%

Cost:income ratio 42.7% 43.8%

Loan:deposit ratio 126% 142%

100,000

start-up accounts in the nine months to September

7%

reduction in costs in the year

Target Return on equity (%) Cost:income (%) Loan:deposit (%)

2011 >5 <45 <135

2013 >15 <35 <130