RBS 2009 Annual Report Download - page 204

Download and view the complete annual report

Please find page 204 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009202

Market turmoil exposures continued

Special purpose entities continued

The Group also employs synthetic structures, where assets are not sold

to the SPE, but credit derivatives are used to transfer the credit risk of

the assets to an SPE. Securities may then be issued by the SPE to

investors, on the back of the credit protection sold to the Group by the

SPE.

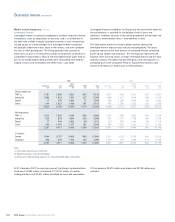

Residential and commercial mortgages and credit card receivables

form the types of assets generally included in cash securitisations, while

corporate loans and commercial mortgages typically serve as reference

obligations in synthetic securitisations.

The Group sponsors own-asset securitisations as a way of diversifying

funding sources, managing specific risk concentrations, and achieving

capital efficiency. The Group purchases the securities issued in own-

asset securitisations. During 2008, the Group was able to pledge AAA-

rated asset-backed securities as collateral for repurchase agreements

with major central banks under schemes such as the Bank of England’s

Special Liquidity Scheme, launched in April 2008, which allowed banks

to temporarily swap high-quality mortgage-backed and other securities

for liquid UK treasury bills. This practice has contributed to the Group’s

sources of funding during 2008 and 2009 in the face of the contraction

in the UK market for inter-bank lending and the investor base for

securitisations.

The Group typically does not retain the majority of risks and rewards of

own-asset securitisations set up for the purposes of risk diversification

and capital efficiency, where the majority of investors tend to be third

parties. Therefore, the Group typically does not consolidate the related

SPEs.

The Group has also established whole loan securitisation programmes

in the US and UK where assets originated by third parties are

warehoused by the Group for securitisation. The majority of these

vehicles are not consolidated by the Group, as it is not exposed to the

risks and rewards of ownership.

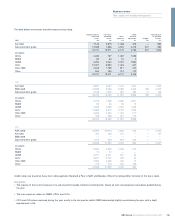

The table below sets out the asset categories together with the carrying

amount of the assets and associated liabilities for those securitisations

and other asset transfers, other than conduits (discussed below), where

the assets continue to be recorded on the Group’s balance sheet.

Conduits

The Group sponsors and administers a number of asset-backed

commercial paper (ABCP) conduits. A conduit is an SPE that issues

commercial paper and uses the proceeds to purchase or fund a pool of

assets. The commercial paper is secured on the assets and is

redeemed either by further commercial paper issuance, repayment of

assets or funding from liquidity facilities. Commercial paper is typically

short-dated, usually up to three months.

Group-sponsored conduits can be divided into multi-seller conduits and

own-asset conduits. The Group consolidates both types of conduit

where the substance of the relationship between the Group and the

conduit vehicle is such that the vehicle is controlled by the Group. The

total assets held by Group-sponsored conduits were £27.4 billion at 31

December 2009 (2008 – £49.9 billion). Liquidity commitments from the

Group to the conduit exceed the nominal amount of assets funded by

the conduit as liquidity commitments are sized to cover the funding cost

of the related assets.

Group-sponsored multi-seller conduits

The multi-seller conduits were established by the Group for the purpose

of providing its clients with access to diversified and flexible funding

sources. A multi-seller conduit typically purchases or funds assets

originated by the banks’ clients. The multi-seller conduits account for

43% of the total liquidity and credit enhancements committed by the

Group at 31 December 2009 (2008 – 69.4%).

The Group sponsors six multi-seller conduits which finance assets from

Europe, North America and Asia-Pacific. Assets purchased or financed

by the multi-seller conduits include auto loans, residential mortgages,

credit card receivables, consumer loans and trade receivables.

2009 2008 2007

Assets Liabilities Assets Liabilities Assets Liabilities

£m £m £m £m £m £m

Residential mortgages 69,927 15,937 55,714* 20,075 23,652 23,436

Credit card receivables 2,975 1,592 3,004 3,197 2,948 2,664

Other loans 36,448 1,010 1,679 1,071 1,703 1,149

Finance lease receivables 597 597 1,077 857 1,038 823

* revised

Key points

•The increase in both residential mortgages and other loan assets in the year principally relates to assets securitised to facilitate access to central

bank liquidity schemes.

•As all notes issued by own-asset securitisation SPEs are purchased by Group companies, assets are significantly greater than securitised liabilities.