RBS 2009 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

Credit risk continued

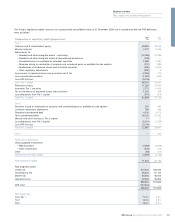

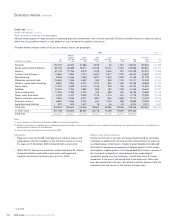

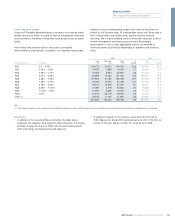

Credit risk assets*

Credit risk assets consist of loans and advances (including overdraft

facilities), instalment credit, finance lease receivables and traded

instruments across all customer types. Reverse repurchase agreements

and issuer risk (primarily debt securities – see page 151 are excluded.

Where relevant, and unless otherwise stated, data reflects the effect of

credit mitigation techniques. All the disclosures in this section (pages

130 to 141) are unaudited and are labelled with an asterisk (*).

RBS Group Annual Report and Accounts 2009130

Key points

•Total credit risk assets reduced by £146 billion, or 17% during 2009

or 13% on a constant currency basis.

•Reductions occurred across industry sectors and in most regions.

The largest reductions were in lending balances and derivatives.

•As part of the strategic review, the designation of assets between

Core and Non-Core divisions was completed during the first

half of 2009, hence the portfolio is reported according to the

divisional structure as at 31 December 2009 in the table above.

2009 2008(1)

Credit risk assets £m £m

UK Retail 103,029 97,069

UK Corporate 109,908 126,736

Wealth 15,951 17,604

Global Banking & Markets 224,355 450,321

Global Transaction Services 7,152 8,995

Ulster Bank 42,042 64,695

US Retail & Commercial 52,104 82,862

Other 2,981 6,594

Core(1) 557,522 n/a

Non-Core 151,264 n/a

708,786 854,876

Note:

(1) The 2008 analysis between Core and Non-Core is not available.

Credit concentration risk

The Group defines four key areas of concentration in credit risk that are

monitored, reported and managed at both Group and divisional levels.

These are single name, industry/sector, country and product/asset class.

Frameworks to address single name, industry/sector and country

concentrations are established and continue to be enhanced and

embedded into business processes across the Group. Aspects of the

product/asset class framework are in place whilst others will be

developed during the course of 2010.

Under the Group’s credit approval framework, the required approval

level is linked to the size of exposure with exposures above a certain

level requiring the highest level of approval, held by a very small

number of executives. In addition, the Group’s single name

concentration framework includes specific approval requirements;

additional reporting and monitoring; and the requirement to develop

plans to address and reduce excess exposures.

The Group has also developed a more robust approach and framework for

managing sector concentrations, a major outcome of which is the regular

review of the most material concentrations at the Executive Risk Forum

(ERF). These reviews include an assessment of the Group’s franchise in a

particular sector, an analysis of the outlook (including downside

outcomes), identification of key vulnerabilities and stress/scenario tests.

Reviews conclude with specific sector caps and other portfolio strategies

to align the Group’s exposure profile with its appetite.

Country risk

Country risk arises from sovereign events (for example, default or

restructuring); economic events (for example, contagion of sovereign

default to other parts of the economy, cyclical economic shock); political

events (for example, convertibility restrictions and expropriation or

nationalisation); and natural disaster or conflict. Losses are broadly

defined and include credit, market, liquidity, operational and franchise

risk related losses.

The Group’s appetite for country risk is set by the ERF in the form of

limits by country risk grade, with sub-limits on term exposure. Countries

where exposures exceed this limit framework are approved by the ERF

while authority is delegated to the Group Country Risk Committee

(GCRC) to manage exposures within the framework. Specific limits are

set for each country based on a risk assessment taking into account the

Group’s franchise and business mix in that country. Additional limitations

– on product types with higher loss potential, for example – are

established to address specific vulnerabilities in the context of a

country's outlook and/or the Group's business strategy in a particular

country. A country watch list framework is in place to proactively monitor

emerging issues and facilitate the development of mitigation strategies.

* unaudited