RBS 2009 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

RBS Group Annual Report and Accounts 200918

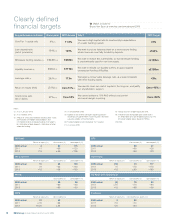

Clearly defined

financial targets dWatch or listen to

Bruce Van Saun at www.rbs.com/annualreport2009

Why?

We need a high capital ratio to meet society’s expectations

of a safer banking system.

We want to put our balance sheet on a more secure footing,

where loans are near fully funded by deposits.

We want to reduce this vulnerability, so that wholesale funding

is predominantly used for non-loan assets.

We want to rebuild our liquidity buffers, to guard against

unexpected funding difficulties.

We target a conservative leverage ratio, at a level consistent

with other leading banks.

We need to cover our cost of capital in the long-run, and justify

our shareholders’ support.

We cannot achieve a 15% RoE without cost control

and asset margin re-pricing.

2013 Target

>8%

c100%

<£150bn

c£150bn

<20x

Core >15% (9)

Core <50%

UK Retail

Return on equity (%) Cost:income (%) Loan:deposit (%)

2009 actual 4 60 115

2011 >1 <60 <120

2013 >15 c.50 <105

UK Corporate

Return on equity (%) Cost:income (%) Loan:deposit (%)

2009 actual 10 43 126

2011 >5 <45 <135

2013 >15 <35 <130

Wealth

Cost:income (%) Loan:deposit (%)

2009 actual 59 38

2011 <60 <35

2013 <50 <30

GBM

Return on equity (%) Cost: income (%)

2009 actual 31 42

2011 c.15 <65

2013 15-20 c.55

GTS

Cost:income (%) Loan:deposit (%)

2009 actual 59 21

2011 <60 <25

2013 <50 <20

Ulster Bank

Return on equity (%) Cost:income (%) Loan:deposit (%)

2009 actual (13) 73 177

2011 >0 <75 <175

2013 >15 c.50 <150

US Retail and Commercial

Return on equity (%) Cost:income (%) Loan:deposit (%)

2009 actual (2) 78 80

2011 c.10 <70 <90

2013 >15 <55 <90

Insurance

Return on equity (%) Cost:income less claims (%)

2009 actual 2 92

2011 >15 <70

2013 >20 <60

Worst point

4% (1)

154% (2)

£343bn (4)

£90bn (4)

28.7x (7)

(31%) (8)

97% (10)

Key performance indicator

Core Tier 1 capital ratio

Loan:deposit ratio

(net of provisions)

Wholesale funding reliance (3)

Liquidity reserves (5)

Leverage ratio (6)

Return on equity (RoE)

Cost:income ratio

net of claims

2009 Actuals

11.0%

135%

£250bn

£171bn

17.0x

Core 13% (9)

Core 53%

Notes:

(1) As at 1 January 2008.

(2) As at October 2008.

(3) Amount of unsecured wholesale funding under 1 year.

2009 includes £109 billion of bank deposits and

£141 billion of other wholesale funding. 2013 target is

for <£65 billion of bank deposits, <£85 billion of other

wholesale funding.

(4) As at December 2008.

(5) Eligible assets held for contingent liquidity purposes

including cash, government issued securities and other

securities eligible with central banks.

(6) Funded tangible assets divided by Tier 1 capital.

(7) As at June 2008.

(8) Group return on tangible equity for 2008.

(9) Indicative Core attributable profit taxed at 28%

on attributable core spot tangible equity (circa 70%

of Group tangible equity based on RWAs).

(10) 2008.