RBS 2009 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

Risk, capital and liquidity management

135RBS Group Annual Report and Accounts 2009

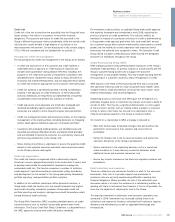

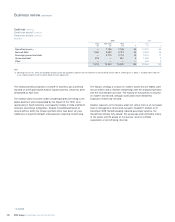

UK residential mortgages

The UK mortgage portfolio totalled £85.5 billion at 31 December 2009,

an increase of 15% from 31 December 2008, due to strong sales

growth and lower redemption rates. Of the total portfolio, 98% is

designated as Core business with the primary brands being the Royal

Bank of Scotland, NatWest, the One Account and First Active. The

assets comprise prime mortgage lending and include 6.6% (£5.6 billion)

of exposure to residential buy-to-let. There is a small legacy self

certification book (0.4% of total assets); which was withdrawn from sale

in 2004.

UK net new mortgage lending in 2009 was strong at £11 billion and the

Group has exceeded its commitment to the UK Government on net

mortgage lending. The average LTV for new business during 2009 was

unchanged at 67.2%. The maximum LTV available to new customers

remains at 90%.

The arrears rate (three or more payments missed) on the combined

Royal Bank of Scotland and NatWest brands was 1.8% at 31 December

2009. After a period of deterioration driven by the economic environment

this stabilised in the second half of 2009 (arrears rate stood at 1.8% at

30 June 2009 and 1.5% at 31 December 2008). The arrears rate on the

buy-to-let portfolio was 1.6% at 31 December 2009 (1.6% at 30 June

2009 and 1.5% at 31 December 2008).

The mortgage impairment charge was £129 million in 2009, compared

with £33 million in 2008, attributable to declining house prices driving

lower recoveries and an increase in defaults reflecting the difficult

economic environment. Default rates remain sensitive to economic

developments, notably unemployment rates. Provision as a proportion

of balances at 31 December 2009 were 0.3% and 0.2% at 31

December 2008.

A number of initiatives aimed at increasing the levels of support to

customers experiencing difficulties were implemented in 2008 and will

continue in 2010. The Group does not initiate repossession proceedings

for at least six months after arrears are evident and participates in

various government-led initiatives such as the mortgage rescue scheme

and homeowner mortgage support.

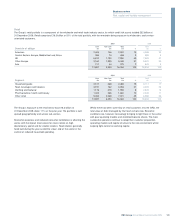

Ulster Bank residential mortgages

The residential mortgage portfolio across the Ulster Bank and First Active

brands totalled £22.3 billion at 31 December 2009; 91% is in the Republic

of Ireland and 9% in Northern Ireland. This represents a decline of 4% in

the Republic of Ireland and an increase of 13% in Northern Ireland from

31 December 2008. 27% of the portfolio is Non-Core.

The arrears rate increased to 3.3% at 31 December 2009 from 1.6% at 31

December 2008. As a result, the impairment charge for 2009 was £115

million versus £23 million for 2008. Repossessions totalled 96 in 2009,

compared with 37 in 2008 with the majority of these being voluntary.

During 2009 new business originations in the Republic of Ireland were

very low across all segments. The bank introduced new products –

Momentum and SecureStep – in both Northern Ireland and the Republic

of Ireland which aim to support market activity for new build properties.

In Northern Ireland, lending increased in the second half of 2009 as a

degree of confidence returned to the property market.

Citizens real estate

Citizens total residential real estate portfolio totalled $42 billion at 31

December 2009 (2008 – $50 billion). The real estate portfolio comprises

$11 billion of first lien mortgages and $31 billion of home equity loans

and lines (Core portfolio 48% first lien). 83% of the portfolio is Core

business; $10 billion of mortgages and $25 billion of home equity loans

and lines (48% of the latter being first lien). The serviced by others

(SBO) portfolio (96% second lien) is the largest component of the Non-

Core portfolio.

Citizens has focused its origination efforts in the more mature and stable

markets of New England and Mid Atlantic (Citizen’s ‘footprint states’),

targeting low risk products and adopting conservative risk policies.

Loan acceptance criteria were tightened during 2009 to address

deteriorating economic and market conditions. At 31 December 2009,

the portfolio consisted of $34 billion (80% of the total portfolio) in these

footprint states.

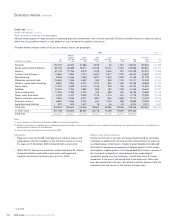

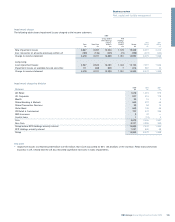

The table below details residential mortgages three months or more in arrears (by volume).

2009 2008

%%

UK Retail (1) 1.8 1.5

Ulster Bank 3.3 1.6

Citizens 1.5 0.9

Note:

(1) UK Retail analysis covers the Royal Bank and NatWest brands and covers 77% of the UK Retail mortgage portfolio (the remainder operates under the same credit policies).