RBS 2009 Annual Report Download - page 364

Download and view the complete annual report

Please find page 364 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

365 -

366

366 -

367

367 -

368

368 -

369

369 -

370

370 -

371

371 -

372

372 -

373

373 -

374

374 -

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Additional information continued

RBS Group Annual Report and Accounts 2009362

The Group participated fully in the consultation processes on the

Banking Reform Bill and the Financial Services Bill. It also engaged with

policymakers on Lord Turner’s Review, ‘A regulatory response to the

global banking crisis’, and its associated consultations. These set out a

wide range of ideas and proposals, aimed at strengthening the

resilience of the banking system and addressing perceived short-

comings in existing regulation, notably with respect to the quantum and

quality of bank regulatory capital. Many of these were subsequently

reflected in more detailed proposals issued by the Basel Committee on

Banking Supervision in December 2009 (see below).

Linked to these issues is the policy debate over systemic banks. The

Group has contributed to responses to a number of systemic bank

proposals and is participating in the FSA’s pilot for the development of

Recovery and Resolution Plans (“Living Wills”). It will be developing

suitable Recovery and Resolution Plans in line with forthcoming

regulatory requirements.

Finally, the FSA has taken an active lead in implementing the G20’s

principles on remuneration structures, introducing a Code on

Remuneration Practices which formally took effect on 1 January 2010.

During the second half of 2009, the Group engaged with FSA on its

Code as it was developed, and put in place new governance processes

and policies to deliver compliance. More information on these aspects

can be found on page 225.

In addition to the above, the Group continued to comment on other

specific regulatory and legal changes that could impact its business.

Examples included the FSA’s retail distribution and mortgage market

reviews; and the Department for Business, Innovation and Skills and HM

Treasury’s consumer reforms, including with respect to credit card

markets.

New requirements that took effect during the period under review

include the EU’s Payment Services Directive (PSD), which came into

force on 1 November 2009, and the FSA’s new liquidity regime for

banks, whose systems and controls requirements took effect on

1 December 2009. The PSD provides an extensive regulatory framework

for European payments markets, by opening up the provision of

payment services to non-bank providers; increasing consumer

protection through new rules on execution times, transparency of

information, liability and pricing; and regulating providers of payment

services through licensing. The new FSA liquidity regime will require

much larger liquidity buffers to be held by specified banks, phased in

over a number of years.

UK regulated firms within the Group are members of the Financial

Services Compensation Scheme (FSCS), which provides compensation

to eligible customers of authorised financial services firms that are

unable to meet their obligations. The FSCS is funded through annual

levies charged to UK regulated firms. These levies are apportioned

between firms on the basis of their shares of the FSCS tariff base: in

the case of deposit takers, this means that levies are determined by

their share of protected deposits. As a result of FSCS involvement in a

number of bank failures in 2008, there has been a significant impact on

levies charged to deposit takers, as reflected in the accounts. Also a

significant aspect of RBS’ response to regulatory developments during

the year was addressing new requirements for banks to develop a

‘single customer view’ systems capability, tailored to generate

information required by FSCS in order to facilitate the early payment by

the Scheme of compensation to depositors. The industry is expected to

have the prescribed Single Customer View in place by end-2010.

The FSA, in their 2009/10 Business Plan, emphasised the strengthening

of their focus on ‘Treating Customers Fairly’. The Group continues to

undertake a process of continuous improvement of management

information, and root cause analysis of customer issues, in order to

demonstrate its commitment to treating customers fairly throughout the

product lifecycle.

The Group also continues to co-operate with the Information

Commissioner’s Office, the UK’s independent public body set up to

promote access to official information and to protect personal

information. The Group continues to improve its processes in line with

changing guidelines in order to meet information security requirements.

European Union/Global developments

In the EU, the Group has also responded to a number of proposals for

regulatory and legislative change, including further proposed

amendments to the Capital Requirements Directive and proposals for

establishing new EU regulatory authorities, which are aimed at

significantly strengthening EU level oversight and coordination of

national supervisors. The Group also follows closely the work (and

recommendations) of the G7 and G20, as well as international standard

setters such as the Basel Committee on Banking Supervision. Of

particular note was the Committee’s initial proposals for major changes

to the quality and quantum of banks’ regulatory capital, which were

published in December 2009. The Group is actively reviewing these,

which the Basel Committee is aiming to finalise by end-2010, for

implementation from end-2012 onwards.

United States

In the US the Group engages constructively with regulators and other

bodies on regulatory and legislative change and seeks to ensure proper

implementation and compliance. Current issues include mortgage

reform and student lending.

Other jurisdictions

The Group is active in monitoring regulatory developments in each

country in which it operates to ensure internal policies are sufficient to

ensure the effective management of regulatory risk.

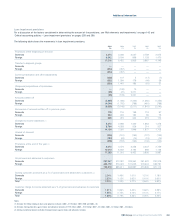

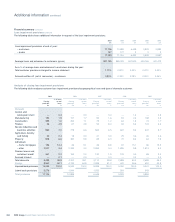

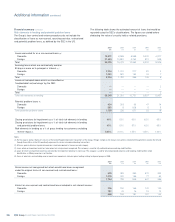

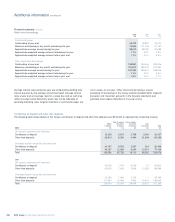

Description of property and equipment

The Group operates from a number of locations worldwide, principally in

the UK. At 31 December 2009, the Royal Bank and NatWest had 649

and 1,612 retail branches, respectively, in the UK. Ulster Bank has a foot

print of 238 branches and an extensive network of business banking

offices across Northern Ireland and the Republic of Ireland. US Retail &

Commercial had 1,512 retail banking offices (including in-store

branches) covering Connecticut, Delaware, Illinois, Massachusetts,

Michigan, New Hampshire, New Jersey, New York, Ohio, Pennsylvania,

Rhode Island and Vermont. A substantial majority of the UK branches

are owned by the Royal Bank, NatWest and their subsidiaries or are

held under leases with unexpired terms of over 50 years. The Group’s

principal properties include its headquarters at Gogarburn, Edinburgh,

its principal offices in London at 135 and 280 Bishopsgate and the

Drummond House administration centre located at South Gyle,

Edinburgh.