RBS 2009 Annual Report Download - page 171

Download and view the complete annual report

Please find page 171 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

Risk, capital and liquidity management

169RBS Group Annual Report and Accounts 2009

Insurance risk*

All the disclosures in this section are unaudited and indicated with an

asterisk (*). The Group is exposed to insurance risk directly through its

general insurance and life insurance businesses.

Insurance risk arises through fluctuations in the timing, frequency and/or

severity of insured events, relative to the expectations at the time of

underwriting. Insurance risk is managed in four distinct ways:

•Underwriting and pricing risk management: is managed through the

use of underwriting guidelines which detail the class, nature and

type of business that may be accepted, pricing policies by product

line and brand and centralised control of wordings and any

subsequent changes;

•Claims risk management: is handled using a range of automated

controls and manual processes;

•Reserving risk management: is applied to ensure that sufficient funds

have been retained to handle and pay claims as the amounts fall

due, both in relation to those claims which have already occurred or

will occur in future periods of insurance. Reserving risk is managed

through detailed analysis of historical and industry claims data and

robust control procedures around reserving models; and

•Reinsurance risk management: is used to protect against adverse

claims experience on business which exceeds internal risk appetite.

The Group uses various types of reinsurance to transfer risk that is

outside the Group’s risk appetite, including individual risk excess of

loss reinsurance, catastrophe excess of loss reinsurance and quota

share reinsurance.

Overall, insurance risk is predictable over time, given the large volumes

of data. However, uncertainty does exist, especially around predictions

such as the variations in weather for example. Risk is minimised through

the application of documented insurance risk policies, coupled with risk

governance frameworks and the purchase of reinsurance.

General insurance business

RBS Insurance underwrites retail and SME insurance with a focus on

high volume, relatively straightforward products. The key insurance risks

are as follows:

•Motor insurance contracts (private and commercial): claims

experience varies due to a range of factors, including age, gender

and driving experience together with the type of vehicle and location;

•Property insurance contracts (residential and commercial): the major

causes of claims for property insurance are weather (flood, storm),

theft, fire, subsidence and various types of accidental damage; and

•Other commercial insurance contracts: risk arises from business

interruption and loss arising from the negligence of the insured

(liability insurance).

Most general insurance contracts are written on an annual basis, which

means that the Group’s liability extends for a twelve month period, after

which the Group is entitled to decline to renew the policy or can impose

renewal terms by amending the premium, terms and conditions.

An analysis of gross and net insurance claims can be found in the

financial statements (see page 310).

Life assurance business

The Group’s three regulated life companies, National Westminster Life

Assurance Limited, Royal Scottish Assurance plc and Direct Line Life

Insurance Company Limited underwrite life insurance products within

the UK retail insurance market. The key assurance risks are as follows:

•Term assurance contracts: mortality claims experience varies due to

a range of factors, including age, gender and smoker status. The key

factors that increase the level of claims are disease pandemics and

adverse lifestyle changes; and

•Critical illness insurance contracts: morbidity claims experience

varies due to a range of factors, including age, gender and past

medical history. The key factors that can increase the level of claims

are adverse lifestyle changes and improvements in medical

diagnosis methods.

These are long-term contracts with long-term business provisions that

are calculated in accordance with the UK accounting standard FRS 27

‘Life Assurance’.

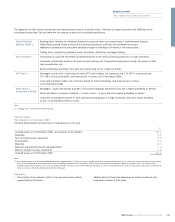

Estimations (assumptions) including future mortality, morbidity,

persistency and levels of expenses are made in calculating reserves.

The Group uses standard mortality and morbidity tables appropriate to

the type of contract being written. These are adjusted as appropriate to

reflect historical experience and future expectations. Sample mortality

rates, expressed as deaths per million per annum, for term assurance

products (age 40) are:

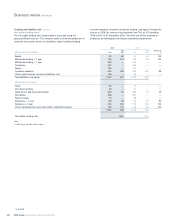

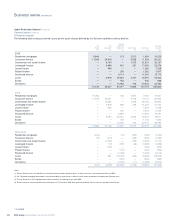

2009 2008

Mortality (per million) per annum per annum

Male non-smoker 674 723

Male smoker 1,542 1,590

Female non-smoker 497 568

Female smoker 1,136 1,277

* unaudited