RBS 2009 Annual Report Download - page 163

Download and view the complete annual report

Please find page 163 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

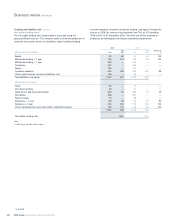

Business review

Risk, capital and liquidity management

161RBS Group Annual Report and Accounts 2009

Market risk

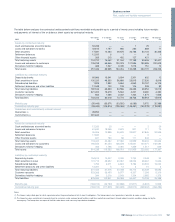

All the disclosures in this section (pages 161 to 166) are audited unless

indicated otherwise with an asterisk (*).

Market risk arises from changes in interest rates, foreign currency, credit

spread, equity prices and risk related factors such as market volatilities.

The Group manages market risk centrally within its trading and non-

trading portfolios through a comprehensive market risk management

framework. This framework includes limits based on, but not limited to

VaR, scenario analysis, position and sensitivity analyses.

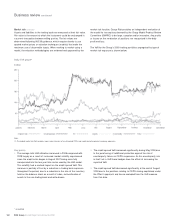

Measurement

At the Group level, the risk appetite is expressed in the form of a

combination of VaR, sensitivity and scenario limits. VaR is a technique

that produces estimates of the potential change in the market value of a

portfolio over a specified time horizon at given confidence levels. For

internal risk management purposes, the Group’s VaR assumes a time

horizon of one trading day and in June 2009 the Group changed its VaR

confidence level from 95% to 99% as it considers this provides greater

clarity in respect of more severe potential economic outcomes. The

Group’s VAR model is based on a historical simulation model utilising

data from the previous two years trading results.

The Group continued to update and enhance its market risk

management framework during 2009. In addition to the move to a VaR

based on a 99% confidence level, the Group has improved and

strengthened its market risk limit framework increasing the transparency

of market risk taken across the Group’s businesses in both the trading

and non-trading portfolios.

The Group’s market risk appetite is defined within this limit framework

which is cascaded down through legal entity, division, business and

ultimately trader level market risk limits.

The VaR disclosure is broken down into trading and non-trading, where

trading VaR relates to the main trading activities of the Group and non-

trading reflects the VaR associated with reclassified assets, money

market business and the management of internal funds flow within the

Group’s businesses.

As part of the strategic review, the designation of assets between Core

and Non-Core divisions was completed during 2009. As the Non-Core

division was not established until conclusion of the strategic review in

the first quarter of 2009, constitution of the average, maximum and

minimum VaR for Core and Non-Core has been prepared on a best

efforts basis as these measures require daily data.

The Group calculates VaR using historical simulation models but does

not make any assumption about the nature or type of underlying loss

distribution other than implied by history. The methodology uses the

previous 500 trading days of market data and calculates both general

market risk (the risk due to movement in general market benchmarks)

and idiosyncratic market risk (the risk due to movements in the value of

securities by reference to specific issuers). The Group VaR should be

interpreted in light of the limitations of the methodology used as follows:

•Historical simulation VaR may not provide the best estimate of future

market movements. It can only provide a prediction of the future

based on events that occurred in the time series horizon. Therefore,

events that are more severe than those in the historical data series

cannot be predicted;

•VaR that uses a 99% confidence level does not reflect the extent of

potential losses beyond that percentile;

•VaR that uses a one-day time horizon will not fully capture the profit

and loss implications of positions that cannot be liquidated or

hedged within one day; and

•The Group computes the VaR of trading portfolios at the close of

business. Positions may change substantially during the course of

the trading day and intra-day profit and losses will be incurred.

A ‘Risks not in VaR’ framework has been developed to address those

market risks not adequately captured by the market standard VaR

methodology. Where risks are not included in the model, various non-

VaR controls (for example, position monitoring, sensitivity limits, triggers

or stress limits) are in place.

These limitations mean that the Group cannot guarantee that losses will

not exceed the VaR.

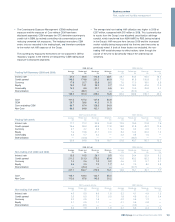

Traded portfolios

The primary focus of the Group’s trading activities is client facilitation.

The Group also undertakes activities within the Core division of the

wholesale bank, built around clients in chosen markets, including:

•Market making – quoting firm bid (buy) and offer (sell) prices with the

intention of profiting from the spread between the quotes.

•Arbitrage – entering into offsetting positions in different, but closely

related markets in order to profit from market imperfections.

•Proprietary activity – taking positions in financial instruments as

principal in order to take advantage of anticipated market conditions.

Financial instruments held in the Group’s trading portfolios include, but

are not limited to: debt securities, loans, deposits, equities, securities

sale and repurchase agreements and derivative financial instruments

(futures, forwards, swaps and options).

The Group participates in exchange traded and over-the-counter (OTC)

derivatives markets. The Group buys and sells financial instruments that

are traded or cleared on an exchange, including interest rate swaps,

futures and options. Holders of exchange traded instruments provide

daily margins with cash or other security at the exchange, to which the

holders look for ultimate settlement.

The Group also buys and sells financial instruments that are traded

OTC, rather than on a recognised exchange. These instruments range

from commoditised transactions in derivative markets, to trades where

the specific terms are tailored to the requirements of the Group’s

customers. In many cases, industry standard documentation is used,

most commonly in the form of a master agreement, with individual

transaction confirmations.