RBS 2009 Annual Report Download - page 156

Download and view the complete annual report

Please find page 156 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009154

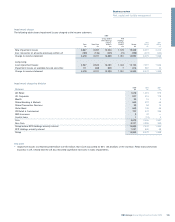

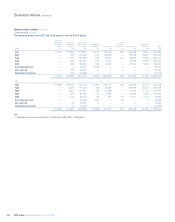

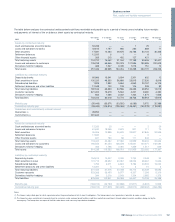

Funding and liquidity risk

All the disclosures in this section (pages 154 to 160) are audited unless

indicated otherwise with an asterisk (*).

The Group’s liquidity policy is designed to ensure that the Group can at

all times meet its obligations as they fall due.

Liquidity management within the Group addresses the overall balance

sheet structure and the control, within prudent limits, of risk arising from

the mismatch of maturities across the balance sheet and from exposure

to undrawn commitments and other contingent obligations.

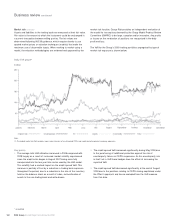

Following a difficult first quarter of 2009, most indicators of stress in

financial markets are close to or better than in late 2008. Liquidity

conditions in money and debt markets have improved significantly since

the beginning of the second quarter of 2009. Contributing to the

improvement has been a combination of ongoing central bank and

other official liquidity support schemes, guarantee schemes and rate

cuts. Signs of underlying macroeconomic trends such as stabilisation of

the UK economy, also helped to sustain a recovery in debt markets.

Liquidity risk framework and governance

The Group has an approved risk appetite supported by explicit targets

and metrics to control the size and extent of both short-term and long-

term liquidity risk. These metrics are reviewed by the Board and Group

Asset and Liability Management Committee (GALCO) on a regular basis.

The Group uses stress tests to refine and update the risk appetite in

light of changing conditions.

The GALCO, chaired by the Group Finance Director, has the

responsibility to set Group policy and ensure that it is cascaded and

communicated to the business divisions. Group Treasury is the

functional area with responsibility for monitoring and control of the

Group's funding and liquidity positions.

Group Treasury is supported by a governance process that includes a

Liquidity Risk Forum comprising functional areas across the organisation

that are responsible for liquidity management, including monitoring

through divisional and regional asset and liability committees.

The Group uses funds transfer pricing to ensure the costs of liquidity as

well as funding are integrated into the business decision making

process.

The Group continues to improve and augment funding and liquidity risk

management practices in light of experience of the market over the last

two years and of emerging regulatory and industry standards such as

the FSA policy statement on strengthening liquidity standards.

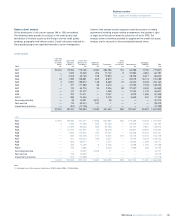

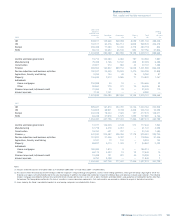

Structural management

The Group regularly evaluates its structural liquidity risk and applies a

variety of balance sheet management and term funding strategies to

maintain this risk within its policy parameters. The degree of maturity

mismatch within the overall long-term structure of the Group’s assets

and liabilities is managed within internal policy guidelines, aimed at

ensuring term asset commitments are funded on an economic basis

over their life. In managing its overall term structure, the Group analyses

and takes into account the effect of retail and corporate customer

behaviour on actual asset and liability maturities where they differ

materially from the underlying contractual maturities.

The Group targets diversification in its funding sources to reduce

funding risk. A key source of funds for the Group is its core customer

deposits gathered by its retail banking, private client, corporate and

small and medium enterprises franchises. The Group’s multi-brand

offering and strong client focus is a key part of the funding strategy and

continues to benefit the Group’s funding position.

The Group also accesses the wholesale funding market to provide

additional flexibility in funding sources. The Group has actively sought to

manage its liquidity position through increasing the duration of short-

term wholesale funding, continued diversification of wholesale debt

investors and depositors, supplemented by long-term issuance,

government guaranteed debt, and a programme of ensuring that assets

held are eligible as collateral to access central bank liquidity schemes.

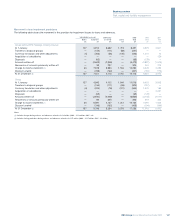

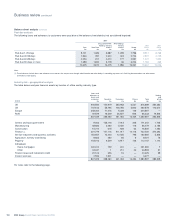

Cash flow management

The short-term maturity structure of the Group’s assets and liabilities is

managed daily to ensure that all material or potential cash flows, undrawn

commitments and other contingent obligations can be met. The primary

focus of the daily management activity is to ensure access to sufficient

liquidity to meet cash flow obligations within key time horizons, including

out to one month ahead and FSA target horizons such as 90 days.

Potential sources of liquidity include cash inflows from maturing assets,

new borrowings or the sale of various debt securities held. Short-term

liquidity risk is generally managed on a consolidated basis with liquidity

mismatch limits in place for subsidiaries and non-UK branches which

have material local treasury activities, thereby assuring that the daily

maintenance of the Group’s overall liquidity risk position is not

compromised.

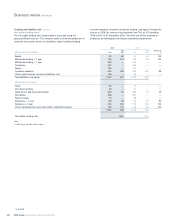

Volume management

The Group also actively monitors and manages future business volumes

to assess funding and liquidity requirements and ensure that the Group

operates within the risk appetite and metrics set by the Board. This

includes management of undrawn commitments, conduits and liquidity

facilities within acceptable levels.

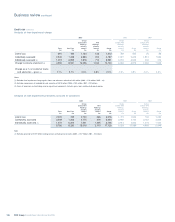

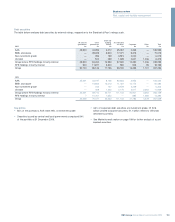

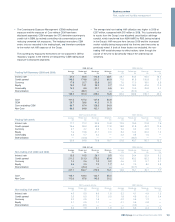

Liquidity reserves

The Group has built up a diversified stock of highly marketable liquid

assets including highly rated central government debt that can be used

as a buffer against unforeseen impacts on cash flow or in stressed

environments. The make up of this portfolio of assets is sub-divided into

tiers on the basis of asset liquidity, with haircuts applied to ensure that

realistic liquidation values are used in key metrics. This portfolio

includes a centrally held buffer against severe liquidity stresses and

locally held buffers to meet self sufficiency needs.