RBS 2009 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

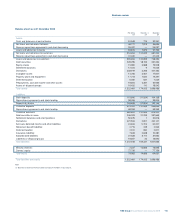

Risk, capital and liquidity management

The Group has seen a continuation of challenging financial market and

economic conditions during 2009. Although some signs of improvement

have started to emerge, the performance of key economies remains

uncertain and the Group has continued to experience material

impairment losses and credit market write-downs, including further

write-downs in respect of monoline exposures. The majority of these are

in the Non-Core division, which in time will be run down, significantly

reducing the size of the Group’s balance sheet and associated capital

requirements.

In April 2009, £5 billion of preference shares were redeemed and

replaced by ordinary shares using the proceeds of the Second Placing

and Open Offer. This strengthened the Group’s Core Tier 1 capital,

enhancing its financial stability during a tough economic and market

period.

As an interim measure pending full compliance with Basel 2, the Group,

with the agreement of the regulators, consolidates the RWAs of ABN

AMRO on the basis of Basel 1 plus an adjustment factor. The Group is

advanced in its preparation for moving to a Basel 2 compliant approach

for the ABN AMRO businesses it will retain. As part of this transition the

Group has agreed with the FSA to increase the adjustment factor with

effect from 31 December 2009 to reflect changing circumstances. This

change has increased RWAs by approximately £8 billion thereby

reducing the Core Tier 1 ratio at 31 December 2009 by 20 basis points.

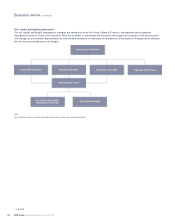

Asset Protection Scheme

On 22 December 2009, the Group acceded to the Asset Protection

Scheme (‘APS’ or ‘the Scheme’). The key commercial terms and details

of the assets covered by the Scheme are set out on page 174.

Following the accession to the APS, HM Treasury provides loss

protection against potential losses arising in a pool of assets. HM

Treasury also subscribed to £25.5 billion of capital in the form of B

shares and a Dividend Access Share with a further £8 billion of capital

in the form of B shares, potentially available as contingent capital. The

Group pays annual fees in respect of the protection and contingent

capital. The Group has the option, subject to HM Treasury consent, to

pay the annual premium, contingent capital and the exit fee payable in

connection with any termination of the Group’s participation in the APS

in whole or in part, by waiving the entitlements of members of the

Group to certain UK tax reliefs.

Following accession to the APS, arrangements were put in place within

the Group that extended effective APS protection to all other regulated

entities holding assets covered by the APS.

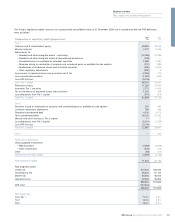

On 19 January 2009, the FSA announced that it expects each bank

participating in the UK Government’s recapitalisation scheme to have a

minimum Core Tier 1 ratio of 4% on a stressed basis. As at 31

December 2009 the Group’s Core Tier 1 ratio was 11.0% (2008 – 6.6%).

While the RWA relief from the APS enabled the Group to maintain robust

capital ratios, it is clear that the next few years pose continuing

challenges in respect of impairment levels, trading performance and the

return to profitability, RWA volatility including procyclical effects, and

increasing regulatory demands.

The Group’s policy will be to continue to maintain a strong capital base,

to develop this base as appropriate and to utilise it efficiently throughout

the Group’s activities in order to optimise shareholder returns while

maintaining a prudent relationship between the capital base and the

underlying risks of the business.

The subscription for £25.5 billion of B shares improved the Group’s Core

Tier 1 capital ratio by 580 basis points at 31 December 2009.

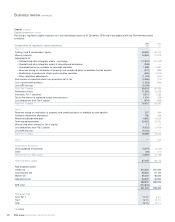

Regulatory capital impact of the APS

Methodology

The regulatory capital requirements for assets covered by the Scheme

are calculated using the securitisation framework under the FSA

prudential rules. The calculation is as follows (known as ‘the Uncapped

Amount’):

•First Loss – the residual first loss, after impairments and writedowns,

to date, is deducted from the available capital – split equally between

Core Tier 1 and Tier 2 capital;

•HM Treasury share of covered losses – after the first loss piece has

been deducted, the 90% of assets covered by HM Treasury are risk

weighted at 0%; and

•RBS share of covered losses – the remaining 10% share of loss is

borne by RBS and is risk weighted in the normal way.

Should the Uncapped Amount be higher than those of the underlying

assets (ignoring the Scheme), the capital requirements for the Scheme

are capped at the level of the requirements for the underlying assets

(‘Capped Amount’). Where capped, the Group apportions the Capped

Amount up to the level of the First Loss as calculated above; any

unused Capped Amount after the First Loss capital deduction will be

taken as RWAs for the Group’s share of covered losses.

Adjustments to the regulatory capital calculation can be made for either

currency or maturity mismatches. These occur where there is a

difference between the currency or maturity of the protection and that

of the underlying asset. These mismatches will have an impact upon the

timing of the removal of the cap and level of regulatory capital benefit

on the Uncapped Amount, but this effect is not material.

Impact at accession

The Group expects initially to calculate its capital requirements in

accordance with the Capped basis. Accordingly, the APS itself (viewed

separately from the B share issuance) at accession had no impact on

the Pillar 1 regulatory capital requirement in respect of the assets

covered by the APS. It will, however, improve the total capital ratios, and

the Core Tier 1 ratios, of the Group as a whole. It is also expected that

the protection afforded by the APS will assist the Group in satisfying the

forward looking stress testing framework applied by the FSA.

123RBS Group Annual Report and Accounts 2009